AI, Musk, Altman, Amodei, Karp and the Insiders' Headstart

KXCO maps the dozen people who decide how artificial intelligence gets built — across compute, models, robotics, defence, space, biotech and brain-computer interfaces — and makes the case that they hold capable AI the public can't see. Explore the live ontology at kxco.ai/ontology-live.

Part of theAI Stocks Center

A small number of people now decide how artificial intelligence gets built, who it serves, and how fast it arrives. Not thousands. Not even hundreds. If you wanted to draw the real command structure of the AI economy on one page, you could do it with about a dozen names and the companies, chips, data centres and capital that connect them.

I have spent the last few years arguing that the most important thing about this moment is not any single model or product — it is the structure: who is connected to whom, who depends on whom, and who is quietly ahead of everyone else. So my team and I built a living map of it. You can open it right now at kxco.ai/ontology-live, and this week we added the people themselves — Elon Musk, Sam Altman, Dario Amodei, Demis Hassabis, Jeff Bezos, Mark Zuckerberg, Jensen Huang, Alex Karp, Satya Nadella, Ilya Sutskever, Mira Murati and Liang Wenfeng — wired to the empires they run.

This article is the guided tour. It profiles each of the people building AI, maps what they are actually doing across compute, models, robotics, defence, space, energy, biotech and brain-computer interfaces, and then draws a conclusion I want to state plainly at the top, because it is the whole point:

The people who build the frontier have access to AI that is meaningfully better than anything you or I can use — and they have it first, wired into their own work, months before the rest of us see it. They built it, so the advantage is fair. But it is real, it is compounding, and it is worth watching closely. That is my thesis, and by the end I will show you the evidence for it — including the parts that argue against the most extreme version of the claim.

Who are the senior people building AI?

Let me answer the plain question first, because it is the one people search for and the one most articles dance around. The senior operators of the major AI companies — the ones whose decisions move the whole field — are, as of mid-2026:

Sam Altman, CEO and co-founder of OpenAI.

Dario Amodei, CEO and co-founder of Anthropic.

Elon Musk, who controls xAI, Tesla, SpaceX and Neuralink.

Demis Hassabis, CEO of Google DeepMind, working under Sundar Pichai at Alphabet.

Mark Zuckerberg, CEO of Meta, with Alexandr Wang as chief AI officer of Meta Superintelligence Labs.

Jensen Huang, founder and CEO of Nvidia — the company that sells the shovels to everyone else.

Satya Nadella, chairman and CEO of Microsoft.

Alex Karp, co-founder and CEO of Palantir.

Jeff Bezos, founder of Amazon, funding Blue Origin and a new AI venture, Prometheus.

Ilya Sutskever, co-founder and CEO of Safe Superintelligence.

Mira Murati, founder and CEO of Thinking Machines Lab.

Liang Wenfeng, founder of DeepSeek, China's most disruptive lab.

That is the power set. Twelve people, a handful of companies, and a supply chain that runs all the way down to a single Dutch company — ASML — that makes the lithography machines every advanced AI chip is printed on. Understanding these individuals is not celebrity-watching. It is the fastest way to understand where the technology, and a good chunk of the world's capital, is going next.

Why a map, and not a list

Before the profiles, one point about method, because it is the reason this piece exists on a live ontology and not just as a slideshow.

A list tells you who exists. It does not tell you that Google funds Anthropic and rents compute from a rocket company, or that Nvidia invests in the very customers who buy its chips, or that roughly a trillion dollars of announced AI deals circle around inside one small cohort. Those are relationships, and relationships are where the meaning lives. A database stores rows; a blockchain stores events; neither understands relationships. An ontology does — it treats every fact as a typed, sourced claim connecting one thing to another, each carrying a source, a date and a confidence level.

That is what the KXCO Ontology Engine is: the AI sector rendered as objects and the verifiable claims between them. As you read the profiles below, everything I assert about who controls what, who funds whom, and who depends on whom is a claim you can click on in that map and check for yourself. That is the standard I want journalism about AI to be held to, and it is the standard I am holding myself to here.

The power set, one by one

Elon Musk — the physical-world bet

Core themes. Musk is the only figure in this group whose AI thesis is fundamentally about atoms, not just bits. His argument is that intelligence is becoming cheap, so the constraint moves to the physical world: robots, energy, and getting off the planet. He talks about civilisation the way other executives talk about quarterly targets.

What he is building. xAI merged into SpaceX in an all-stock deal in early 2026, folding the Colossus supercomputers — some of the largest training clusters on Earth — into the same entity that builds Starship, a company that has since completed its own IPO and now trades as SPCX. Tesla is pushing the Optimus humanoid robot toward mass production and the Cybercab toward the road. And Neuralink, his brain-computer interface company, had implanted its device in twelve people by September 2025 and is moving toward automated robotic surgery and a visual-cortex implant called Blindsight. On the map, Musk sits at the centre of a personal interlock — SpaceX, xAI, Tesla and Neuralink — that no one else in the field comes close to matching.

What worries him. Musk has repeatedly put a rough number on it — something like a one-in-five chance of catastrophe from advanced AI — while arguing that building it himself is safer than ceding it to others. He worries about civilisational fragility: low birth rates, energy shortages, and misaligned machines.

Health and longevity. He is publicly optimistic that ageing is a solvable problem, though he channels most of that energy into species-level survival — making humanity multi-planetary — rather than personal biohacking.

Sam Altman — the abundance salesman

Core themes. Altman's message is relentless optimism about abundance: intelligence and energy both trending toward near-free, and a world reorganised around that. He speaks in "thousands of days" to superintelligence and frames AI as the great accelerant of science.

What he is building. OpenAI is at the centre of the largest infrastructure mobilisation in corporate history — the $500 billion Stargate joint venture with SoftBank and Oracle, a $100 billion commitment from Nvidia paid in GPUs, and a $300 billion, multi-year Oracle compute deal. But the most revealing Altman bets are personal and biological. He seeded the longevity company Retro Biosciences with $180 million of his own money; it is now valued around $1.8 billion and running its first human trial of an anti-ageing pill. OpenAI even built a custom protein-design model that reportedly made cellular reprogramming roughly fifty times more efficient. He has also co-founded Merge Labs, a brain-computer interface startup that puts him head-to-head with Musk's Neuralink.

What worries him. Altman has warned since 2015 that AI could be "the greatest threat to the continued existence of humanity," and co-signed the 2023 statement putting extinction risk alongside pandemics and nuclear war. His day-to-day worry now is societal readiness and misuse.

Health and longevity. Diet, exercise, sleep, and metformin — plus the biggest cheque of anyone in the group written directly at extending human lifespan.

Dario Amodei — the safety-first accelerationist

Core themes. Amodei is the field's most articulate paradox: he believes AI will be extraordinarily, almost unimaginably powerful — and precisely because of that, it must be built carefully. His essay "Machines of Loving Grace" describes "a country of geniuses in a datacentre" that could compress a century of biomedical progress into five to ten years.

What he is building. Anthropic's Claude models, with an unusually heavy investment in safety and alignment research, funded by up to $10 billion from Nvidia and a $30 billion Azure compute commitment, at a valuation that has climbed at a blistering pace. Notably, Anthropic's own internal data shows a large and growing share of its code is now written by AI — its researchers increasingly review and direct AI agents rather than type.

What worries him. Catastrophic misuse — biological weapons, cyberattacks, loss of control — and a society "dangerously underprepared" for how fast this is arriving.

Health and longevity. Private about his routine. The public driver is personal: a family illness that became treatable just too late, which he cites as the root of his urgency to accelerate AI-for-biology.

Demis Hassabis — the scientist

Core themes. Hassabis, a 2024 Nobel laureate, frames AGI as an "infinity machine" and insists it is still five to ten years away because genuine scientific creativity — not just pattern-matching — remains unsolved. He is the most measured voice in the group.

What he is building. Google DeepMind's Gemini models, and Isomorphic Labs, the AlphaFold-derived drug-discovery company now moving toward clinical trials. All of it sits inside Alphabet's roughly $180 billion 2026 capital budget, overseen by Sundar Pichai.

What worries him. That too much responsibility rests on too few people. He has openly called for a "CERN for AI" — an international institution to monitor the technology.

Jeff Bezos — industry off-Earth

Core themes. Bezos thinks on a century scale: move heavy industry into space to spare the planet, and treat AI as an engine of higher living standards rather than mass unemployment.

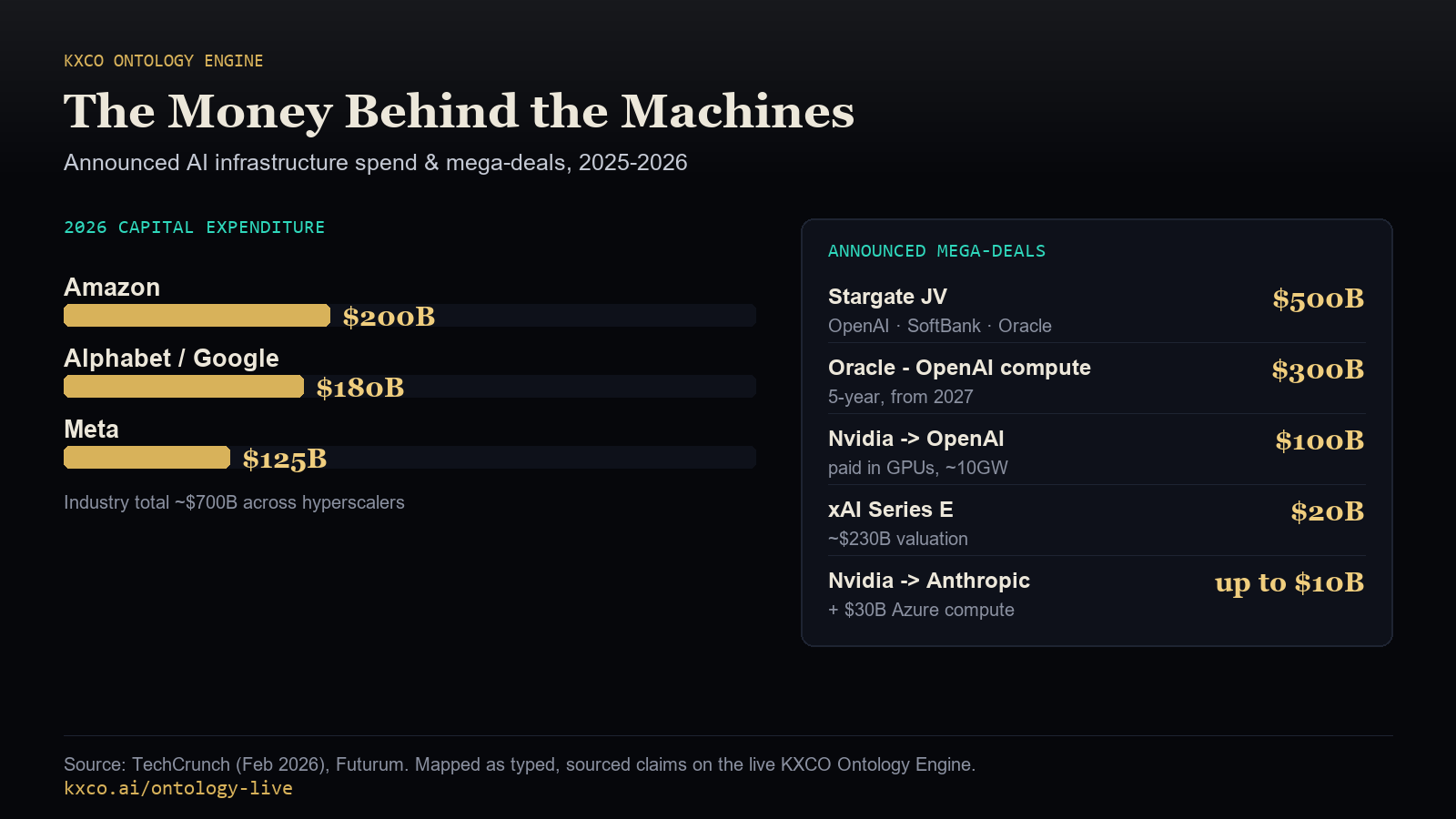

What he is building. Blue Origin, now raising outside capital for the first time; a new AI venture, Prometheus, aimed at an "artificial general engineer"; and, through Amazon, the single largest 2026 capital line in the industry at roughly $200 billion. He is also an investor in Altos Labs, the ~$5 billion cellular-reprogramming longevity firm.

Health and longevity. A structured fitness regimen with a trainer, and the Altos bet — another AI-adjacent billionaire funding the science of living longer.

Mark Zuckerberg and Alexandr Wang — spend through the doubt

Core themes. Zuckerberg's pitch is "personal superintelligence" for everyone, owned end-to-end by Meta. The strategy is to out-spend and out-hire everyone, doubts be damned.

What they are building. A stated $600 billion in US infrastructure through 2028 — including a five-gigawatt Louisiana data centre and a gas-powered Ohio site — plus a pivot to sell excess compute as a cloud business. Zuckerberg installed Alexandr Wang, founder of Scale AI, as chief AI officer of Meta Superintelligence Labs, buying talent at the top of the market.

Health and longevity. Zuckerberg co-founded the Breakthrough Prize, funds disease research through CZI, predicts living past 100 will be normal by century's end, and trains in jiu-jitsu and CrossFit.

Jensen Huang — the man who sells the shovels

Core themes. Huang's whole worldview is that we are building "AI factories," and that demand for them is structural, not a bubble. He is the counterparty to everyone.

What he is building. Nvidia designs the GPUs the entire field depends on — roughly 80% of data-centre AI compute by revenue — and has taken strategic stakes in its own customers: up to $100 billion into OpenAI, up to $10 billion into Anthropic, and a stake in xAI. The irony, which the ontology annotates directly, is that Nvidia invests in the very companies that then spend that money buying Nvidia chips.

Alex Karp — the sovereigntist

Core themes. Karp is the field's fiercest critic of the other founders. His argument is that Western governments and companies must own and control their models, data and compute — that outsourcing national security to unaccountable Silicon Valley labs is, in his words, indefensible.

What he is building. Palantir's AI Platform and Ontology, deep defence and intelligence contracts, and a battlefield AI layer used within NATO — with Nvidia as a partner for sovereign, government-grade AI.

Health and longevity. The most disciplined of the group: high-intensity cardio for VO2 max, daily Tai Chi, eight hours of sleep, very low body fat, and a diet that avoids sugar and ultra-processed food.

Satya Nadella — the platform operator

Core themes. Nadella sees AI as the platform shift of the era and is determined that Microsoft owns the layer businesses actually run on. He is the calmest capital allocator in the group.

What he is building. The OpenAI partnership and a vast Azure buildout, hedged with in-house Microsoft AI models and custom Maia silicon so Microsoft is never wholly dependent on any single lab.

Ilya Sutskever and Mira Murati — the purists

Two of OpenAI's most important alumni have gone their own way. Ilya Sutskever, the former chief scientist, founded Safe Superintelligence with a single stated goal — safe superintelligence — and no intention of shipping interim products, raising billions at no revenue. Mira Murati, OpenAI's former CTO, founded Thinking Machines Lab, gathering ex-OpenAI talent behind capable, broadly useful, transparent AI, and raised one of the largest seed rounds on record. Both are bets that the frontier can be pushed by small, focused teams rather than only by hyperscalers.

Liang Wenfeng — the disruptor

Liang Wenfeng and DeepSeek are the reason no one in this group can relax. Funded off his quantitative trading fund, DeepSeek has repeatedly delivered frontier-level results at a fraction of the compute and cost, releasing open weights as a strategy. DeepSeek is the single strongest piece of evidence that the moat around the frontier is thinner than the incumbents would like — and the clearest reason the US export-control fight matters so much.

What they are actually building

Step back from the personalities and a single shape emerges. The money is not chasing a clever algorithm. It is chasing infrastructure — and everything physical that infrastructure needs.

Compute and chips. This is the base layer, and the numbers are staggering. Combined hyperscaler capital expenditure is on track for roughly $700 billion in 2026 — Amazon near $200 billion, Alphabet $175–185 billion, Meta $115–135 billion — on top of the $500 billion Stargate project and Nvidia's direct investments. Nvidia sells the chips; TSMC fabricates them; ASML makes the machines that make them possible. Whoever controls this stack controls the pace of everything above it.

Foundation models. OpenAI, Anthropic, Google DeepMind, xAI, Meta and — from China — DeepSeek and the rest are locked in a race where the leading edge keeps moving but the gap between the leaders and the cheap, open alternatives keeps narrowing.

Energy. This is the quiet chokepoint. AI's power demand is restarting nuclear plants and prompting five-gigawatt data-centre campuses and gas plants built specifically to feed models. Energy, not talent, may be the binding constraint of the next five years.

Robotics. Tesla's Optimus and companies like Figure AI are pushing humanoid robots toward production. This is Musk's core wager: that the real payoff from cheap intelligence is cheap physical labour.

Defence. Palantir under Karp has made "AI for national security" its whole identity, with a battlefield layer inside NATO and a growing roster of government contracts.

Space. Musk's SpaceX and Bezos's Blue Origin are both, increasingly, AI-infrastructure plays — connectivity, and eventually compute and industry, beyond Earth.

Biotech and longevity. This is the pattern the mainstream coverage keeps missing. The same people building AI are personally funding the science of living longer: Altman's Retro Biosciences, Bezos's Altos Labs, Hassabis's Isomorphic Labs, Amodei's biomedical thesis, Zuckerberg's CZI. They are using AI to attack ageing itself.

Brain-computer interfaces. And at the far edge, two of the most powerful people in AI — Musk with Neuralink and Altman with Merge Labs — are racing to connect the human brain directly to machines.

Read across those eight sectors and the through-line is unmistakable: compute leads to models, and models lead into the physical world — robots, drugs, rockets, brains — with energy as the constraint everyone is scrambling to secure.

What they agree on — and where they split

For all their public feuding, the power set agrees on more than it admits. Every one of them believes transformative AI arrives this decade. Every one of them is pouring capital into compute and energy as if that belief were certain. And nearly every one of them, quietly or loudly, is hedging their personal future against mortality itself.

Where they split is on the route. Altman and Musk are all-in consumers of compute, building as fast as capital allows. Zuckerberg and Nadella build first and sell the excess, treating infrastructure as a product. Amodei, Sutskever and Hassabis wrap the ambition in guardrails and talk openly about catastrophe. Karp rejects the whole Silicon Valley frame in favour of sovereignty and defence. And Liang Wenfeng simply does it cheaper, proving the incumbents' moat is narrower than their valuations imply.

That combination — total agreement on the destination, sharp disagreement on the path — is exactly the condition under which a small group pulls ahead of everyone else. Which brings me to the thesis.

The trillion-dollar loop

There is one more structural feature you cannot see from a list of names, and it is the one that worries me most as an investor. The capital in this sector does not flow in a straight line from backers to builders. It flows in a circle.

Follow it. Nvidia invests up to $100 billion in OpenAI. OpenAI commits hundreds of billions to compute — much of which is spent, directly or indirectly, on Nvidia chips. SoftBank and Oracle fund Stargate; Stargate buys Nvidia. Microsoft funds both OpenAI and Anthropic; both spend that money on Azure, which runs on Nvidia. Google funds Anthropic while renting compute from a rocket company, SpaceX, whose data centres are filled with Nvidia GPUs. Roughly a trillion dollars of announced deals circulate inside one small cohort, and a striking share of it ends up back where it started.

This is not necessarily fraud or folly — vendor financing is an old and sometimes rational strategy. But it means the sector's most important numbers are, to a degree, marking their own homework. When a chipmaker invests in the customer who then reports record chip purchases, revenue growth and demand signals get harder to read from the outside. The ontology annotates these loops explicitly — there is a filter on the live map that shows only the circular flows — because they are precisely the kind of relationship that a headline reports as growth and a graph reveals as a loop.

I raise it here, in the middle of the argument about the insiders' headstart, deliberately. The same concentration that gives a dozen people an informational lead in capability gives them a lead in understanding the real economics of this buildout. They know which demand is genuine and which is recycled, because they are on both ends of the transaction. The rest of us are reading press releases. That asymmetry — not just who has the best model, but who can actually see whether the money makes sense — is the deeper version of the headstart, and it is the reason a public, verifiable map of the flows is not a nice-to-have. It is a defence.

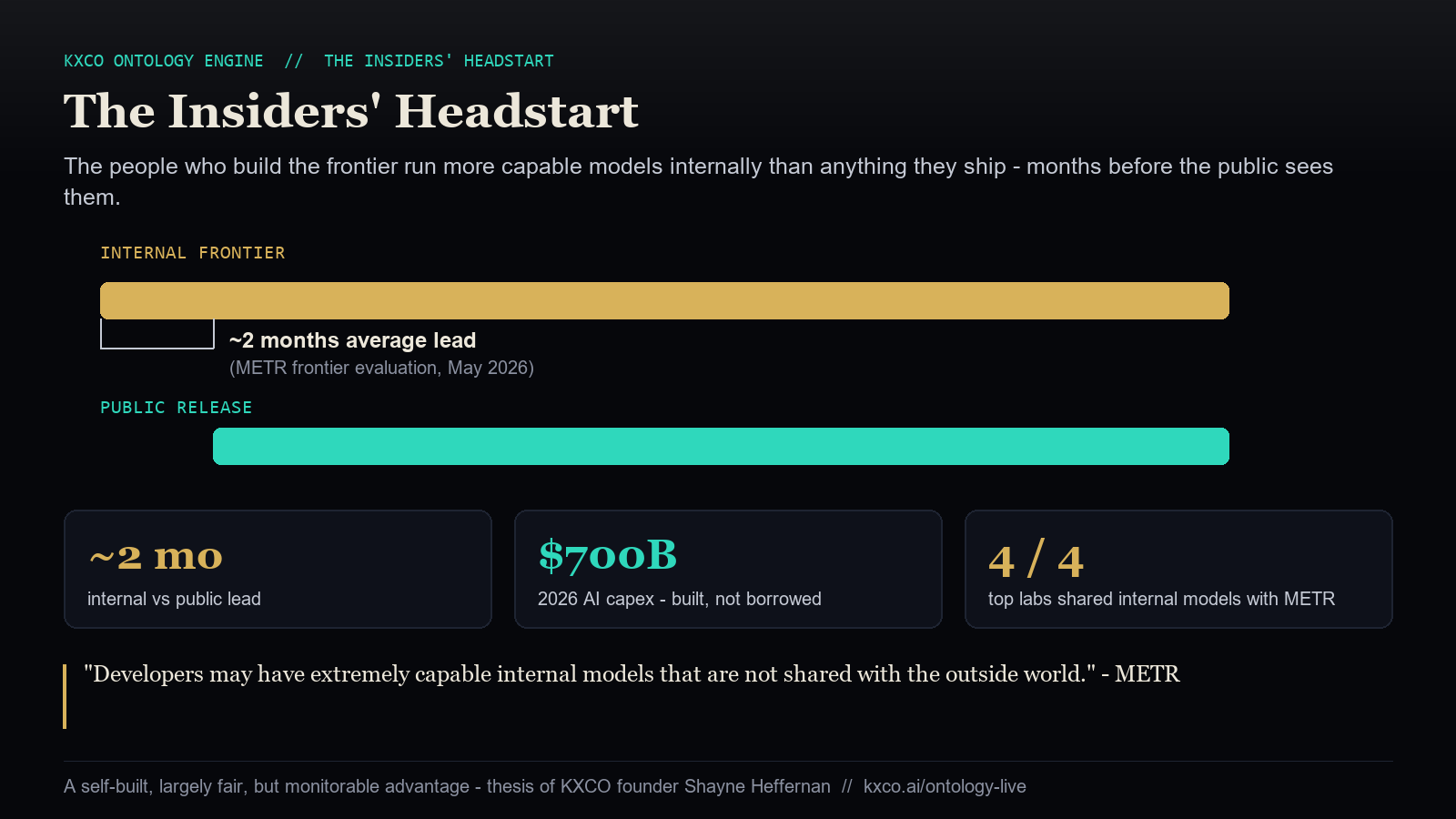

The Insiders' Headstart

Here is what I believe, stated as plainly as I can: the people in this article are working with AI that is materially more capable than anything the public can access, and they have it first.

I do not mean a conspiracy. I mean something more mundane and more important. When a lab trains a new frontier model, it does not appear in your chatbot the next morning. It is used internally for months — to write code, to run research, to design the next model — before it is ever released, if it is released at all. The most advanced version of the technology is always the one being used by the people building it, pointed at the problem of building more of it.

The honest version of the theory

I want to be careful here, because this is exactly the kind of claim that gets inflated into nonsense, and I would rather be right than loud.

The strongest evidence comes from METR, an independent evaluation organisation that, in 2026, was given access to the actual internal frontier models of Anthropic, Google, Meta and OpenAI — not the public versions. Their finding cuts both ways. On one hand, it confirms the headstart is real: the labs do run more capable models internally than they release, and they deploy them heavily on their own R&D. On the other hand, it puts a number on the gap that should keep the theory honest — internally, the frontier was on average only about two months ahead of what the public could document, and none of the internal models were dramatically, secretly superhuman.

So the extreme version of the theory — that a lab is sitting on a hidden artificial general intelligence years beyond public knowledge — is not supported by the best evidence we have. But the reasonable version is not just supported, it is confirmed by the labs' own transparency framework, which explicitly warns that "developers may have extremely capable internal models that are not shared with the outside world," and treats "how many months behind is your public model?" as a metric worth disclosing.

Two months does not sound like much. But compound it. Two months of head start, using the best model to build the next best model, funded by hundreds of billions of dollars, repeated cycle after cycle, concentrated in a dozen people — that is not a gap that closes on its own. It is a gap that widens.

This is why I keep returning to the same conclusion. The advantage is fair — they built it, they paid for it, and in most cases they took real risks to do so. But fair is not the same as safe to ignore. An advantage this concentrated, this compounding, and this invisible to outsiders is precisely the kind of thing a healthy society keeps a close eye on. Not to punish it. To understand it, and to be ready.

Why this needs an ontology, not a headline

Everything I have described — the people, the companies, the deals, the dependencies, the headstart — is a set of relationships that changes every week. You cannot hold it in a static article, and you certainly cannot hold it in your head. That is precisely the problem an ontology solves, and it is why the KXCO Ontology Engine now includes these twelve individuals alongside the roughly one hundred companies, chokepoints and capital flows they connect to.

Open it and you can ask it questions directly: Who holds a capability headstart the public can't see? Who rents compute from a rival? Who funds a company they compete with? What does the whole sector rest on? Every answer is a typed, sourced claim you can inspect — the same discipline I have tried to hold to in this piece. It is the difference between being told what to think about AI and being able to check it.

That is the real reason we build these maps at KXCO. The AI economy is being assembled at a speed and scale that outruns ordinary reporting. The only way to keep it accountable is to model it as what it actually is — a graph of objects and verifiable relationships — and to keep that graph honest, current and public.

The China question

No honest map of AI power stops at the American coast. The most important structural fact of the last eighteen months is that China has built a near-complete parallel stack: SMIC fabricating chips, Huawei designing them, and a cluster of labs — DeepSeek, Alibaba, ByteDance, Baidu, Tencent, Zhipu, MiniMax and Moonshot — training models that increasingly rival the American frontier. Liang Wenfeng's DeepSeek is the emblem of it: open-weight models delivered at a fraction of Western training cost, released deliberately to erode the incumbents' pricing power.

This changes the headstart argument in an important way. Inside the United States, the frontier is concentrated in a dozen people who share, however grudgingly, a common regulatory environment and a common set of independent evaluators. Across the Pacific, a second frontier is advancing that answers to none of those. The US export controls on advanced chips and lithography — the ASML and Nvidia chokepoints — are the single biggest lever anyone has over the pace of that second stack, which is exactly why the fight over them is so bitter.

For an investor or a policymaker, the takeaway is uncomfortable but clear: the "insiders" are not one group but two, in two systems, and the gap between them is now measured in months, not years. A headstart that a Western lab holds over the Western public is one thing. A headstart — in either direction — between two superpowers building superintelligence is a different order of question, and it is the one that will dominate the back half of this decade. The ontology maps both stacks side by side for precisely this reason: you cannot reason about one without the other.

What to watch

Three things, over the next year, will tell you whether the headstart is widening or closing.

First, the IPO wave. SpaceX has already gone public — it completed its IPO and now trades as SPCX, the first of this cohort to list and the first real read on public appetite for the buildout. OpenAI and Anthropic are still to come; when they file, we will see the numbers that show how much of that $700 billion in spending is being validated by demand.

Second, the internal-versus-public gap. Watch whether independent evaluators like METR keep getting access, and whether that two-month gap grows. If the labs stop sharing, that itself is information.

Third, the challengers. Watch DeepSeek and the open-weight models. Every time they match the frontier for a fraction of the cost, the insiders' headstart shrinks — and the argument for keeping a close, public eye on the whole structure gets easier to make.

The people in this article are not villains, and they are not wizards. They are a small group of extraordinarily capable operators who got to the frontier first and are using every advantage of being there. Understanding them — precisely, not breathlessly — is the first step to making sure the rest of us are not left reacting to a world that a dozen people already finished building. That understanding starts with a map, and the map is live.

Frequently asked questions

Who are the CEOs of the major AI companies in 2026? Sam Altman leads OpenAI; Dario Amodei leads Anthropic; Demis Hassabis leads Google DeepMind under Sundar Pichai at Alphabet; Elon Musk controls xAI (now merged into SpaceX) as well as Tesla and Neuralink; Mark Zuckerberg leads Meta with Alexandr Wang as chief AI officer; Jensen Huang founded and runs Nvidia; Satya Nadella chairs and runs Microsoft; Alex Karp co-founded and runs Palantir; Ilya Sutskever leads Safe Superintelligence; Mira Murati leads Thinking Machines Lab; and Liang Wenfeng founded DeepSeek in China.

Do AI leaders have access to more powerful AI than the public? Yes — with an important caveat about degree. Independent evaluation by METR in 2026, using the labs' actual internal models, confirmed that frontier developers run more capable models internally than they release, and use them heavily on their own research. But the measured gap was on average about two months, not the years-ahead secret superintelligence that the most dramatic version of the theory imagines. The advantage is real, compounding and worth monitoring; it is not a hidden AGI.

What is an ontology, and why does AI need one? An ontology is a formal map of things and the relationships between them, where every fact is a typed claim carrying a source, a date and a confidence level. A database stores rows and a blockchain stores events, but neither understands relationships — which is where meaning, and risk, actually live. As AI agents begin to act in the world, they need a shared, verifiable model of what is real and how it connects. That is the layer the KXCO Ontology Engine demonstrates at kxco.ai/ontology-live.

Who funds OpenAI and Anthropic? OpenAI's backers include Microsoft (~27%), Nvidia (up to $100 billion, paid in GPUs), SoftBank and Oracle (through Stargate and compute deals). Anthropic is backed by Nvidia (up to $10 billion), Microsoft/Azure ($30 billion in compute), Amazon and Google — a web of overlapping investments in which Google, notably, funds Anthropic while competing with it.

Which company is most important to AI? By dependency, three: Nvidia, which designs roughly 80% of data-centre AI chips by revenue; TSMC, which fabricates the leading-edge silicon; and ASML, the sole maker of the EUV lithography machines that make those chips possible. The whole sector rests on that spine — a point the ontology map makes visible at a glance.

Are the tech billionaires investing in living longer? Several are, directly. Sam Altman seeded Retro Biosciences; Jeff Bezos backs Altos Labs; Demis Hassabis founded Isomorphic Labs; Dario Amodei's thesis centres on compressing biomedical progress; and Mark Zuckerberg funds disease research through CZI. The same people building AI are using it to attack ageing.

What is the biggest risk in the AI buildout? Concentration. A dozen people, two national systems, and roughly $700 billion of annual spending are deciding the shape of a general-purpose technology faster than institutions can supervise it. The risk is not that any one of them is malicious; it is that an advantage this large and this invisible goes unwatched.

The KXCO Ontology Engine is a public reference that models the AI sector as typed, sourced claims. Explore it at [kxco.ai/ontology-live](https://kxco.ai/ontology-live/).

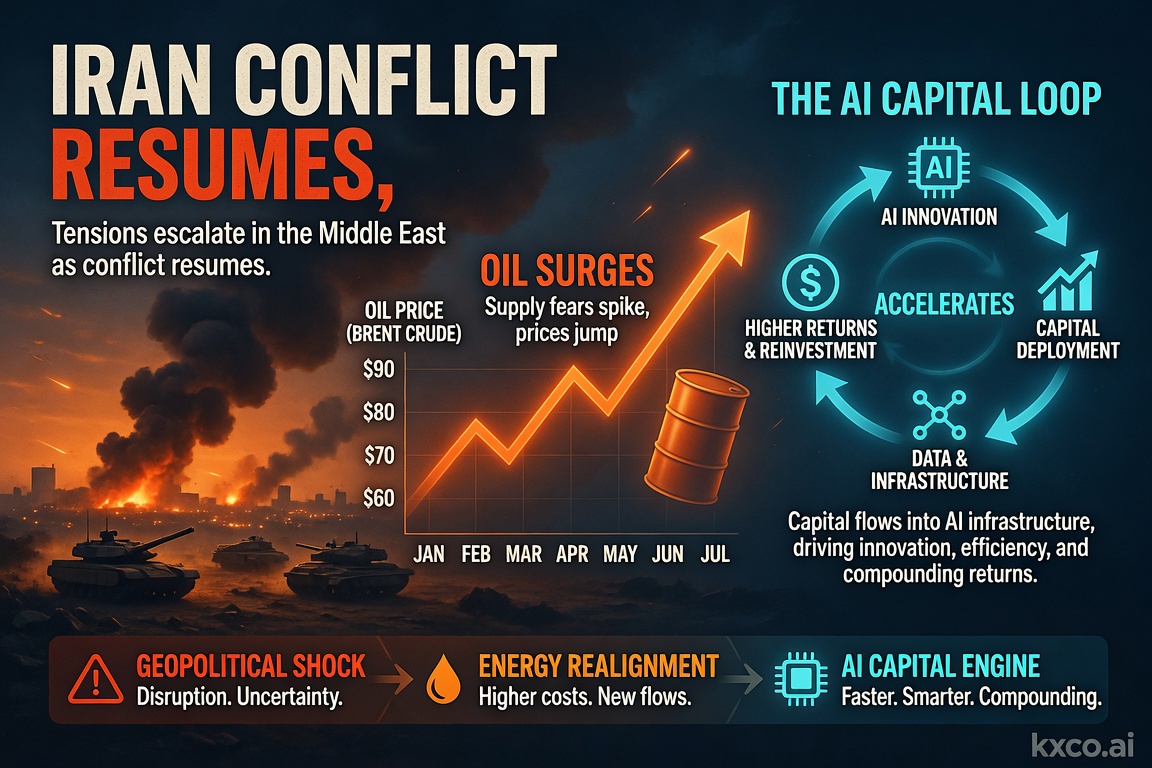

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

Who Is Who in the AI Space: The Definitive Guide to AI Stocks in 2026

The definitive 2026 guide to AI stocks: $NVDA, $GOOGL, $MSFT, $AMZN, $META, $TSM, $AVGO, $ORCL and $PLTR in the US; $BABA, $TCEHY and $BIDU in China — each mapped to its layer of the AI value chain, with cashtags, market caps and the investment thesis for each.

Ontology: Agentic AI and Infrastructure

The AI trade so far has been a compute trade. The next leg is a meaning trade — and ontology, secured and settled, is the layer almost everyone is skipping. Shayne Heffernan on why ontology is the missing layer in agentic AI, and the infrastructure it needs.

AI and Quantum Computing Latest News

AI and quantum computing are converging into a single US-China contest. A fact-checked, investor-focused map of the model gap, the quantum milestones, the security imperative, and the stocks positioned across both — NVDA, GOOGL, MSFT, IBM, IONQ, TSM. By Shayne Heffernan.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.