AI and Quantum Computing Latest News

The US-China race is no longer about one technology. Shayne Heffernan maps where AI and quantum computing actually stand in mid-2026 — the near-parity model gap, the quantum milestones from Willow to Zuchongzhi 3.2, why the two are converging, and the AI + quantum stocks to watch.

Part of theAI Stocks Center

The United States and China are no longer racing to win a single technology. They are racing to master two at once — artificial intelligence and quantum computing — and, increasingly, to master the way those two reinforce each other. The country that pairs frontier AI with useful quantum hardware, and secures the whole stack against the day a quantum machine can break today's encryption, will hold a durable advantage across defence, finance, drug discovery and materials science.

For investors, this is not an abstract contest. It is already repricing semiconductors, cloud infrastructure, a young cohort of quantum pure-plays, and a new category of companies whose entire job is to keep the AI-quantum stack trustworthy. This piece maps where the two powers actually stand in mid-2026 — corrected against the primary sources rather than the hype — why the two technologies are converging, and what it means for portfolios over the next 12 to 24 months.

The short version

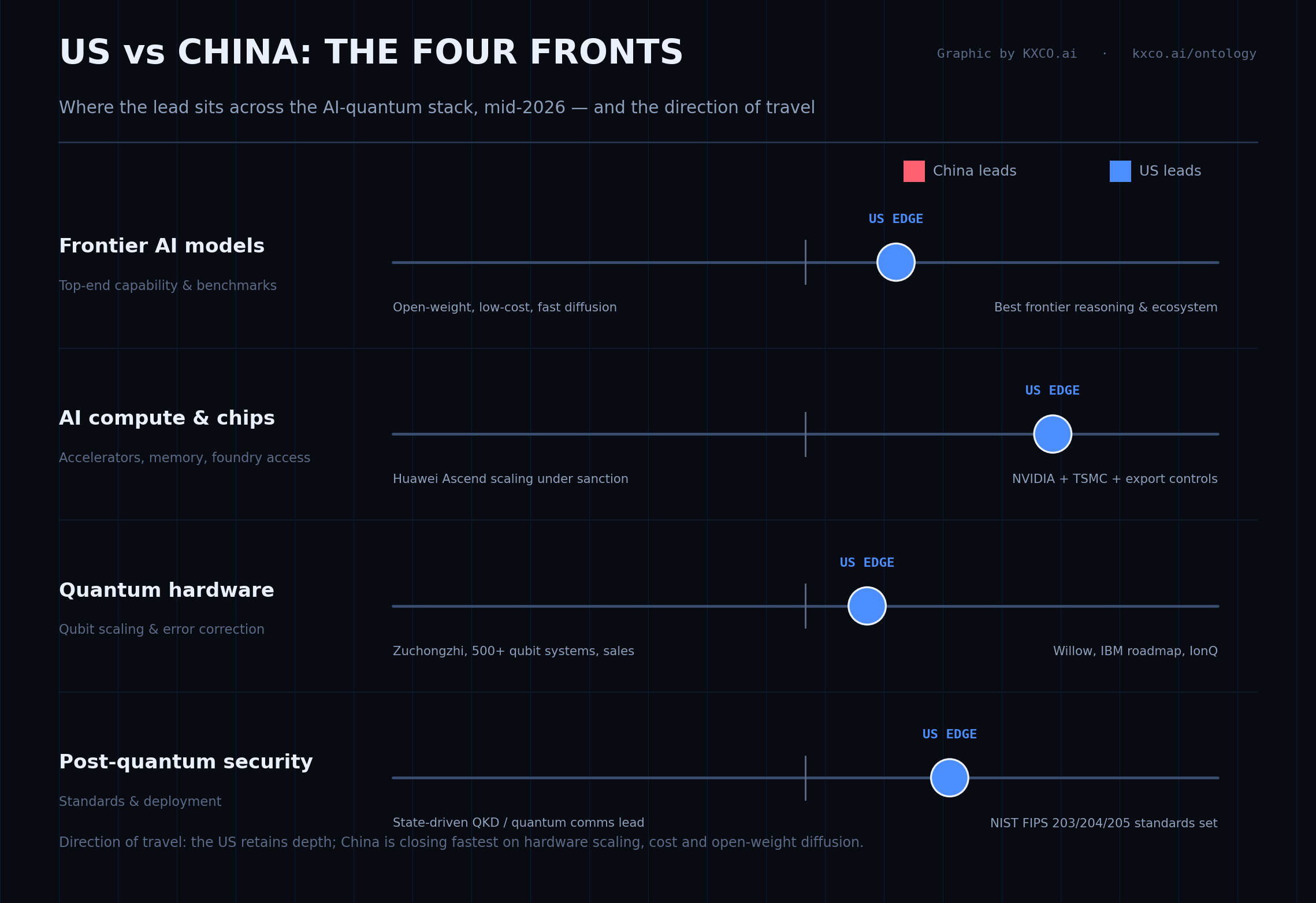

The AI gap has narrowed to near-parity, not closed. Stanford's 2026 AI Index puts the leading US model just ~2.7% ahead of the best Chinese model on the LMArena leaderboard, down from double digits two years ago. But the US still produced 50 notable models in 2025 versus China's 30, and retains the deeper research ecosystem.

China is winning on diffusion. DeepSeek, Alibaba's Qwen, Zhipu's GLM and Moonshot's Kimi ship open weights at a fraction of US pricing and now supply a large share of the world's open-model usage.

In quantum, America leads and China is scaling fastest. Google's Willow and IBM's roadmap set the pace on fault-tolerant computing, but China has matched below-threshold error correction (Zuchongzhi 3.2), fielded a 504-qubit machine, and started selling quantum computers — including an export order.

The security clock is the sleeper trade. NIST's post-quantum cryptography standards are finalised; the migration is just beginning. Organisations slow to move are exposed to "harvest-now, decrypt-later" attacks today.

The AI race: near-parity, not a blowout

The single most repeated claim about AI in 2026 — that China has "caught up" — needs a precise correction. It has nearly caught up at the very top, and overtaken on cost and openness, but the US has not been dethroned.

Where the US still leads. The frontier is still set in America. OpenAI's GPT-5 (August 2025), Anthropic's Claude Opus line, Google DeepMind's Gemini 3 and Meta's Llama 4 anchor the top of every serious capability benchmark, and the US ecosystem — capital, chips, research talent, cloud distribution — remains unmatched. Stanford's AI Index confirms the quantitative edge: 50 notable US models in 2025 against China's 30, and a top-model lead that, while shrunk to ~2.7% on public leaderboards, is still a lead.

Where China has won. China's advantage is speed of deployment, cost efficiency and open-source diffusion. DeepSeek's low-cost, high-performance releases stunned the market in early 2025; Alibaba's Qwen, Zhipu's GLM and Moonshot's Kimi families followed, publishing open weights that anyone can download and run. Chinese open-weight models now account for a large and growing share of global open-model usage. When capability is roughly equal, price and openness decide adoption — and on both, China is ahead.

The policy overhang. Washington is treating Chinese AI as a security problem. The House Select Committee on the CCP branded DeepSeek a "profound threat" in April 2025 and alleged it distilled US models; federal agencies barred it from official devices; and in July 2026 lawmakers sent letters to US companies — including Cursor and Airbnb — probing their use of Chinese models. Beijing is mirroring the posture: through 2026 China's commerce ministry has been in talks with Alibaba, ByteDance and Zhipu about restricting overseas access to its most advanced models. Meanwhile China's State Council "AI Plus" initiative (August 2025) is pushing AI into industry, healthcare and governance with penetration targets above 90% by 2030.

The real bottleneck is physical. Both countries are now constrained by electricity, not ideas. The IEA reports data-centre electricity use rose 17% in 2025, with AI-specific consumption up roughly 50%; global data-centre demand is projected to nearly double from about 485 TWh in 2025 to roughly 950 TWh by 2030 — around 3% of world electricity. Grid connection, not model architecture, is becoming the strategic chokepoint for scaling.

The quantum race: America leads, China scales fastest

Quantum computing crossed a threshold in the last 18 months — literally. The field's central problem is error correction: qubits are fragile, and until recently adding more of them added more noise. "Below-threshold" error correction — where errors fall as the system grows — is the gateway to useful machines.

The US milestones. Google's Willow chip (105 qubits, December 2024) was the landmark: it demonstrated below-threshold error correction, with logical error rates dropping as the code scaled up. IBM continues to execute the most detailed public roadmap in the industry — its 2025 Nighthawk processor and modular Loon/Kookaburra path lead toward "Starling," a large-scale fault-tolerant machine targeted for 2029. On the public markets, IonQ (trapped ions), Rigetti (superconducting) and D-Wave (annealing, now adding a gate-model roadmap) give investors direct, if volatile, exposure.

China's answer. The gap here is closing faster than most expected. USTC's Zuchongzhi 3.0 (105 qubits) matched Google on random-circuit sampling in 2024; its successor, Zuchongzhi 3.2 (107 qubits), reached below-threshold error correction in late 2025 — the first non-US group to hit that milestone. China Telecom's Tianyan-504 fielded a 504-qubit superconducting system, and the neutral-atom Hanyuan-1 (~100 qubits) became China's first commercial quantum computer, booking more than $5 million in orders including an export to Pakistan. China also runs multiple quantum cloud platforms and dominates quantum communication — its fibre QKD network has no US equivalent.

The verdict. The Special Competitive Studies Project's assessment is the fair one: the US retains an overall lead in quantum information science — roughly 300 quantum start-ups to China's 30, plus the deeper industrial and talent base — but China leads decisively in quantum communication and out-spends the US on government funding (an estimated $15 billion versus $6 billion). Beijing named quantum the first of seven "future industries" in its 15th Five-Year Plan (2026–2030), pivoting from research to commercialisation. In Washington, the National Quantum Initiative reauthorisation is moving through Congress but is not yet law.

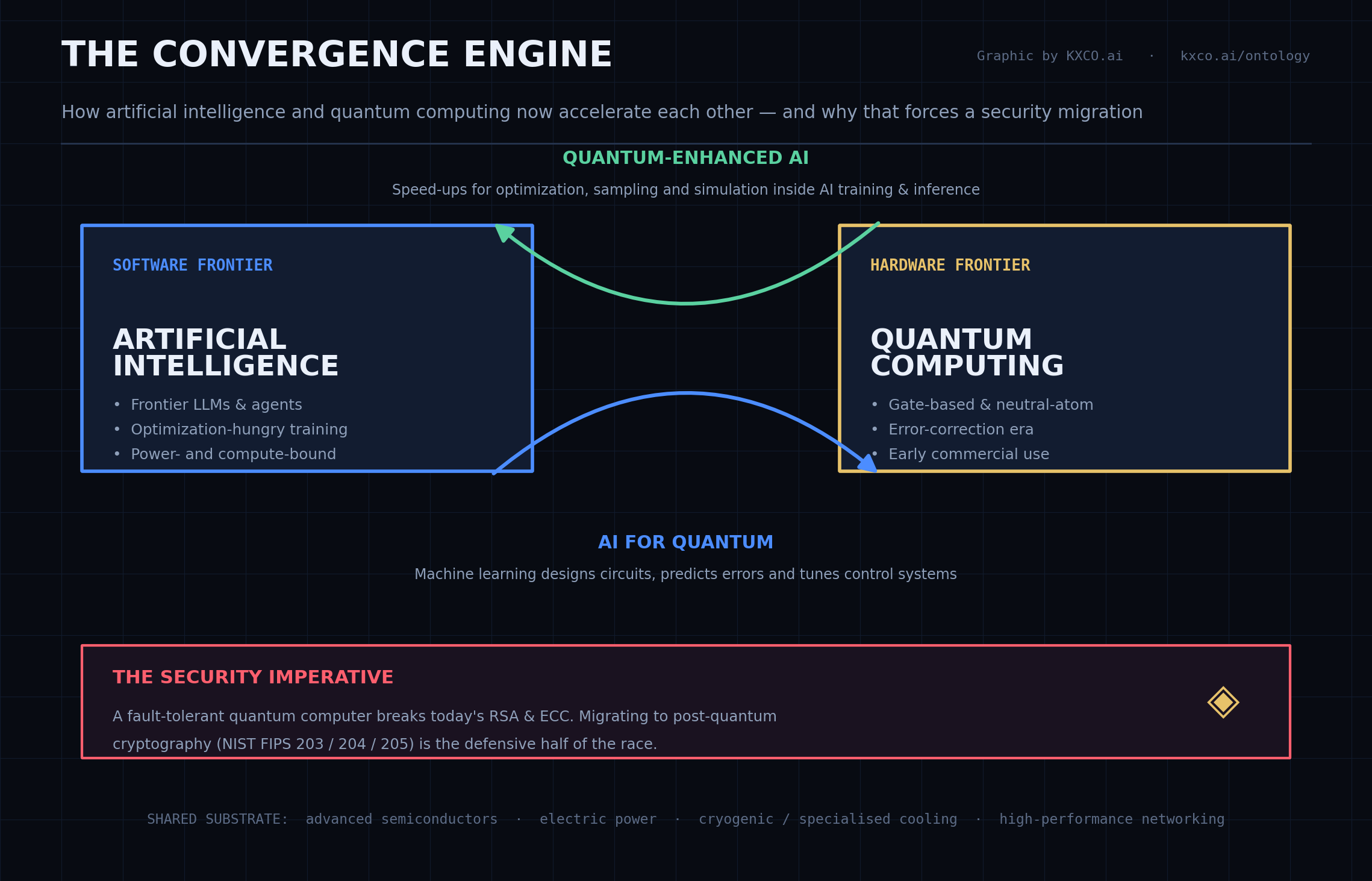

Why AI and quantum are converging

The convergence is not speculative — it is already underway on four fronts.

1. Quantum-enhanced AI. Quantum computers are naturally suited to the optimization and sampling problems that sit at the heart of machine learning. As hardware matures, quantum machine-learning routines could accelerate specific training and inference workloads that are bottlenecks on classical silicon.

2. AI for quantum. The traffic runs both ways. Machine learning is now used to design better quantum circuits, predict and classify error patterns, and tune the control systems that keep qubits stable — compressing the path to fault tolerance.

3. The security imperative. Large AI systems run on vast flows of encrypted data and valuable model IP. A sufficiently large quantum computer breaks the public-key cryptography (RSA, ECC) that protects all of it. That is why NIST finalised its post-quantum cryptography standards — FIPS 203 (ML-KEM), 204 (ML-DSA) and 205 (SLH-DSA) — in August 2024, and why the migration to quantum-resistant, verifiable infrastructure is now a live requirement rather than a research topic. It is the domain KXCO's Sentinel platform is built to address.

4. Infrastructure overlap. Both technologies are power-hungry and depend on the same advanced semiconductors, specialised cooling and high-performance networking. The companies that supply the AI build-out — NVIDIA, TSMC, Broadcom, the memory makers — are frequently the same names positioned to benefit from the quantum one.

The security imperative, in plain terms

The most under-priced risk in this whole story is timing. A cryptographically relevant quantum computer may still be years away, but the threat is present tense: adversaries can capture encrypted data now and decrypt it later, once the hardware exists. Sensitive records with a long shelf life — financial, medical, defence, intellectual property — are exposed the day they are transmitted, not the day quantum arrives.

With NIST's standards finalised, the excuse for delay is gone. Enterprises and critical infrastructure are beginning the multi-year job of inventorying their cryptography and migrating to post-quantum algorithms. Firms that build, verify and secure that transition — the defensive half of the AI-quantum race — are a distinct and growing investment category.

Investment implications

The convergence creates five clear themes: AI infrastructure (chips, data centres, power), quantum hardware and software pure-plays, post-quantum security enablers, cloud platforms that integrate both, and Chinese domestic champions for investors willing to navigate geopolitical risk.

Table 1 — Key US-listed stocks with AI + quantum exposure

Ticker | Company | AI exposure | Quantum exposure | Outlook (12–24m) | Key risks |

|---|---|---|---|---|---|

NVIDIA | Dominant AI GPUs & software | CUDA-Q platform, NVAQC/NVQLink | Very strong | Export controls, competition, valuation | |

Alphabet | Gemini, Google Cloud AI | Quantum AI, Willow chip | Strong | Antitrust, AI monetisation | |

Microsoft | OpenAI partnership, Azure AI | Azure Quantum, Majorana 1 chip | Strong | OpenAI dependency, capex intensity | |

IBM | watsonx enterprise AI | Leading quantum roadmap (Starling 2029) | Moderate–strong | Slower core growth | |

IonQ | Emerging quantum-AI apps | Trapped-ion leader; Tempo sales | High risk / high reward | Pre-revenue economics, dilution | |

Broadcom | Custom AI ASICs (XPUs) | Limited direct | Strong | Customer concentration |

Table 2 — Notable China-related or exposed stocks

Ticker | Company | AI exposure | Quantum / tech exposure | Outlook | Key risks |

|---|---|---|---|---|---|

Alibaba | Qwen open-weight models, cloud | Quantum investment | Moderate (domestic recovery) | Regulation, geopolitics | |

Baidu | Ernie models | Quantum research | Moderate | Open-model competition | |

TSMC | Advanced-node manufacturing | Supplies both US & China | Strong (foundry leader) | Geopolitical (Taiwan) | |

ASML | EUV lithography (critical) | Indirect (enables chips) | Strong but constrained | China export limits (EUV barred; DUV ~19% of sales) |

Prices and multiples move daily; the exposures above are structural, not a snapshot of valuation.

Semiconductor, cloud and infrastructure beneficiaries

NVIDIA ($NVDA) remains the clearest winner from AI scaling and is extending deliberately into quantum software via its CUDA-Q platform and QPU-agnostic tooling. Broadcom ($AVGO) benefits from surging custom-ASIC demand from the hyperscalers; TSMC ($TSM) manufactures the leading-edge silicon both sides depend on; and ASML's ($ASML) EUV monopoly makes it a chokepoint — though its China exposure is now capped by export controls. The cloud majors — Microsoft Azure ($MSFT), Google Cloud ($GOOGL), AWS ($AMZN) — are the natural platforms for hybrid classical-quantum-AI workloads, while power, grid and cooling suppliers ride an indirect but durable tailwind.

The pure-play quantum names ($IONQ, $RGTI, $QBTS) remain speculative and are valued on future potential rather than current revenue. They offer asymmetric upside if commercial milestones accelerate — and outsized drawdowns if they slip.

Risks and valuation considerations

Geopolitical. Tighter US export controls or Chinese retaliation can disrupt supply chains overnight; China's move toward restricting its own model exports could fragment the global AI ecosystem into incompatible blocs.

Technical. Fault-tolerant quantum computing is hard, and quantum-advantage timelines have slipped before. Below-threshold error correction is a milestone, not a finished product.

Valuation. AI leaders trade at premiums that already price in years of growth; quantum pure-plays are priced on narrative. Both are vulnerable to any wobble in the AI capex cycle.

Security. The window to migrate to post-quantum cryptography narrows every year. Organisations that delay are accumulating a liability that compounds silently.

The 12–24 month outlook

Next 12 months: a steady cadence of model releases from both US and Chinese labs; incremental quantum-hardware gains and early commercial use cases in optimization and simulation; and rising regulatory scrutiny on cross-border AI model usage in both capitals.

12–24 months: the first credible demonstrations of quantum advantage on practically useful, AI-adjacent problems; an acceleration of post-quantum cryptography adoption across finance and critical infrastructure; and policy that swings with the state of US-China relations.

Investment stance: favour companies with exposure to both AI infrastructure and quantum-enabling technology, keep an eye on the post-quantum security layer, and hold diversified exposure across US leaders and selective Chinese champions (via ADRs). Size the speculative quantum sleeve to a level you can hold through volatility.

The AI-quantum convergence is one of the defining technological shifts of the decade. The United States holds the advantage in ecosystem depth and several hardware approaches; China's coordinated national strategy and rapid iteration are narrowing those leads front by front. The investors who understand both the opportunities and the security imperatives of this new computing paradigm will be the ones best positioned for what comes next.

By Shayne Heffernan, Founder & CEO, KXCO.

Sources: Stanford HAI 2026 AI Index; US House Select Committee on the CCP; US State Council "AI Plus" Opinions (2025); International Energy Agency, Electricity 2026; Nature (Google Willow, 2024); Physical Review Letters (Zuchongzhi 3.0 / 3.2); China Telecom Quantum Group (Tianyan-504); Chinese Academy of Sciences (Hanyuan-1); IBM Quantum roadmap; Special Competitive Studies Project; NIST FIPS 203/204/205; US Congress (S.3597 / H.R.8462).

This article is for informational purposes only and does not constitute investment advice. Markets and technologies evolve rapidly; readers should conduct their own due diligence.

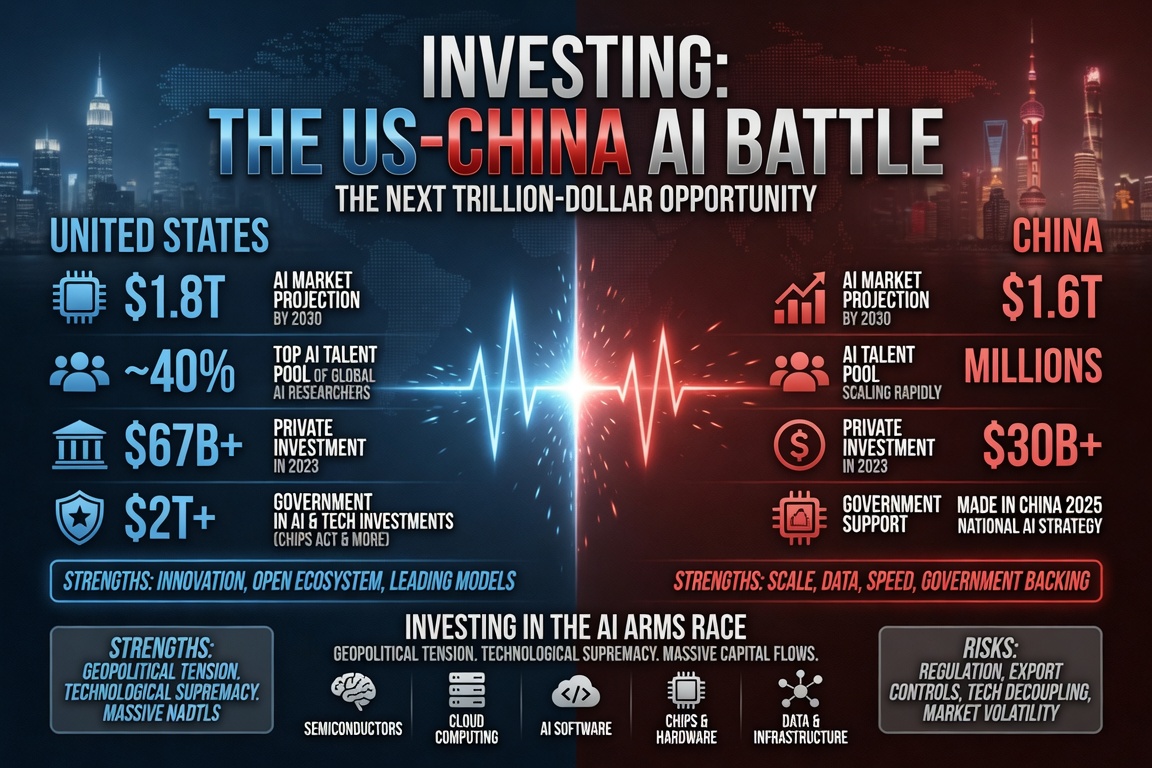

Investing: The US-China AI Battle

US China AI battle investing, decoded: Claude Fable 5 & Opus 4.8 vs GLM-5.2 & Kimi K2.7, the NVIDIA-vs-Huawei chip supply chain, target prices for the best AI stocks to buy in 2026, and a full geopolitical risk matrix. By Shayne Heffernan.

Economic Calendar and Trading Strategies for July 7–11, 2026

A trader's guide to the week of July 7–11, 2026: the US and China economic calendar, the Fed-pivot test after a soft jobs report, and how to trade Nvidia, SpaceX, Bitcoin, the dollar, gold, silver, AI and quantum. Track every release on Live Trading News.

Quantum Computing Hits Commercial Reality

Quantum computing hit commercial reality in 2026: $2B in US foundry funding, Quantinuum's $14B IPO, and violent rallies in IonQ, Rigetti and D-Wave. Shayne Heffernan explains the AI–quantum flywheel, tables the stocks in the space (IONQ, RGTI, QBTS, QUBT, QNT, IBM, GOOGL, MSFT, NVDA, GFS, HON), covers China's LineShine supercomputer, and closes on KXCO's post-quantum solutions.

MANGO Stocks the 2026 Guide

MANGO stocks are the cohort powering the AI infrastructure economy: Meta (META), Anthropic, Nvidia (NVDA), Google/Alphabet (GOOGL), OpenAI and SpaceX (SPCX). Shayne Heffernan defines the term, covers the latest 2026 earnings and IPO filings, and explains why the infrastructure economy is best understood as a graph — with KXCO's Ontology Engine as a key reference.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.