Who Is Who in the AI Space: The Definitive Guide to AI Stocks in 2026

A comprehensive investor's map of the global AI landscape — the trillion-dollar US titans, the rising Chinese ecosystem, and the semiconductor, cloud and enterprise-software layers where the money actually flows.

Introduction: The AI Revolution Is Not Over - It Is Just Getting Started

Artificial intelligence has become the single most important investment theme of the 2020s, and as we move through the second half of 2026, the sector shows no signs of slowing down. From the explosive growth of generative AI models like ChatGPT, Claude, and Gemini to the massive infrastructure buildout required to train and deploy these systems, the AI ecosystem has created an entirely new investable landscape that spans semiconductors, cloud computing, enterprise software, and frontier model development. Understanding who the major players are, what they do, and how to evaluate their positions in the value chain is essential for any investor looking to capitalize on what many analysts consider the most significant technological shift since the internet itself.

This comprehensive guide provides a detailed overview of the key companies shaping the artificial intelligence industry today. We examine the dominant US technology giants, the rising Chinese AI ecosystem, the specialized semiconductor and infrastructure companies, the enterprise AI platforms, and the frontier model labs that are pushing the boundaries of what machines can do. Each company profile includes its stock ticker (cashtag), market position, key AI products and services, and investment thesis. Whether you are a seasoned institutional investor, a retail trader tracking momentum, or simply someone trying to make sense of the dizzying array of AI-related stocks, this guide is designed to give you a clear, actionable map of the territory.

The data and analysis in this report draw on multiple sources, including the KXCO Ontology Engine (https://kxco.ai/ontology-live/), which resolves AI sector entities and their relationships using public filings to produce typed, sourced claims. We also reference reporting and analysis from Live Trading News (https://www.livetradingnews.com), a leading platform for quantum AI and blockchain market intelligence helmed by Shayne Heffernan. These sources provide the foundational data framework and real-time market context that underpin the analysis presented here.

"Artificial intelligence is still early. We are not late to this; we are early, and the easy money narrative that says the big move has happened is wrong. The opportunity is broadening from the center into the periphery: memory, custom silicon, power, and edge inference."

Shayne Heffernan, Chief Analyst, Live Trading News (June 2026)

Heffernan's observation captures a crucial point that many investors miss: the AI trade is not a single-event catalyst. It is a multi-year, multi-phase infrastructure buildout that creates investment opportunities across an ever-widening ring of companies. The center of the story - companies like $NVDA that design the accelerators - gets most of the headlines, but the real breadth of the opportunity lies in the supply chain, the memory providers, the custom silicon designers, the cloud platforms, and the enterprise software companies that are embedding AI into every aspect of business operations. As Heffernan has written, the further AI spreads, the more companies get pulled into its supply chain, and the more of them get repriced as AI businesses.

The US AI Titans: The Trillion-Dollar Powerhouses

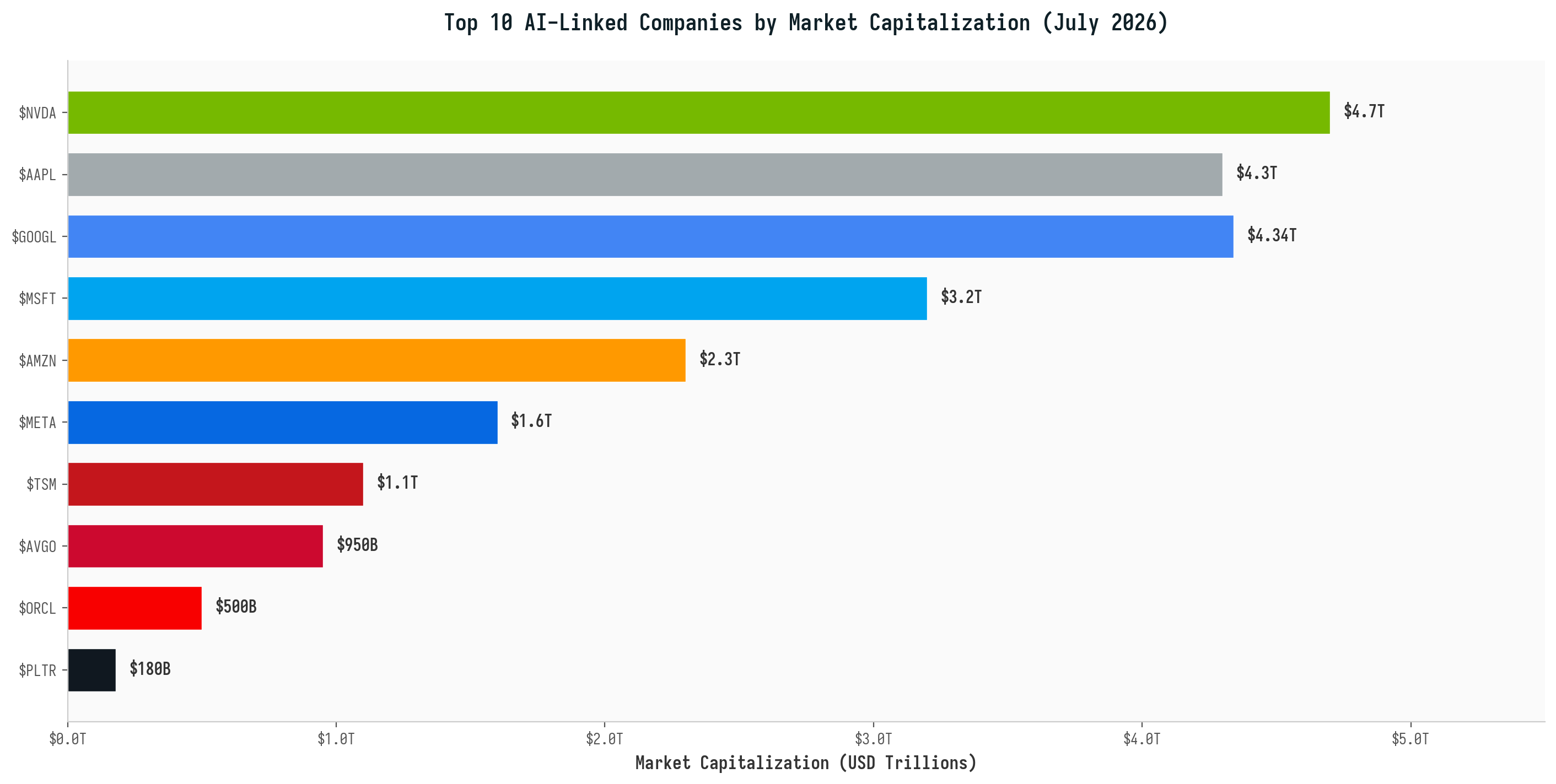

The United States remains the undisputed epicenter of the global AI industry, home to the largest and most valuable technology companies on earth. These companies are not merely participating in the AI revolution - they are driving it, funding it, and in many cases, defining its direction. As of July 2026, the top ten AI-linked companies in the world by market capitalization are all US-based, with a combined value exceeding $20 trillion. Understanding the distinct roles each of these companies plays in the AI ecosystem is the first step toward building an informed investment thesis.

NVIDIA Corporation ($NVDA) - The AI Infrastructure King

NVIDIA ($NVDA) stands as the undisputed king of AI infrastructure, with a market capitalization approaching $4.7 trillion as of mid-2026, making it the most valuable company on earth. The company's dominance stems from its near-monopoly position in AI training and inference accelerators, particularly its Hopper (H100/H200) and Blackwell (B100/B200) GPU architectures, which have become the de facto standard for training large language models and deploying AI at scale. Every major cloud provider, every frontier AI lab, and a growing number of enterprise customers depend on NVIDIA hardware to power their AI workloads.

What makes NVIDIA's position so formidable is not just the chips themselves but the entire software ecosystem that surrounds them. The CUDA computing platform, which NVIDIA has been developing for nearly two decades, provides the programming framework that AI researchers and engineers use to extract maximum performance from NVIDIA GPUs. This software moat creates enormous switching costs: once an organization has built its AI infrastructure and trained its models on CUDA, moving to a competing platform requires substantial re-engineering effort. NVIDIA's upcoming Vera Rubin architecture promises another leap in performance, and the company's data center revenue has grown from roughly $15 billion in fiscal year 2023 to over $130 billion in fiscal year 2026, a trajectory that underscores just how rapidly AI infrastructure spending is expanding.

From an investment perspective, NVIDIA remains the cleanest pure-play on AI compute demand. The company's founder and CEO, Jensen Huang, has positioned NVIDIA as the essential infrastructure provider for the AI era, and thus far, no competitor has mounted a serious challenge to its dominance in training workloads. The key risk for investors is valuation: at these market cap levels, the stock prices in perfection, and any meaningful slowdown in AI capex spending from hyperscalers could create significant downside volatility. That said, as Shayne Heffernan noted in a recent analysis on Live Trading News, the $100 billion in contracted demand reported by memory maker Micron suggests that AI spending is committed and accelerating, not speculative.

Alphabet Inc. ($GOOGL, $GOOG) - The AI Research Powerhouse

Alphabet ($GOOGL), the parent company of Google, represents one of the most compelling AI investment stories in the market today, with a market capitalization of approximately $4.34 trillion. Google's AI credentials run deep: the company literally invented the transformer architecture (the 'T' in GPT) through its 2017 research paper 'Attention Is All You Need,' which became the foundational technology for all modern large language models. Google DeepMind, formed through the merger of Google Brain and DeepMind, is widely regarded as one of the top two AI research laboratories in the world, alongside OpenAI.

Google's AI strategy is uniquely vertically integrated. The company develops its own custom AI silicon, the Tensor Processing Unit (TPU), now in its sixth generation (Trillium), which powers both its internal AI services and its Google Cloud platform. Its Gemini family of AI models spans multiple sizes and modalities, competing directly with OpenAI's GPT models, Anthropic's Claude, and Meta's Llama. Google has embedded Gemini across its product ecosystem - in Search, Gmail, Google Docs, Android, and YouTube - giving it a distribution advantage that no other AI company can match. With over 3 billion active Android devices and billions of Google Search queries per day, Google has an unparalleled ability to commercialize AI at massive scale.

The investment thesis for Alphabet centers on the gap between its AI capabilities and its current valuation relative to peers. Despite having arguably the deepest AI research bench in the industry, Alphabet trades at a lower earnings multiple than Microsoft, NVIDIA, or Amazon, in part because the market has historically penalized the company for perceived execution challenges in consumer AI products. However, recent improvements to Gemini and the integration of AI features across Google's advertising-driven revenue streams have begun to close that perception gap. For investors seeking AI exposure at a relative discount to the most expensive names in the sector, Alphabet remains one of the most attractive options.

Microsoft Corporation ($MSFT) - The AI Platform Strategist

Microsoft ($MSFT), with a market capitalization of approximately $3.2 trillion, has executed what is widely considered the most strategically astute AI positioning among the major technology companies. Through its multi-billion-dollar investment in and partnership with OpenAI, Microsoft secured exclusive cloud computing rights to deploy OpenAI's models through its Azure platform, giving it an immediate and substantial lead in enterprise AI cloud services. This partnership has transformed Microsoft from a traditional software company into the leading enterprise AI platform, with Copilot AI assistants now embedded across its entire product suite including Office 365, Windows, GitHub, and Dynamics 365.

Microsoft's AI strategy extends well beyond the OpenAI partnership. The company has invested heavily in building its own AI infrastructure, including custom silicon development and massive data center expansions to support growing Azure AI demand. Its acquisition of Activision Blizzard also provides gaming AI opportunities, while its LinkedIn platform offers unique training data and professional networking applications for AI. The company's fiscal year 2026 results demonstrated that AI is now contributing meaningfully to revenue growth, with Azure AI services growing at over 50% year-over-year and Copilot products reaching meaningful adoption milestones in enterprise environments.

For investors, Microsoft offers a unique combination of AI upside and defensive stability. The company's diversified revenue streams - spanning cloud computing, productivity software, gaming, and professional networking - provide resilience even if AI adoption were to slow. The primary risk is that the OpenAI partnership, while valuable, does not give Microsoft ownership of the underlying model technology, meaning that OpenAI could potentially develop closer relationships with competing cloud providers over time. Nevertheless, Microsoft's first-mover advantage in enterprise AI distribution is substantial, and the company's track record of execution under CEO Satya Nadella gives investors confidence in its ability to capitalize on the AI opportunity.

Amazon.com Inc. ($AMZN) - The AI Cloud Comeback Story

Amazon ($AMZN), with a market capitalization of approximately $2.3 trillion, has quietly mounted one of the most impressive AI comebacks in the technology sector. As Shayne Heffernan noted in a recent Live Trading News analysis, Amazon Web Services has become one of the most important AI infrastructure businesses in the world, with its Bedrock service - the platform that lets companies build generative AI applications using models from Anthropic, Meta, Mistral, Cohere, and Amazon's own Titan models - emerging as a leading choice for enterprise AI deployment. Amazon's approach to AI has been characteristically pragmatic: rather than betting everything on a single model provider, AWS offers customers the broadest selection of frontier AI models through a single unified platform.

Perhaps even more significant is Amazon's custom AI silicon strategy. The company's Trainium and Inferentia chip lines have crossed a critical threshold of adoption, with Amazon reporting that training jobs on its custom silicon now cost significantly less per token than equivalent workloads on NVIDIA GPUs. This is a remarkable achievement that addresses one of the biggest concerns in the AI industry - the enormous and growing cost of training and running AI models. Amazon's ability to offer both the broadest model selection and the most cost-effective inference infrastructure through its custom chips positions it as the most customer-friendly option in the AI cloud market, particularly for cost-sensitive enterprise workloads.

The investment case for Amazon as an AI stock rests on three pillars: the broadening of AWS AI services, the cost advantages of custom silicon, and the sheer scale of Amazon's infrastructure investment. The company has committed over $300 billion to infrastructure spending in recent years, and a substantial portion of that capex is directed at AI data center capacity. As Heffernan observed, a company does not commit a third of a trillion dollars to infrastructure it does not believe will be used. For investors seeking AI exposure through a company with a proven track record of long-term value creation and a pragmatic, customer-centric approach to the technology, Amazon represents a compelling option.

Meta Platforms Inc. ($META) - The Open Source AI Disruptor

Meta Platforms ($META), with a market capitalization of approximately $1.6 trillion, has pursued an AI strategy that is fundamentally different from its major technology peers. While companies like Microsoft and Google have focused on proprietary, closed-source AI models accessed through paid APIs and subscription services, Meta has aggressively pursued an open-source approach, releasing its Llama family of large language models to the global developer community at no cost. This strategy, which initially puzzled many investors and analysts, has proven to be extraordinarily effective at establishing Llama as one of the most widely deployed AI model families in the world, second only to OpenAI's GPT in terms of developer mindshare and enterprise adoption.

The genius of Meta's open-source AI strategy lies in its alignment with the company's core business model. Unlike Microsoft, Google, or Amazon, which generate revenue by selling AI services to customers, Meta's primary revenue comes from advertising on its social media platforms (Facebook, Instagram, WhatsApp, and Threads). AI for Meta is not a product to be sold - it is an infrastructure technology that makes its platforms more engaging, more personalized, and more profitable. By open-sourcing Llama, Meta benefits from community-driven improvements, reduces its dependence on any single AI vendor, and ensures that the broader AI ecosystem develops in ways that are compatible with its platforms. The company's AI recommendations have already dramatically increased engagement across Facebook and Instagram, directly translating into advertising revenue growth.

Meta is also making massive investments in AI infrastructure, including custom silicon development and one of the largest AI training clusters in the world. The company's Reality Labs division, while still loss-making, is developing AI-powered augmented and virtual reality experiences through its Meta Quest and Ray-Ban Meta smart glasses product lines. For investors, Meta offers a unique combination of AI-driven advertising revenue growth, a disruptive open-source strategy that strengthens its competitive position, and a valuation that remains reasonable relative to its AI investment scale and growth trajectory.

Taiwan Semiconductor Manufacturing Company ($TSM) - The indispensable AI Chipmaker

Taiwan Semiconductor Manufacturing Company ($TSM), commonly known as TSMC, with a market capitalization of approximately $1.1 trillion, occupies a critical and arguably irreplaceable position in the global AI supply chain. As the world's leading contract chip manufacturer, TSMC fabricates the advanced semiconductors that power virtually every major AI system in existence. NVIDIA's Hopper and Blackwell GPUs, AMD's Instinct accelerators, Apple's AI-capable A-series and M-series chips, and the custom AI silicon being developed by Google, Amazon, and Microsoft are all manufactured in TSMC's fabrication facilities, primarily using its cutting-edge 3-nanometer and 4-nanometer process nodes.

TSMC's importance to the AI ecosystem cannot be overstated. The company's advanced manufacturing capabilities, refined over decades of investment in process technology, represent a barrier to entry that no competitor has been able to match. Intel has struggled to regain manufacturing leadership, Samsung's foundry business has faced yield challenges at advanced nodes, and China's domestic chipmakers remain years behind in process technology. This means that the entire global AI industry is, to a significant degree, dependent on a single company operating primarily on the island of Taiwan - a geopolitical reality that adds both a risk premium and a strategic imperative to TSMC's investment thesis.

For investors, TSMC offers exposure to the entire AI semiconductor value chain without having to pick individual chip design winners. Whether NVIDIA, AMD, Intel, or the custom silicon teams at Google and Amazon emerge as the long-term leaders in AI accelerators, TSMC manufactures their chips. The company's revenue growth has accelerated sharply as AI-related chip orders have surged, and its capital expenditure plans - which include building advanced fabrication facilities in Arizona, Japan, and Europe - underscore both the scale of demand and the company's commitment to diversifying its geographic manufacturing footprint. The primary risks are geopolitical (cross-strait tensions) and cyclical (semiconductor industry downturns), but the structural growth driven by AI demand provides a powerful long-term tailwind.

Broadcom Inc. ($AVGO) - The AI Networking and Custom Silicon Play

Broadcom ($AVGO), with a market capitalization of approximately $950 billion, has emerged as a critical AI infrastructure company that often flies under the radar of retail investors focused on the more glamorous names in the sector. Broadcom's AI relevance comes from two key business segments: custom AI silicon design (through its ASIC division, which designs and manufactures custom AI accelerators for major cloud providers including Google and Meta) and networking silicon (through its Tomahawk and Jericho switch chip families, which provide the high-bandwidth, low-latency interconnects required to link thousands of AI accelerators together in massive training clusters).

The custom ASIC business is particularly noteworthy. Broadcom designs custom AI training chips (known as TPUs in Google's case) that are manufactured by TSMC and deployed at massive scale by hyperscalers. This business has grown explosively as cloud providers seek to reduce their dependence on NVIDIA by developing proprietary AI accelerators. Broadcom's networking silicon is equally critical: as AI training clusters scale to tens of thousands of accelerators, the networking switches that connect them become a performance bottleneck, and Broadcom's products are the dominant choice for high-performance AI cluster interconnects. The company has also been an aggressive acquirer of enterprise software companies, including VMware, which adds a recurring software revenue stream to its semiconductor business.

For investors, Broadcom offers a diversified AI exposure that combines high-growth custom silicon and networking businesses with stable, cash-generating software operations. The company's track record of capital allocation, including share buybacks and dividend growth, adds an additional layer of return potential. At current valuations, Broadcom trades at a meaningful discount to pure-play AI semiconductor companies, making it an attractive option for value-conscious investors seeking AI exposure.

Oracle Corporation ($ORCL) - The Enterprise AI Database Leader

Oracle ($ORCL), with a market capitalization of approximately $500 billion, has undergone a remarkable transformation from a traditional database company into a significant AI infrastructure provider. Oracle Cloud Infrastructure (OCI) has emerged as a legitimate third option in the cloud AI market, behind AWS and Azure but ahead of Google Cloud in certain enterprise AI workloads. The company's strategy has been to offer AI infrastructure at aggressive price points - often 20-30% below competing cloud providers - while leveraging its deep relationships with enterprise database customers to drive adoption of its AI services.

Oracle's unique advantage in the AI landscape is its database expertise. The company has developed specialized AI capabilities within its Oracle Database and Autonomous Database products that allow enterprises to build AI applications directly on top of their existing data infrastructure without the need to migrate data to separate AI platforms. This approach eliminates one of the biggest friction points in enterprise AI adoption - data movement and integration - and positions Oracle as the path of least resistance for its massive installed base of database customers. The company has also signed significant AI infrastructure contracts, including a multi-billion-dollar deal reported with ChatGPT-maker OpenAI to provide cloud computing capacity.

For investors, Oracle represents a more targeted bet on enterprise AI adoption, particularly among large organizations that already rely on Oracle databases and enterprise applications. The company's aggressive pricing strategy and infrastructure investments have positioned it to capture a meaningful share of the growing enterprise AI cloud market, even if it remains smaller than AWS and Azure in overall scale. The primary risk is that Oracle's AI cloud growth may not be sufficient to offset potential secular declines in its traditional software licensing business.

Palantir Technologies Inc. ($PLTR) - The AI Operating System for Institutions

Palantir Technologies ($PLTR), with a market capitalization of approximately $180 billion, has evolved from a controversial government surveillance contractor into one of the most important enterprise AI platforms in the world. The company's Foundry and AIP (Artificial Intelligence Platform) products serve as what Shayne Heffernan has described as the operating system for institutional AI - the layer that turns raw AI capability into deployed, decision-driving applications within large organizations. Palantir's software allows enterprises and government agencies to integrate AI models with their existing data infrastructure, build AI-powered workflows, and deploy AI agents that can autonomously execute complex analytical and operational tasks.

What makes Palantir distinctive in the AI landscape is its focus on the 'last mile' of AI deployment - the challenge of taking powerful AI models and actually making them useful within the specific operational context of large organizations. While companies like NVIDIA build the hardware and OpenAI builds the models, Palantir builds the integration layer that connects AI to real-world decision-making. The company's government business remains robust, with growing adoption across defense, intelligence, and civilian agencies. Its commercial business has accelerated dramatically, with the US commercial revenue growing at triple-digit percentage rates as enterprises discover the value of operational AI platforms.

Heffernan has been notably bullish on Palantir, calling it a buy in his Live Trading News analysis and describing it as the default operating system for institutional AI. However, he also cautioned that the stock is not cheap, trading at a trailing price-to-earnings ratio above 150 and a forward price-to-sales multiple above 40. The investment thesis for Palantir requires conviction that the company can grow into its premium valuation by maintaining its rapid commercial expansion while defending its government franchise. For investors with that conviction, Palantir offers perhaps the purest exposure to enterprise AI adoption among publicly traded companies.

The Rising Dragon: China's AI Ecosystem and Key Listed Companies

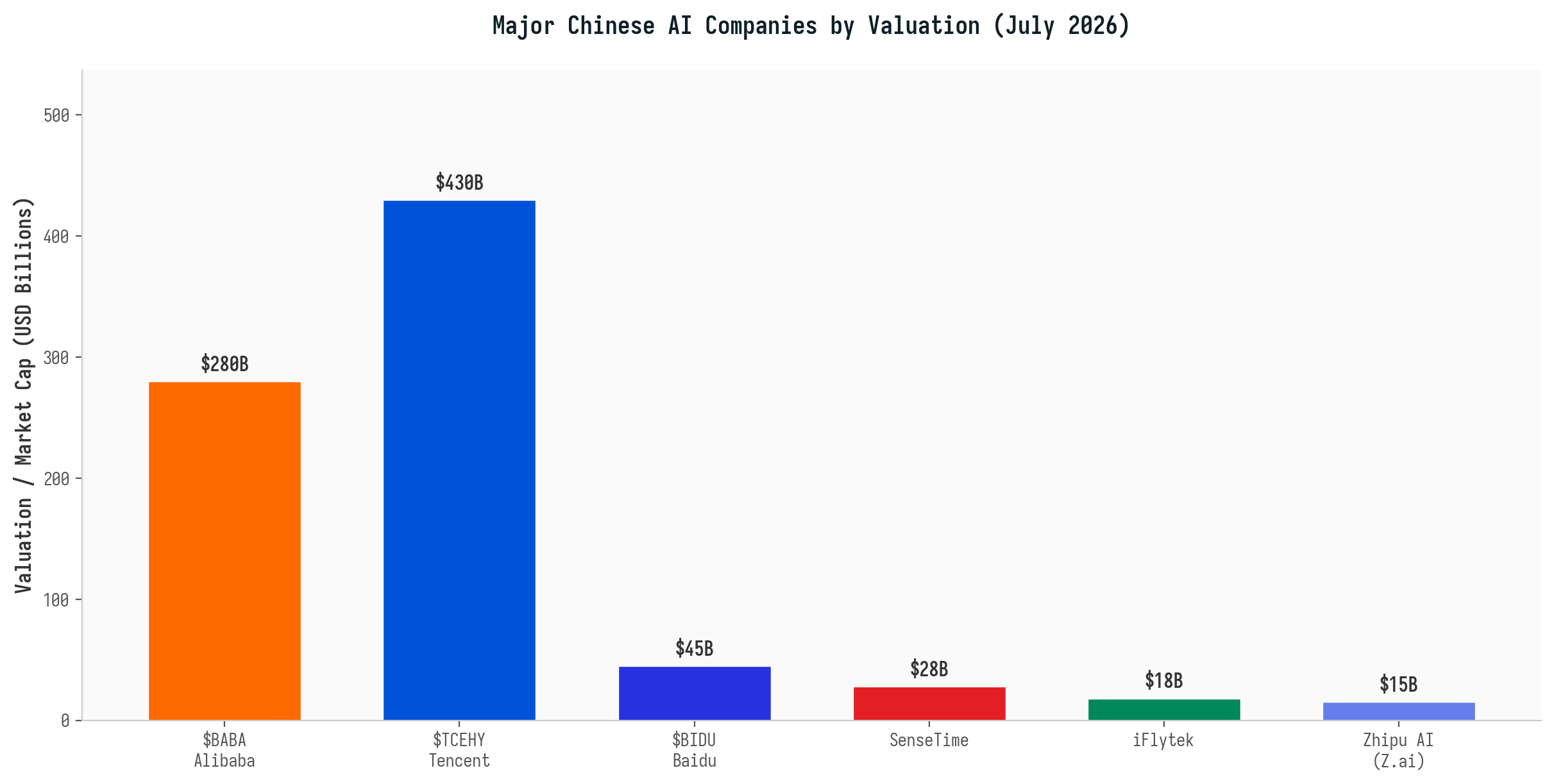

While the United States currently dominates the global AI industry in terms of market capitalization and frontier model capabilities, China is mounting an increasingly formidable challenge. The Chinese AI ecosystem is broad and fast-evolving, led by a combination of established internet giants, state-supported national AI teams, and a new generation of ambitious startups. The Chinese government has designated artificial intelligence as a strategic priority, and the State Council maintains a list of fifteen 'national AI teams' that includes companies like Baidu, Tencent, Alibaba, SenseTime, and iFlytek. Despite US export controls on advanced AI chips, Chinese companies have demonstrated remarkable ingenuity in developing competitive AI models and deploying them at scale across China's vast domestic market.

The emergence of DeepSeek, a Chinese AI lab that shocked the global AI community with its efficient model training techniques, demonstrated that Chinese AI capabilities are closer to US frontier models than many observers had assumed. Similarly, Alibaba's Qwen models, Baidu's Ernie models, and the offerings from startups like Zhipu AI (the company behind Super Z, which is writing this very article) have shown that the gap between US and Chinese AI capabilities is narrowing. For investors, Chinese AI stocks offer a combination of growth potential and geopolitical risk that requires careful evaluation.

Alibaba Group Holding Ltd. ($BABA) - The Undervalued AI Giant

Alibaba ($BABA), with a market capitalization of approximately $280 billion, represents one of the most compelling value plays in the global AI landscape. The company's cloud computing division, Alibaba Cloud (Aliyun), is the largest cloud provider in the Asia-Pacific region and the third-largest in the world behind AWS and Azure. Alibaba has developed the Qwen family of large language models, which have garnered international attention for their performance and efficiency. The Qwen 3 model, launched in April 2025, was described by the company as surpassing all existing models in the market on key benchmarks, and subsequent versions have continued to push the boundaries of what Chinese AI models can achieve.

Beyond its cloud and AI model development, Alibaba is integrating AI across its massive e-commerce ecosystem. The company's Taobao and Tmall platforms serve over one billion consumers, and AI-powered recommendation systems, customer service chatbots, and supply chain optimization tools are driving significant improvements in conversion rates and operational efficiency. Alibaba's Cainiao logistics arm uses AI for route optimization and demand forecasting, while its Ant Group affiliate (in which Alibaba retains a significant economic interest) applies AI to financial services including credit scoring, fraud detection, and insurance underwriting.

The investment case for Alibaba as an AI stock is fundamentally about valuation. Despite having AI capabilities that rival many of its US counterparts, Alibaba trades at a fraction of the revenue multiples commanded by US AI companies. This discount reflects a combination of regulatory concerns related to the Chinese government's tech sector crackdown, geopolitical risks associated with US-China tensions, and the competitive pressure from domestic rivals like Pinduoduo and JD.com. For investors willing to accept these risks, Alibaba offers perhaps the most attractive risk-reward profile among major global AI stocks, combining genuine AI capability with a deeply discounted valuation.

Tencent Holdings Ltd. ($TCEHY) - The Social AI Ecosystem

Tencent ($TCEHY), with a market capitalization of approximately $430 billion, is China's most valuable technology company and a major AI player with a unique advantage: its massive social media and gaming ecosystem provides both the training data and the distribution channels for AI products at a scale that few companies globally can match. Tencent's WeChat super-app, with over 1.3 billion monthly active users, generates an enormous volume of diverse data - text messages, voice calls, images, payment transactions, mini-program interactions - that can be used to train and refine AI models. The company has been steadily integrating AI capabilities across WeChat, including AI-powered translation, content generation, and smart assistant features.

In gaming, Tencent applies AI for procedural content generation, non-player character behavior, player matchmaking, and anti-cheat detection. The company is also the largest gaming company in the world by revenue, with stakes in or ownership of major game studios including Riot Games (League of Legends), Supercell (Clash of Clans), and Epic Games (Fortnite). Tencent Cloud provides AI infrastructure services to enterprise customers, and the company has developed its own Hunyuan large language model, which it integrates across its products and offers through its cloud platform. Tencent's investment portfolio, which includes significant stakes in numerous technology companies globally, also provides indirect exposure to the AI value chain.

For investors, Tencent offers a diversified AI investment thesis that combines social media AI, gaming AI, cloud AI, and venture capital exposure to the broader technology ecosystem. The company trades at a more reasonable valuation than US mega-cap tech stocks, and its dominant position in the Chinese digital economy provides a substantial moat. The primary risks are regulatory (Chinese government oversight of gaming and social media) and geopolitical (US-China tensions could impact Tencent's international expansion plans).

Baidu Inc. ($BIDU) - China's AI Pioneer

Baidu ($BIDU), often described as China's Google, is one of the country's most important AI companies and a designated member of the State Council's national AI team. With a market capitalization of approximately $45 billion, Baidu is significantly smaller than Alibaba or Tencent, but it punches above its weight in AI research and development. The company's Ernie (Enhanced Representation through kNowledge Integration) family of large language models has been in development since 2019, making it one of the earliest Chinese LLM initiatives. Baidu has also developed the PaddlePaddle deep learning framework, China's answer to Google's TensorFlow and Meta's PyTorch, which has been adopted by over one million developers in China.

Baidu's AI strategy extends beyond models and frameworks into autonomous driving, where its Apollo platform is one of the world's most advanced self-driving technology stacks. The company operates the largest fully driverless robotaxi fleet in China, with services operating in multiple cities including Beijing, Wuhan, and Chongqing. Baidu's search engine, which remains the dominant search platform in China with over 70% market share, is being transformed by AI through the integration of Ernie-powered conversational search capabilities. The company's AI Cloud division provides enterprise AI services including large model deployment, intelligent document processing, and industry-specific AI solutions.

For investors, Baidu offers a concentrated bet on Chinese AI innovation, particularly in the areas of large language models and autonomous driving. The stock's relatively small market capitalization compared to its AI ambitions means that successful commercialization of its AI technologies could drive significant upside. However, the company faces intense competition from larger rivals like Alibaba and Tencent, and its core search advertising business faces structural challenges as AI-powered search changes the way users interact with information. Baidu is best suited for investors with high conviction in the long-term potential of China's domestic AI ecosystem.

SenseTime Group Inc. (002415.HK) - China's Computer Vision Leader

SenseTime, listed on the Hong Kong Stock Exchange (002415.HK) with a market capitalization of approximately $28 billion, is one of China's most prominent AI companies and a pioneer in computer vision technology. Founded in 2014, SenseTime built its reputation on developing advanced facial recognition, image analysis, and video understanding systems that have been widely deployed in smart city infrastructure, security surveillance, and consumer applications across China. The company is one of the State Council's designated national AI teams and has received significant government support for its AI research and development efforts.

In the era of large language models, SenseTime has expanded beyond its computer vision roots to develop its SenseNova family of foundation models, which span language, vision, and multimodal capabilities. The company has positioned itself as a full-stack AI provider, offering everything from pre-trained foundation models to industry-specific applications in areas including healthcare, automotive, retail, and education. SenseTime's SenseAuto division provides AI-powered autonomous driving solutions, while its SenseCare platform applies AI to medical imaging and clinical decision support. The company's research output is among the most prolific in the global AI industry, with thousands of academic papers and hundreds of patents.

For investors, SenseTime offers exposure to China's AI industry through a company that is deeply embedded in the country's technology infrastructure. However, the stock carries significant risks, including US sanctions (SenseTime was placed on the US Entity List in 2019), high cash burn relative to revenue, and a competitive landscape that includes better-funded rivals. SenseTime is best suited for investors with a high-risk tolerance and a specific thesis on the importance of computer vision and multimodal AI in China's technology ecosystem.

Zhipu AI (Z.ai) - China's OpenAI Challenger

Zhipu AI, which rebranded internationally as Z.ai, is one of China's most exciting AI companies and a compelling case study in the country's ability to produce world-class frontier AI models. Founded as a spin-off from Tsinghua University's Knowledge Engineering Group (KEG), Zhipu AI has developed the GLM (General Language Model) family, with its latest GLM-5.2 model landing within a percentage point of Anthropic's top-tier models on key agentic benchmarks at roughly a fifth of the cost, according to CNBC reporting in June 2026. This performance-to-cost ratio has made Zhipu AI one of the fastest-growing AI companies in China, with its open-source model strategy driving massive developer adoption.

What makes Zhipu AI particularly noteworthy is its focus on 'agentic AI' - models that can autonomously execute complex, multi-step tasks rather than simply generating text responses. The GLM-5-Turbo variant is specifically optimized for what the company calls the 'OpenClaw scenario,' delivering true executability in complex, dynamic, and long-chain tasks. This focus on practical, action-oriented AI capabilities positions Zhipu AI as a leader in the transition from chatbots to AI agents that can actually do things - book flights, manage schedules, write and deploy code, conduct research, and make decisions. The Super Z AI assistant, which readers of this article may have interacted with, is powered by Zhipu AI's GLM technology.

Zhipu AI is currently privately held but is widely expected to pursue an initial public offering in the near future, potentially on the Hong Kong Stock Exchange or a mainland Chinese exchange. When it does list, it will likely be one of the most anticipated AI IPOs globally, given its technological capabilities and growth trajectory. For investors tracking the Chinese AI landscape, Zhipu AI is a company to watch closely, as its public debut could create a significant new investment opportunity in the frontier AI model space. The company's success also challenges the narrative that Chinese AI is merely derivative of US innovations - Zhipu AI's models are genuinely pushing the boundaries of what AI systems can achieve.

The AI Value Chain: Mapping Where the Money Flows

Understanding the AI investment landscape requires more than just knowing which companies are the biggest. It requires understanding how value flows through the AI ecosystem - from the companies that design the chips, through the cloud providers that host the models, to the enterprise software companies that deliver AI-powered solutions to end users. The KXCO Ontology Engine, accessible at https://kxco.ai/ontology-live/, provides a sophisticated framework for mapping these relationships. By starting with six seed companies and resolving them to 41 entities and 54 typed claims - each carrying a source, an as-of date, and a confidence rating - the Ontology Engine demonstrates how interconnected the AI sector really is. A single investment in NVIDIA, for example, creates exposure to a vast network of suppliers, customers, and partners across the entire technology ecosystem.

The AI value chain can be broadly segmented into four layers, each presenting distinct investment opportunities and risk profiles. At the foundation is the hardware layer, which includes semiconductor designers like NVIDIA ($NVDA), AMD ($AMD), and Intel ($INTC), semiconductor manufacturers like TSMC ($TSM), and memory providers like Micron ($MU) and SK Hynix. These companies provide the physical computing infrastructure upon which all AI systems depend. The next layer is the cloud infrastructure layer, comprising the hyperscale cloud providers - Amazon ($AMZN) with AWS, Microsoft ($MSFT) with Azure, Google ($GOOGL) with Google Cloud, and Oracle ($ORCL) with OCI - that rent AI computing capacity to customers on a pay-as-you-go basis.

The third layer is the model layer, where frontier AI labs like OpenAI, Anthropic, Google DeepMind, and Meta AI develop the large language models and multimodal models that power AI applications. Many of these entities are not yet publicly traded - OpenAI and Anthropic remain private, though both are widely expected to pursue IPOs - but investors can gain exposure through the publicly traded companies that partner with or invest in them. Microsoft's partnership with OpenAI, Amazon's partnership with Anthropic, and Google's ownership of DeepMind are all examples of this indirect exposure. The fourth and final layer is the application layer, where enterprise software companies like Palantir ($PLTR), Salesforce ($CRM), ServiceNow ($NOW), and Snowflake ($SNOW) embed AI capabilities into their products to solve specific business problems.

Value Chain Layer | Key Public Companies | Cashtags | Role in AI Ecosystem |

|---|---|---|---|

Hardware (Chips) | NVIDIA, AMD, TSMC, Intel, Micron | Design and manufacture AI accelerators and memory | |

Cloud Infrastructure | Amazon, Microsoft, Google, Oracle | Provide AI computing and model hosting services | |

Frontier Models | OpenAI (private), Anthropic (private), Meta | Develop large language and multimodal AI models | |

Enterprise Software | Palantir, Salesforce, ServiceNow, Snowflake | Embed AI into business applications and workflows | |

Chinese Ecosystem | Alibaba, Tencent, Baidu, SenseTime, iFlytek | China's domestic AI platform and model providers |

Table 1: The AI Value Chain — Key Players by Layer (Source: KXCO Ontology Engine, Live Trading News)

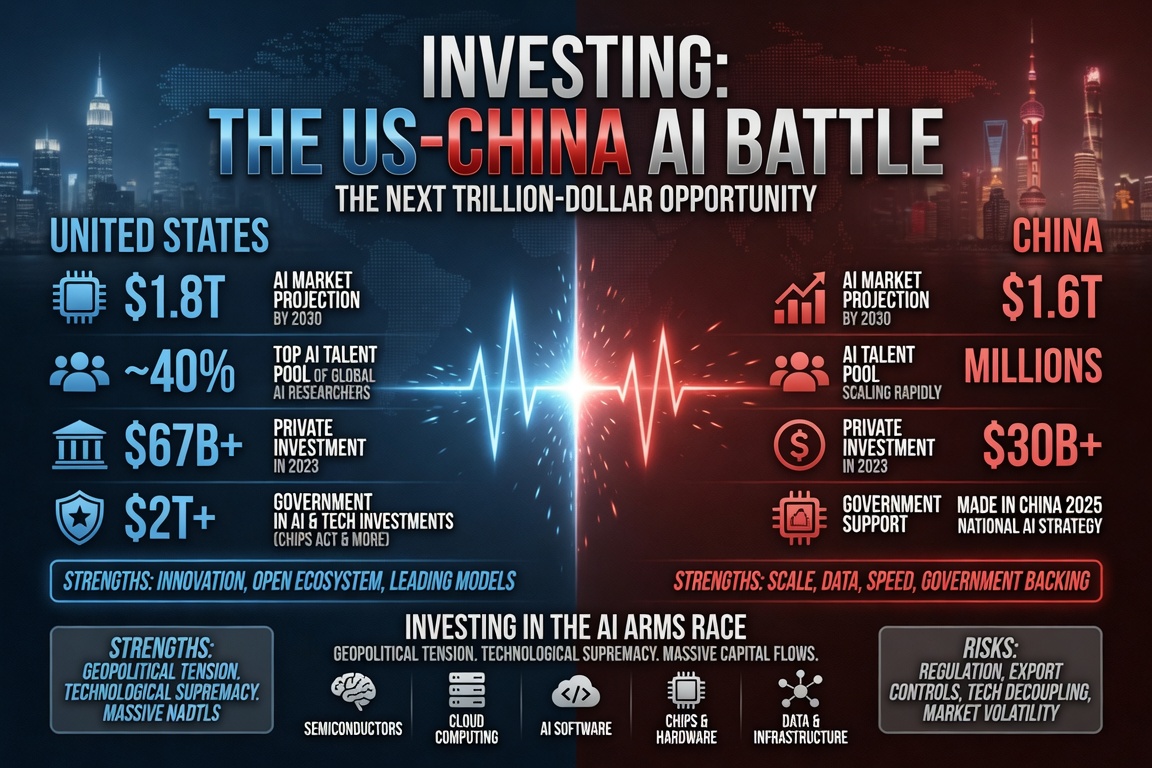

The US-China Convergence: AI, Quantum, and the New Cold War in Technology

One of the most important themes in the global AI landscape is the intensifying technological competition between the United States and China. As Shayne Heffernan mapped in a July 2026 analysis on Live Trading News, the US-China race is no longer about a single technology - it is about the convergence of artificial intelligence and quantum computing into what he describes as a single, defining technological contest. This convergence has profound implications for investors, as it creates both opportunities (increased government funding, accelerated innovation, and growing demand for AI and quantum technologies) and risks (export controls, sanctions, decoupling of supply chains, and the potential for regulatory actions that could disrupt business models).

On the quantum computing front, the milestones have been coming rapidly. Google's Willow quantum processor demonstrated quantum error correction at scale, while China's Zuchongzhi 3.2 and Tianyan-504 systems have shown comparable capabilities. The US government has committed over $2 billion to quantum computing development, including taking equity stakes in quantum companies through the CHIPS and Science Act ecosystem, as Heffernan noted in his analysis. For investors, the convergence of AI and quantum creates a new set of investment opportunities that span both sectors, including companies like IBM ($IBM), IonQ ($IONQ), Rigetti Computing ($RGTI), and Quantum Computing Inc. ($QUBT) in the quantum space, alongside the established AI names.

The practical implication for investors is that the AI trade is no longer just about which company has the best model or the fastest chip. It is increasingly about which companies are positioned to benefit from the massive flow of government and private capital being directed at technological supremacy. Companies that straddle both the AI and quantum domains, or that provide essential infrastructure for both, may offer particularly attractive risk-reward profiles. Heffernan's analysis on Live Trading News highlighted several convergence trade names to watch, including $NVDA, $GOOGL, $MSFT, $IBM, $IONQ, and $TSM, and investors would do well to consider the geopolitical dimension when constructing their AI stock portfolios.

Other Notable AI Companies Worth Watching

Advanced Micro Devices ($AMD) - The NVIDIA Challenger

AMD ($AMD) has emerged as the most credible challenger to NVIDIA's dominance in AI accelerators, with its Instinct MI300X and MI325X data center GPUs gaining significant traction among cloud providers and enterprise customers. The company's acquisition of Xilinx also gives it a strong position in FPGA (Field-Programmable Gate Array) technology, which is increasingly used for AI inference workloads that require flexibility and low latency. AMD's ability to offer competitive AI accelerators at price points below NVIDIA's products has made it the preferred alternative for customers seeking to diversify their AI hardware supply chain, and the company's data center revenue has grown substantially as a result.

Intel Corporation ($INTC) - The Turnaround AI Play

Intel ($INTC) is in the midst of a multi-year turnaround effort under CEO Pat Gelsinger that includes a significant push into AI computing. The company's Gaudi series of AI accelerators represents a direct challenge to NVIDIA and AMD in the data center AI training and inference market. While Intel has struggled to gain meaningful market share against its better-capitalized rivals, the company's recent partnerships and pricing strategies have begun to yield results. Intel also benefits from the US government's push for domestic semiconductor manufacturing through the CHIPS Act, which has provided substantial subsidies for the company's factory construction projects in Arizona, Ohio, and Oregon.

Micron Technology ($MU) - The AI Memory Boom

Micron ($MU) has become one of the most important AI infrastructure companies through its leadership in high-bandwidth memory (HBM), the specialized memory chips that sit next to AI accelerators and feed them data fast enough to keep them busy. As Shayne Heffernan highlighted in his June 2026 analysis, Micron posted $41.5 billion in revenue with approximately $100 billion in take-or-pay contracted demand, providing what he described as proof that AI spending is committed and accelerating, not speculative. Micron's HBM4 products, designed for NVIDIA's upcoming Vera Rubin platform, represent the next generation of AI memory technology and are expected to drive significant revenue growth in the coming years.

Qualcomm Incorporated ($QCOM) - Edge AI and On-Device Intelligence

Qualcomm ($QCOM), known primarily for the Snapdragon chips that power most of the world's smartphones, is positioning itself as a leader in edge AI - the deployment of AI capabilities directly on devices rather than in the cloud. The company's latest Snapdragon processors include dedicated neural processing units (NPUs) capable of running AI models locally on smartphones, laptops, and IoT devices. This on-device AI approach offers significant advantages in terms of privacy, latency, and cost (no cloud computing fees), and Qualcomm is working with Google, Microsoft, and other major technology companies to optimize AI models for on-device execution. As AI moves beyond the data center and onto billions of edge devices, Qualcomm is positioned to be a primary beneficiary.

Investment Framework: How to Evaluate AI Stocks

With dozens of publicly traded companies now offering some form of AI exposure, investors need a structured framework for evaluating which AI stocks deserve a position in their portfolios. The following criteria, informed by the analysis from Live Trading News and the KXCO Ontology Engine, provide a starting point for AI stock evaluation. First, consider the company's position in the AI value chain: is it providing essential infrastructure (chips, cloud, memory) where demand is structural and growing, or is it an application-layer company that needs to demonstrate AI-driven revenue growth? Infrastructure companies tend to offer more predictable revenue trajectories during the buildout phase, while application-layer companies offer higher growth potential but greater execution risk.

Second, evaluate the competitive moat. In AI, moats can take several forms: technological (proprietary models or silicon), ecosystem (platform effects and switching costs), data (unique training datasets), distribution (existing customer relationships), or cost (ability to offer AI services at lower prices than competitors). Companies like NVIDIA ($NVDA) have technology and ecosystem moats, Microsoft ($MSFT) has a distribution moat through its enterprise relationships, Amazon ($AMZN) has a cost moat through custom silicon, and Meta ($META) has a data moat through its social media platforms. The strongest AI investments combine multiple moat types.

Third, consider valuation relative to AI growth potential. Many AI stocks trade at premium multiples that reflect the market's expectations for future growth. The key question is whether a company's actual AI revenue trajectory can support its current valuation. Companies like Alibaba ($BABA) and Baidu ($BIDU) offer AI exposure at discounted valuations, while companies like Palantir ($PLTR) and Broadcom ($AVGO) require greater conviction in sustained high growth rates. Finally, be mindful of the geopolitical dimension, particularly for companies with significant China exposure or dependence on cross-strait supply chains. The AI investment landscape is dynamic and evolving rapidly, and investors should approach it with both enthusiasm for the long-term opportunity and discipline in their valuation and risk analysis.

Quick Reference: Major AI Stocks and Cashtags

Company | Cashtag / Ticker | Market Cap (Approx.) | Primary AI Role |

|---|---|---|---|

NVIDIA Corporation | $4.7 Trillion | AI GPU / accelerator design | |

Apple Inc. | $4.3 Trillion | On-device AI (Apple Intelligence) | |

Alphabet Inc. | $4.34 Trillion | AI research, Gemini models, TPUs | |

Microsoft Corporation | $3.2 Trillion | AI cloud platform (Azure + OpenAI) | |

Amazon.com Inc. | $2.3 Trillion | AI cloud (AWS Bedrock), custom silicon | |

Meta Platforms Inc. | $1.6 Trillion | Open-source Llama models, social AI | |

TSMC | $1.1 Trillion | AI chip manufacturing | |

Broadcom Inc. | $950 Billion | Custom ASICs, AI networking | |

Oracle Corporation | $500 Billion | Enterprise AI cloud (OCI) | |

Palantir Technologies | $180 Billion | Enterprise AI platform (AIP) | |

AMD | $230 Billion | AI accelerators (Instinct), FPGAs | |

Intel Corporation | $110 Billion | AI accelerators (Gaudi), foundry | |

Micron Technology | $160 Billion | HBM memory for AI | |

Qualcomm | $190 Billion | Edge AI, on-device AI (Snapdragon) | |

Alibaba Group | $280 Billion | Qwen LLMs, Aliyun AI cloud | |

Tencent Holdings | $430 Billion | Hunyuan LLMs, social / gaming AI | |

Baidu Inc. | $45 Billion | Ernie LLMs, Apollo autonomous driving | |

SenseTime | 002415.HK | $28 Billion | Computer vision, SenseNova models |

Zhipu AI (Z.ai) | Private (IPO expected) | $15B+ (est.) | GLM models, agentic AI |

Table 2: Comprehensive AI Stock Reference Guide — Cashtags, Market Caps, and Roles (Source: Market Data, July 2026)

Looking Ahead: The AI Investment Landscape in Late 2026 and Beyond

As we navigate the second half of 2026, the AI investment landscape is simultaneously broader and more complex than at any point in the technology's brief but spectacular history. The trillion-dollar US AI titans - NVIDIA, Alphabet, Microsoft, Amazon, and Meta - continue to dominate the sector by market capitalization, but the opportunity has expanded far beyond these household names. The AI value chain now encompasses semiconductor manufacturers, memory providers, networking companies, enterprise software platforms, and a growing roster of Chinese companies that are closing the capability gap with stunning speed.

Shayne Heffernan's observation that AI is still early remains the most important insight for investors to internalize. The $100 billion in contracted memory demand, the $300 billion\+ in cumulative hyperscaler infrastructure spending, and the accelerating pace of AI model improvements all point to an industry that is in the early innings of a multi-year expansion. The opportunity is broadening from the center into the periphery, from training accelerators to memory, custom silicon, power, edge inference, and enterprise applications. Companies that were not considered AI stocks two years ago are now being repriced as AI businesses as the technology permeates every sector of the economy.

For investors, the practical implication is clear: the AI trade is not a single stock or a single theme. It is a multi-year, multi-phase investment opportunity that requires a diversified approach. The best AI stock portfolios will combine exposure to the infrastructure leaders (NVIDIA, TSMC, Micron), the cloud platforms (Microsoft, Amazon, Google), the enterprise AI enablers (Palantir, Salesforce, ServiceNow), and selectively, the Chinese AI ecosystem (Alibaba, Tencent, Baidu) for investors comfortable with the additional geopolitical risk. The companies that will generate the highest returns may not be the ones making headlines today - they may be the peripheral companies that are just beginning to be pulled into AI's expanding orbit. As Heffernan wrote, we are early in that repricing, and the investors who recognize the breadth of the opportunity will be the ones who benefit most from the AI revolution that is still unfolding.

References and Sources

Live Trading News - Quantum AI and blockchain market intelligence by Shayne Heffernan. Available at: https://www.livetradingnews.com

KXCO Ontology Engine - AI sector as typed, sourced claims. Available at: https://kxco.ai/ontology-live/

Shayne Heffernan, "AI Is Still Early. Quantum Is Real.", Live Trading News, June 25, 2026.

Shayne Heffernan, "AI \+ Quantum: The US-China Convergence Trade," Live Trading News, July 9, 2026.

CNBC, "China's Zhipu is booming with Anthropic and OpenAI held back," June 26, 2026.

CompaniesMarketCap - Largest AI companies by market capitalization. Available at: companiesmarketcap.com

All market capitalization figures are approximate as of July 2026 and are subject to change. This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with financial advisors before making investment decisions.

AI and Quantum Computing Latest News

AI and quantum computing are converging into a single US-China contest. A fact-checked, investor-focused map of the model gap, the quantum milestones, the security imperative, and the stocks positioned across both — NVDA, GOOGL, MSFT, IBM, IONQ, TSM. By Shayne Heffernan.

Investing: The US-China AI Battle

US China AI battle investing, decoded: Claude Fable 5 & Opus 4.8 vs GLM-5.2 & Kimi K2.7, the NVIDIA-vs-Huawei chip supply chain, target prices for the best AI stocks to buy in 2026, and a full geopolitical risk matrix. By Shayne Heffernan.

Economic Calendar and Trading Strategies for July 7–11, 2026

A trader's guide to the week of July 7–11, 2026: the US and China economic calendar, the Fed-pivot test after a soft jobs report, and how to trade Nvidia, SpaceX, Bitcoin, the dollar, gold, silver, AI and quantum. Track every release on Live Trading News.

Quantum Computing Hits Commercial Reality

Quantum computing hit commercial reality in 2026: $2B in US foundry funding, Quantinuum's $14B IPO, and violent rallies in IonQ, Rigetti and D-Wave. Shayne Heffernan explains the AI–quantum flywheel, tables the stocks in the space (IONQ, RGTI, QBTS, QUBT, QNT, IBM, GOOGL, MSFT, NVDA, GFS, HON), covers China's LineShine supercomputer, and closes on KXCO's post-quantum solutions.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.