Wall Street Outlook: Stocks, AI, Oil and Bitcoin (June 22-26)

AI capex keeps pulling the tape up while a hawkish Warsh Fed and a still-twitchy oil market pull it back. Micron earnings and Thursday's PCE are the week's hinges.

By Shayne Heffernan

Markets walk into the back half of June with a split personality. The headline indices are still parked within shouting distance of record territory — the S&P 500 printed above 7,600 for the first time at the start of the month and the Nasdaq Composite is hovering near 26,500 — yet underneath that calm there is a genuine tug of war going on. Artificial intelligence spending is pulling the tape higher. A hawkish Federal Reserve and a Middle East that refuses to fully settle down are pulling it back.

That is the real Wall Street outlook for the week ahead: not a single story, but a fight between two of them.

The calendar does not give the bulls much cover. It is a light week for data, which means the few releases that do land will carry extra weight, and the earnings that report will be scrutinised line by line. Add a freshly public SpaceX, a quantum-computing trade that has roared back to life, and a Bitcoin that has quietly given back most of its June gains, and you have plenty to chew on. Let me walk through what actually matters.

What is driving the market

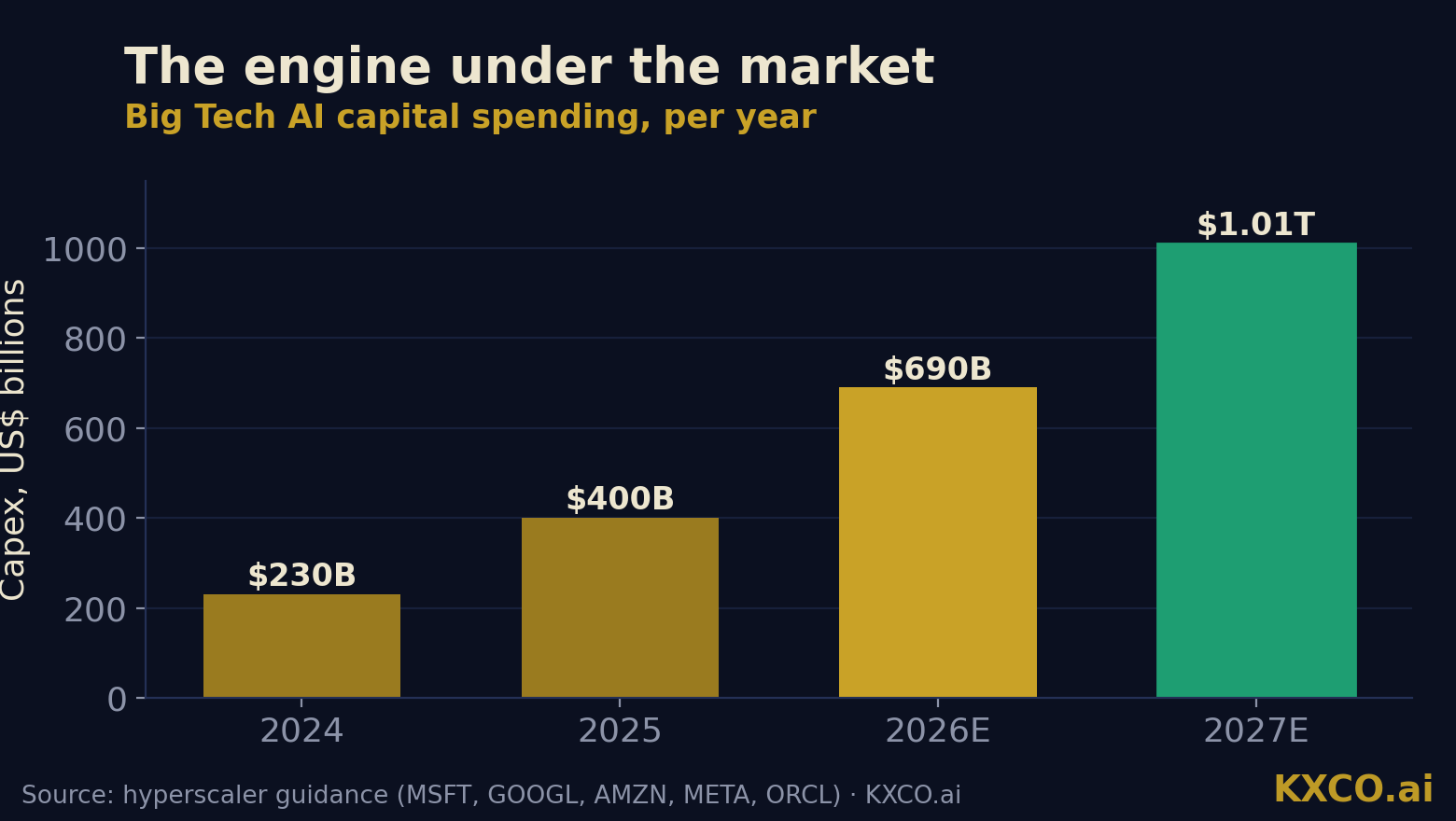

Strip everything else away and one number explains most of this rally: capital expenditure on AI.

The five largest cloud and AI builders — Microsoft, Alphabet, Amazon, Meta and Oracle — have collectively committed to somewhere between $660 billion and $690 billion of capex this year, close to double what they spent in 2025. Street estimates now have total compute spending topping $1 trillion in 2027. To put that in plain terms, 2026 is on course to be the first trillion-dollar year of compute spending in human history. Microsoft has even said it is sitting on an $80 billion backlog of Azure orders it cannot fill, not because demand isn't there but because it cannot get power to the data centres fast enough.

That is the bull case in one paragraph. As long as the cheques keep clearing, the companies selling the picks and shovels — chips, networking, power, cooling — keep beating. The bear case is just as simple: spending on this scale eventually has to earn a return, and the day the market decides it won't, the unwind will be ugly. We are nowhere near that day yet. But it is worth keeping the receipt.

Against that backdrop sits a Fed that has stopped playing along. Kevin Warsh chaired his FOMC and the committee left rates unchanged, but the message was hawkish: with energy costs feeding back into prices, higher rates later this year are now openly on the table. Headline CPI is running near 3.8%. Rate cuts, which the market spent the spring pricing in, have quietly been priced back out. That single shift is why long-duration assets — speculative tech, crypto — have wobbled even as the megacaps held firm.

The week ahead: a thin calendar with two real catalysts

Here is what is on the docket for June 22–26.

Monday 22 — A quiet open. No tier-one data; the market trades off the weekend's Middle East headlines and positioning into the heavyweight reports later in the week.

Tuesday 23 — Earnings from Carnival ($CCL) and FedEx ($FDX). FedEx is the one to watch; it is as good a read on global goods demand as we get, and management's tone on volumes tells you more about the real economy than most government data.

Wednesday 24 — May new home sales, the Fed's annual bank stress-test results, and the week's marquee report: Micron ($MU) after the close, alongside Paychex ($PAYX) and Jefferies ($JEF).

Thursday 25 — The big one. May PCE — the Fed's preferred inflation gauge — plus the final read on Q1 GDP and May durable goods orders. Darden ($DRI) reports.

Friday 26 — Tidy-up day into the weekend, with sentiment data and the market digesting whatever PCE delivered.

Thursday's PCE is the hinge the whole week turns on. Forecasts have core PCE up around 0.3% on the month and roughly 3.4% year over year, with the headline rate pushed up toward 4.1% by energy. A hot print hardens Warsh's higher-for-longer message and puts pressure on exactly the assets that have run hardest. A soft one revives the rate-cut trade and lets the bulls breathe. Position accordingly.

The big stocks: Nvidia, Micron and a brand-new giant

Nvidia ($NVDA) remains the gravitational centre of this market, and the numbers are still absurd in the best way. Fiscal-2026 revenue came in at $215.94 billion, up more than 65%. The most recent quarter did $81.62 billion, an 85% jump, with guidance of $91 billion ahead — both above consensus. The company still owns an estimated 85% to 92% of the AI accelerator market. "Blackwell sales are off the charts, and cloud GPUs are sold out," is how Jensen Huang put it, and the order book backs him up. Analysts are overwhelmingly at Strong Buy with an average target near $299. The one cloud on the horizon is custom silicon — Google's, Amazon's and others' in-house chips — which is creeping up to nearly 28% of the AI-chip market and is the long-term threat to that fat margin. Nvidia is also out raising around $20 billion in debt, which tells you how aggressively it intends to keep feeding the buildout.

The chip story you should actually circle this week, though, is Micron. Memory is where the AI cycle gets violent on the upside, and Micron's fiscal-Q3 numbers land Wednesday. The Street is looking for earnings near $20 a share on revenue around $35 billion — a roughly 276% year-on-year surge — and several shops have hiked price targets into a frankly eye-watering $1,200 to $1,500 range. The single line that matters is high-bandwidth memory. Management has signalled its entire HBM capacity is sold out under binding contracts through the rest of 2026 and into 2027. If they confirm that and nudge pricing higher, it validates the whole AI-hardware trade. If they hedge, the read-through hits everyone.

Then there is the new kid, and it is not a small one.

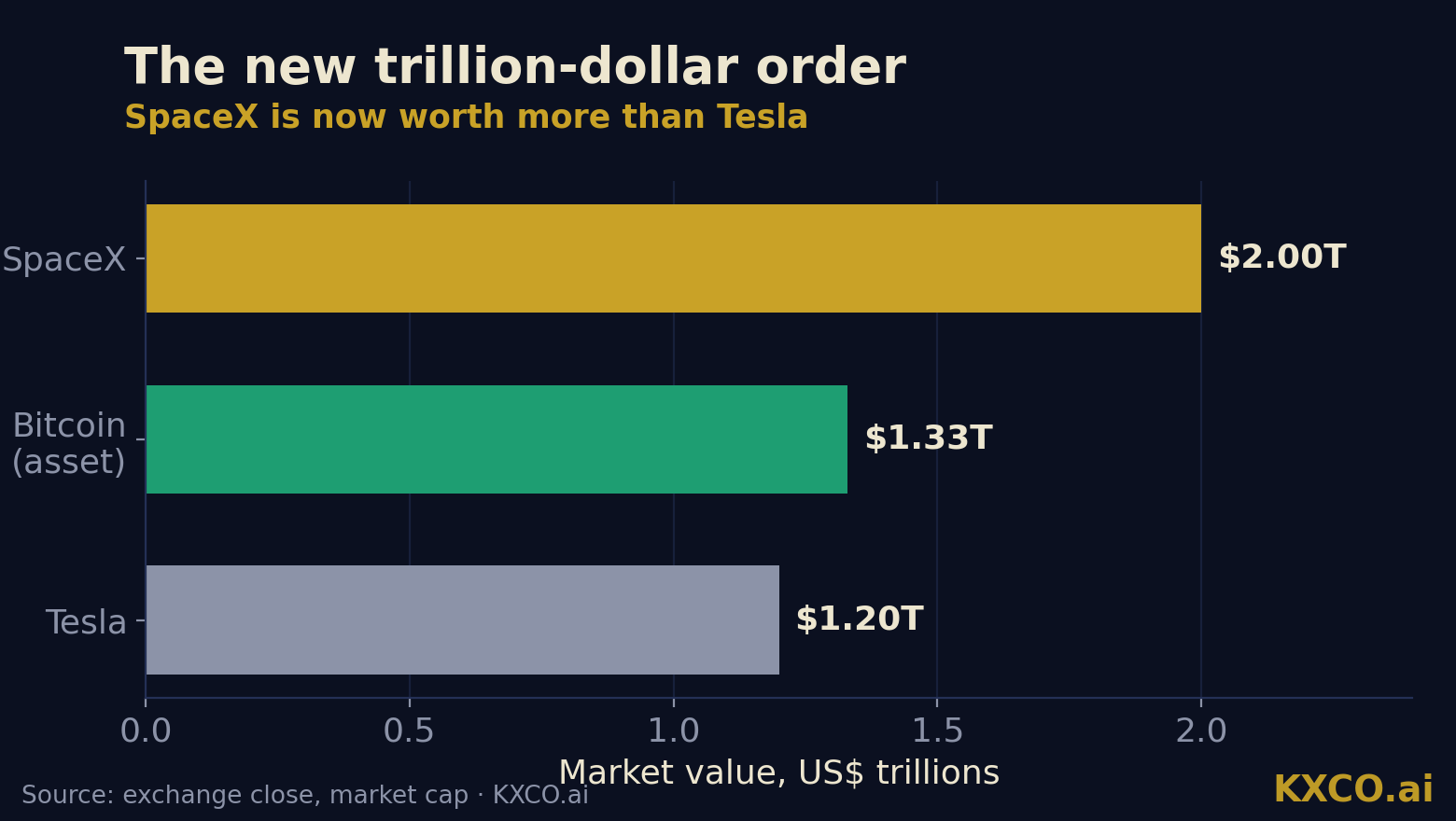

SpaceX ($SPCX) went public on June 12 in the largest IPO in US history. It priced at $135, opened to a frenzy, touched $176.52 intraday and closed its first session at $161.11 — up 19% on day one. The valuation target was $1.75 trillion, and with the stock where it is, Elon Musk's space and satellite company is now worth north of $2 trillion — more than Tesla ($TSLA), which sits around $1.2 trillion. Read that again: the rocket company is now bigger than the car company. The engine is Starlink, which has grown to more than 9,800 operational satellites and over 10 million subscribers across 100 countries, and is the only consistently profitable piece of the business. For a market obsessed with AI, SPCX is a reminder that the other frontier — space and connectivity — just minted a giant overnight. Expect it to stay volatile while the float settles and the lock-ups loom.

AI and quantum: the second leg gets funded

If AI is leg one of the tech trade, quantum computing has become leg two — and this is where it gets interesting for anyone watching the post-quantum security theme, which is squarely in KXCO's wheelhouse.

The catalyst was policy. In late May the US Commerce Department put more than $2 billion of CHIPS and Science Act money into nine quantum companies in exchange for equity stakes, with IBM as the $1 billion anchor. That is the government effectively underwriting the sector. The pure-plays have responded in kind. IonQ ($IONQ) is up more than 60% year to date, guiding 2026 revenue to $225–245 million after a 77% jump in the first quarter, and has rolled out its Clavis XG Multiplex to push further into quantum security. Rigetti ($RGTI) is up better than 44% in a month and picked up $100 million in the Commerce deal for hardware scaling.

A word of caution, because someone has to say it: these are still tiny-revenue, no-profit companies trading at valuations that assume the future arrives on schedule. The move is real, the funding is real, and the long-term thesis is sound. But position sizing matters. The flip side of quantum progress is that the cryptography securing today's financial system has a shelf life — which is exactly why the migration to post-quantum standards is no longer a research footnote but a board-level conversation. The companies building the threat and the companies building the defence are, increasingly, the same trade.

Iran, oil and the round trip nobody expected

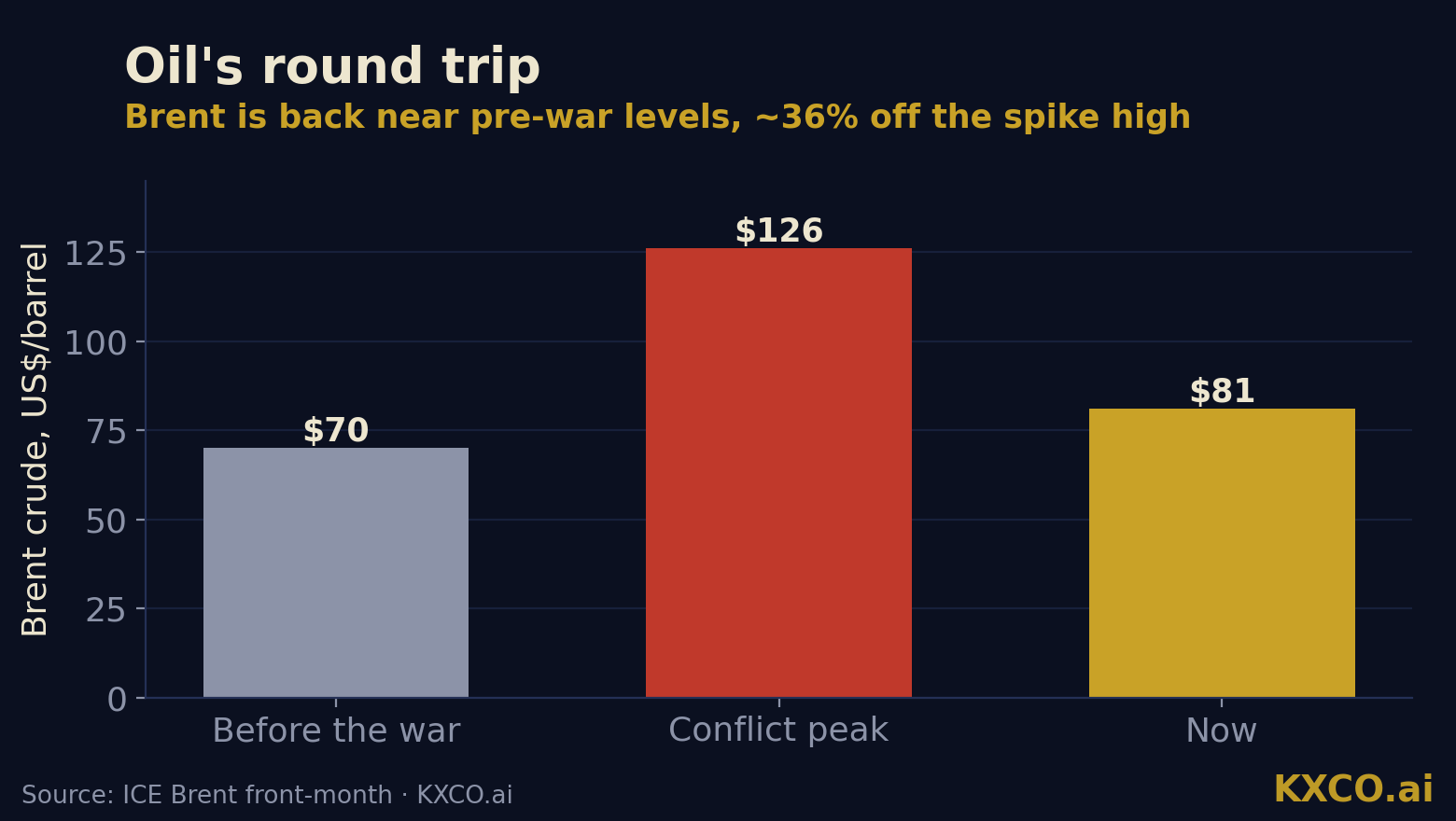

The geopolitical story that dominated the spring has, mercifully, started to de-escalate — and the oil chart tells the tale better than any headline.

At its worst, the 2026 Iran war shut the Strait of Hormuz — the chokepoint roughly a fifth of the world's seaborne oil passes through — and sent Brent spiking toward the mid-$120s. US gasoline, which started the conflict just under $3 a gallon, ran as high as $4.56. The progress since has been substantial: a Pakistan-mediated memorandum points to Iran reopening Hormuz and the US lifting its blockade of Iranian ports. Brent has fallen all the way back to around $81 — roughly 36% off the spike high — with West Texas Intermediate near $77.

But this is not over, and the tape knows it. When US–Iran talks in Switzerland were abruptly postponed on Friday, crude ticked straight back up. The near-term range looks like $75 to $82, and the swing factor is binary: every Hormuz headline moves the barrel. For equities, lower oil is a quiet tailwind into the back half of the year — it takes pressure off the inflation data and the consumer. For the energy complex, the easy money on the long side has already been made.

FX: a firm dollar and a yen on a knife's edge

Currencies are where the Fed's new hawkishness shows up most cleanly. The US Dollar Index is sitting near 99 and is expected to grind out the month roughly flat — firm, but rangebound. Sticky inflation and a Fed with cuts off the table support the buck; slower growth and the prospect of Middle East de-escalation cap it. EUR/USD is holding in a 1.15–1.22 band, trading around 1.17.

The wildcard is the yen. The market is pricing something like an 80% chance the Bank of Japan finally hikes, with USD/JPY up near 158–159. If the BoJ moves and the Fed stays hawkish, you get two central banks pulling in the same direction and a lot of carry-trade unwinding to watch. This is the corner of the macro map I'd keep one eye on all week; yen volatility has a way of spilling into everything else.

Bitcoin: the June pop, given back

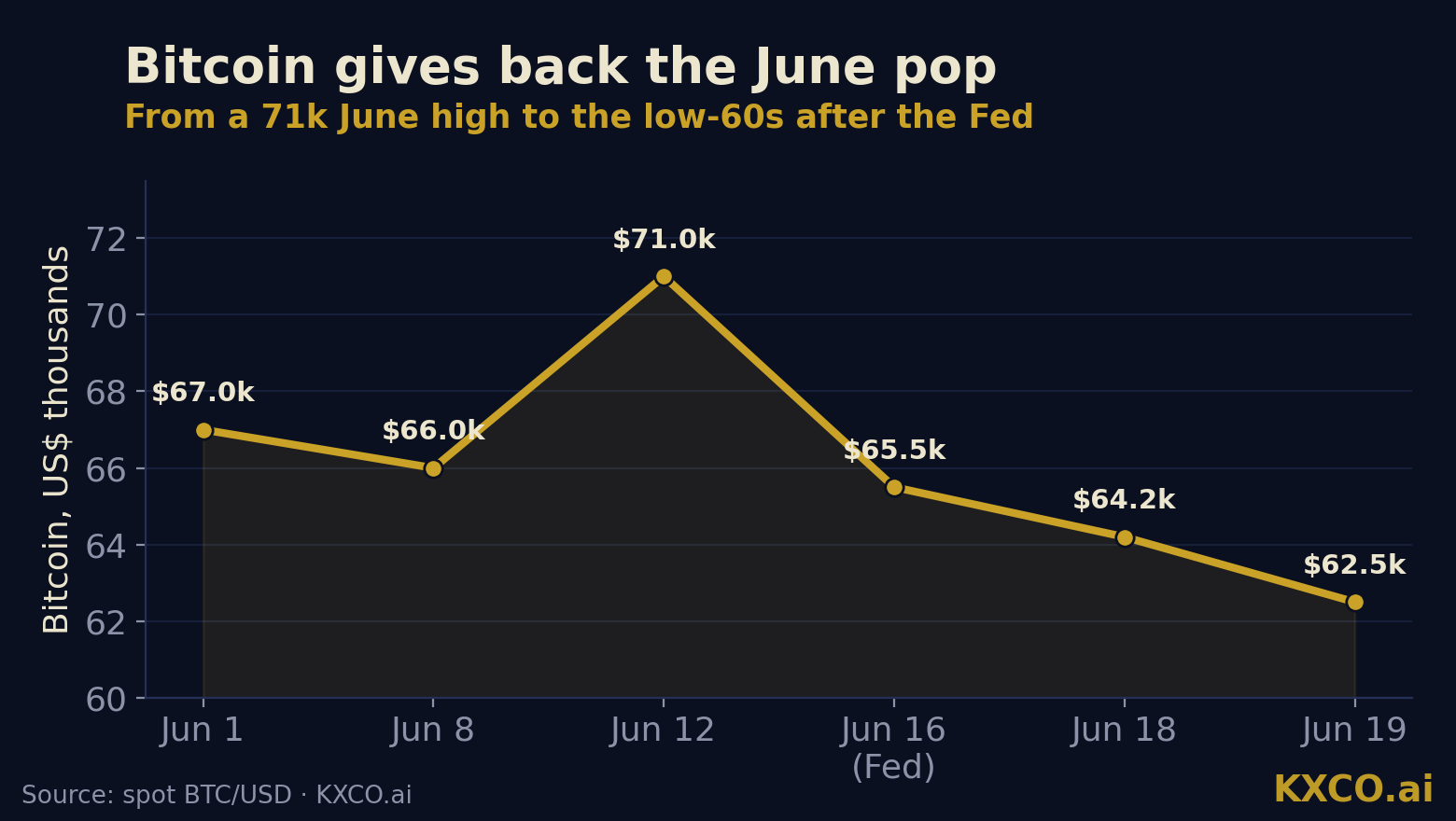

Crypto had a great first week of June and has spent the rest of the month handing it back.

Bitcoin pushed above $71,000 early in the month on ETF inflows and the usual adoption headlines, then rolled over. It has been sliding since the Fed meeting, broke below $64,000 — a move that triggered more than $1.1 billion in liquidations in a single day — and was trading in the low-$60,000s by Friday. The institutional money cooled hard: spot Bitcoin ETFs saw $2.3 billion of net outflows in May, the steepest monthly exodus of the year. Bitcoin's market value is still around $1.33 trillion, comfortably ahead of Ethereum's $233 billion.

The story here is rates, plain and simple. When the Fed signals higher-for-longer, the most rate-sensitive, highest-beta asset on the board gets sold first, and that is crypto. Until the rate narrative softens — and Thursday's PCE is the next chance for that — Bitcoin is likely to stay heavy. This is a macro tape, not a crypto-specific one; Bitcoin is trading like the risk asset it is.

The bottom line

Put it all together and the week ahead is a referendum on one question: can the AI capex engine keep outrunning a hawkish Fed and a still-twitchy oil market? My read is that it can, for now — the spending is too large and too committed to stall in a single quarter, and Micron is likely to pour fuel on the AI-hardware fire on Wednesday. But the margin of safety is thinner than the index levels suggest.

Watch Thursday's PCE above everything. A cool number and this market grinds higher into quarter-end. A hot one and the same hawkish Fed that has been an inconvenience becomes a problem. Keep some powder dry, respect the levels, and don't confuse a record-high index with a low-risk market. They are not the same thing.

Analysis by Shayne Heffernan. This article is for information only and is not investment advice. Charts and data graphics by KXCO.ai. Every new Live Trading News story is cryptographically signed.

SpaceX and the Space Economy

Space is no longer the domain of governments alone. Led by SpaceX and a growing ecosystem of launch providers, satellite operators, and lunar infrastructure companies, the space economy is rapidly becoming one of the world's most important growth industries and could represent the next great gold rush for investors.

USA vs China: The Quantum Computing Race

The U.S. still leads quantum computing, but China has closed the gap fast — on hardware scale, supply-chain self-reliance and quantum networking. A category-by-category scorecard as of June 2026.

5 Stocks to Buy as Rate Fears Return

SpaceX just completed the largest IPO ever, Intel is up 250% in 2026, and the rate-hike bears are circling. Shayne Heffernan makes the bullish case for five most-active names — NVIDIA, Intel, Nokia, Snap and SpaceX — and explains why higher rates are a buying opportunity, not a reason to sell.

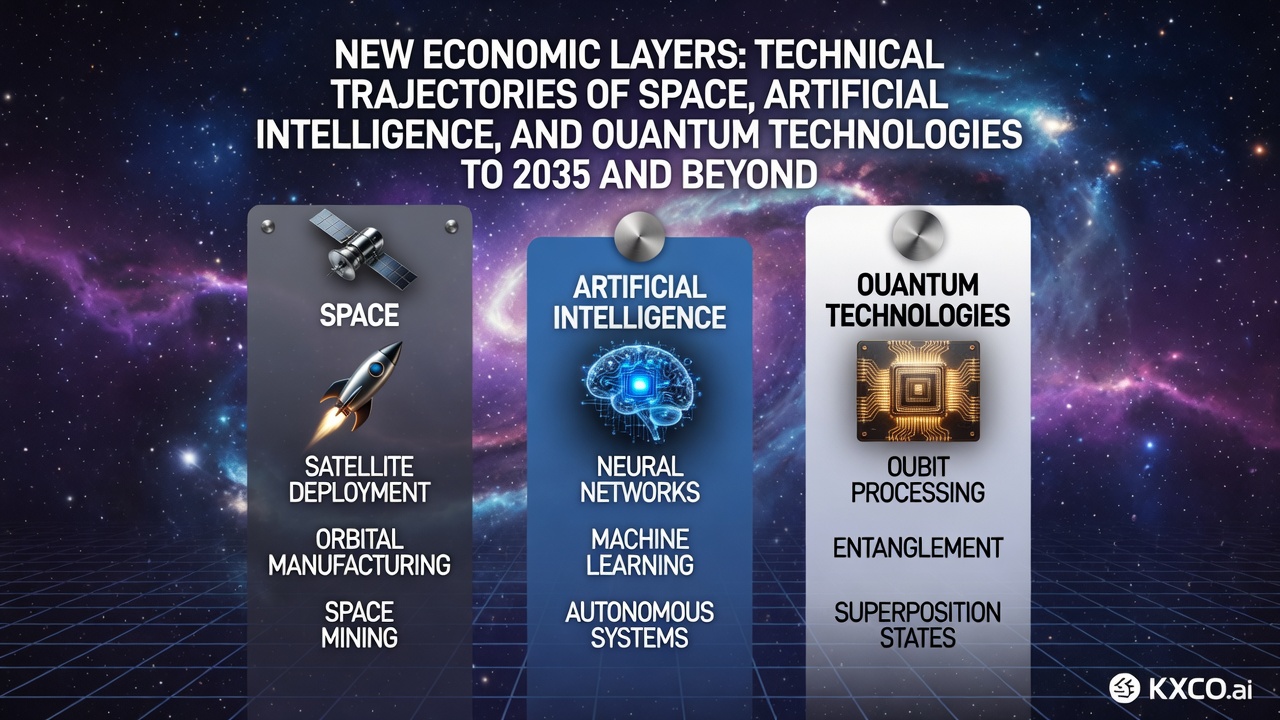

The New Economies: Space, AI, and Quantum

Three new economic layers are taking shape: space is becoming an industrial domain, artificial intelligence is evolving into continuous infrastructure, and quantum technologies are moving into operational use in simulation and sensing. While technical and energy constraints remain significant, the period through 2035 is likely to see these layers expand in parallel, creating new requirements for verifiable trust and post-quantum security. KXCO is positioning its infrastructure as the transaction

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.