5 Stocks to Buy as Rate Fears Return

Why $NVDA, $INTC, $NOK, $SNAP and $SPCX still look like buys even if the Fed turns hawkish again.

Markets love a wall of worry, and right now the tape is climbing one. Take a glance at the most-active board and you see a market that cannot make up its mind: $SPCX off more than 4%, $SNAP down a brutal 8%, $NOK drifting lower, while $INTC rips nearly 4% higher and $NVDA holds the line just above $207. Five names, five different stories, one shared backdrop — a market suddenly nervous that the era of rate cuts is over and that the next move from central banks could be a hike rather than a cut.

Here is my take after thirty years of doing this: that fear is exactly the kind of thing that hands patient investors their best entry points. When everyone is bracing for higher rates, the good businesses get sold alongside the bad ones, and the baby goes out with the bathwater. I am bullish on all five of these stocks, and I am bullish because of the rate-hike chatter, not in spite of it. Let me walk you through why.

And what a week it has been for headlines under these tickers. SpaceX just completed the largest initial public offering in history — pricing on June 11 and debuting on the Nasdaq on June 12, raising roughly $75 billion — so $SPCX is now a live, listed stock rather than a private dream. Intel has ripped some 250% higher in 2026 after Google placed an order to build more than three million of its custom AI chips at Intel Foundry. Snap just launched its $2,195 "SPECS" augmented-reality glasses and won a credit-rating upgrade. Nokia opened a new AI networking lab in Silicon Valley. And NVIDIA quietly carries a market value north of $5 trillion with a Strong Buy consensus behind it. This is not a sleepy corner of the market — it is where the action is. So let me update the thesis with what is actually happening right now.

Why the rate-hike fear is a gift, not a threat

First, the macro. The bond market has spent the last few weeks repricing the odds of another round of tightening. Sticky services inflation, resilient labour data, and a few too-hot prints have the hawks circling again. Every time a Fed governor clears their throat, growth stocks wobble and the most-active list lights up red. That is the tape you are looking at above.

But step back. Rate hikes are a blunt instrument aimed at cooling demand. They hurt indebted, cash-burning, no-moat companies the most — the ones that need cheap money to survive. They barely scratch businesses that throw off cash, own irreplaceable infrastructure, or sell something the world cannot stop buying. The art of investing into a hawkish scare is to separate the two.

Of the five names on this board, four are cash machines or strategic monopolies in the making, and the fifth is a turnaround so cheap that the rate question barely moves the needle. That is why I want to own this basket into the fear, not run from it. Higher rates compress the multiple you are willing to pay — they do not repeal the demand for AI compute, 5G networks, satellite internet, or digital advertising. The demand curve does not care what the Fed funds rate is.

There is a second, less obvious point. A central bank only hikes when the economy is running hot. A hot economy means corporate earnings are growing, ad budgets are expanding, capital spending on technology is accelerating, and consumers are still swiping their cards. The very condition that produces a rate hike is the condition that drives revenue for the companies below. Bears treat "higher rates" as a synonym for "recession." It is not. Higher rates into a strong economy is a bullish setup for operating businesses, even if it is a headwind for the multiple. I will take growing earnings and a lower multiple any day — that is how you compound.

Now to the names.

$NVDA

Let us start with the one everybody owns and everybody second-guesses. $NVDA is sitting at $207.57, dead flat on the session, and that flatness is itself the story. On a day when the speculative end of the market is getting hit, the most important stock in the world barely moves. That is what leadership looks like. Money is not fleeing NVIDIA; it is parking in it.

The latest headlines only reinforce the point. NVIDIA now carries a market capitalisation above $5 trillion, and the analyst community is not blinking: the consensus sits at Strong Buy across the better part of forty covering analysts, with an average target up near $299 — a meaningful step above today's price. The order flow keeps confirming the story, too. Just this week, HPE revealed that cloud provider Vultr has selected HPE and NVIDIA for large-scale AI data-centre deployments to meet booming enterprise demand. That is the pattern: another quarter, another marquee customer committing to NVIDIA silicon. The next earnings report lands in late August, and the bar, as always, is high — but the demand signals heading into it are anything but soft.

The bull case here has not changed, and the rate scare does not dent it. NVIDIA sells the picks and shovels of the single largest capital-spending cycle in the history of technology. Every hyperscaler — every cloud provider, every sovereign AI project, every enterprise trying not to be left behind — is competing to buy as many of NVIDIA's accelerators as the company can ship. Demand still outstrips supply. When you have pricing power like that, you can pass through cost pressure, you can fund your own growth out of cash flow, and you do not need to tap expensive debt markets to keep the lights on. A higher discount rate trims the present value of NVIDIA's future profits on a spreadsheet, but it does nothing to slow the orders.

There is also a moat the bears consistently underweight: software. NVIDIA is not just a chip company; it is a platform company. The developer ecosystem built on top of its hardware is a switching cost that compounds every year. A rival can, in theory, build a competitive accelerator. What it cannot easily replicate is the decade of tooling, libraries, and developer mindshare that makes NVIDIA's silicon the default choice. And the demand base is broadening, not narrowing — sovereign AI projects, where entire nations are standing up their own compute capacity rather than renting it from foreign clouds, are an enormous and durable new source of orders that barely existed a few years ago.

What I watch with $NVDA is not the daily candle but the data-center build-out. As long as the largest technology companies on earth are guiding capital expenditure up — and they are — NVIDIA is the toll booth they all have to pass through. The next product cycle extends that lead rather than closing it. The flat tape today, while everything around it sells off, is a tell. In a genuine risk-off panic driven by rate fear, you find out very quickly which stocks investors refuse to sell. NVIDIA is at the top of that list. I remain a buyer, and I would use any rate-driven pullback to add.

$INTC

Now the comeback kid. $INTC is the green print on an otherwise jittery board, up 3.76% to $121.46, and I think this is one of the most interesting setups in large-cap technology. For years, Intel was the value trap that everyone loved to short — losing process leadership, losing share, losing credibility. The narrative was that the company would slowly fade. That narrative is now being challenged, and the stock is responding.

And the comeback is no longer theoretical — it is showing up in the tape and the order book. Intel began 2026 below $40 and has rallied something like 250% on the year, one of the great large-cap turnarounds of the decade. The catalyst that lit the fuse: Google placed an order to manufacture more than three million of its custom Tensor Processing Units at Intel Foundry for 2028, the kind of anchor customer that validates the entire foundry thesis in a single stroke. Computex this year turned Intel into a full-stack AI story — from Xeon data-centre chips to 18A-based PC and edge platforms — and the big banks responded by lifting price targets across the board. The stock has wobbled on news that NVIDIA is pushing into Windows laptop processors, a traditional Intel stronghold, and that competitive threat is real and worth watching. But a name up 250% is allowed to catch its breath. The trend is the friend here.

Here is why I am bullish. The market is starting to price Intel not as a declining chip vendor but as a strategic national asset. The entire developed world has woken up to the fact that leading-edge semiconductor manufacturing cannot all sit in one geography. Intel is the only American company with both the design heritage and the ambition to build advanced logic at scale on home soil. That gives it something no spreadsheet captures: political tailwind. Governments want this company to succeed, and they are willing to back that wish with incentives. When the state has a vested interest in your survival, your tail risk shrinks dramatically.

Layer on the operational story. Intel's roadmap to regain process leadership is the most credible it has been in a decade, and the foundry ambition — building chips for other companies, not just itself — opens a total addressable market many times larger than its traditional business. If even a fraction of that foundry vision lands, today's price will look cheap. The foundry economics are worth dwelling on: leading-edge fabrication is one of the most capital-intensive, highest-barrier businesses that exists. There are only a tiny number of companies on earth that can do it at all, and the demand for advanced chips — driven by the very AI wave that powers $NVDA — is structural, not cyclical. A credible third major foundry player would be welcomed by every chip designer that worries about concentration risk in its supply chain. Intel does not need to win the whole market; it needs to win a slice of a market that is exploding in size.

Yes, it is a turnaround, and turnarounds are bumpy. But a 3.76% rally on a red day tells you the smart money is starting to believe. On the rate question, Intel is a manufacturer with real assets and government support — exactly the kind of hard-asset, strategically-protected business that holds up when money gets more expensive. Factories, equipment, and intellectual property are real things with real value, and unlike a speculative growth story, the downside is anchored by tangible assets. I am bullish.

$NOK

$NOK at $13.83, down a modest 1.07%, is the quiet compounder nobody talks about at dinner parties — and that is precisely why I like it. Nokia is one of only a handful of companies on the planet that can build and maintain the core networks that carry the world's data. That is a duopoly-bordering business with enormous barriers to entry, and it sits right in the path of two unstoppable trends: the global 5G build-out and the explosion of AI-driven data-centre networking.

Think about what AI actually requires beyond the chips. It requires moving staggering volumes of data between machines, between data centres, and out to the edge. Someone has to build that plumbing. Nokia's networking and optical infrastructure businesses are levered directly to that spend, and the company has been winning the kind of large data-centre and fixed-network contracts that signal it is being taken seriously as an AI-infrastructure play, not just a legacy telecom name.

The market has noticed. Nokia is up roughly 127% in 2026, and the recent news flow tells you why: the company opened a new AI Networking Innovation Lab in Sunnyvale, California, built to tune networks alongside cloud and AI partners for the heaviest data-centre workloads, and it rolled out agentic-AI capabilities across its broadband products to automate diagnostics and cut operators' costs. The sell-side has been chasing the story higher — Morgan Stanley moved to Overweight with a raised target, with further upgrades from Deutsche Bank and SEB. Yes, there have been down days on worries about softer 5G equipment demand, and that is a fair thing to monitor. But a stock that has more than doubled while throwing off royalty income and a dividend is doing exactly what a quiet compounder is supposed to do.

Then there is the part of Nokia that the market chronically underrates: its patent portfolio. Nokia owns a deep library of essential telecommunications patents, and licensing that intellectual property is a high-margin, recurring, almost annuity-like stream of cash. That income does not evaporate when rates rise — if anything, a steady, contracted royalty stream becomes more attractive to investors when they are nervous about growth. Add a real dividend, a cleaned-up balance sheet, and a valuation that asks very little of you, and $NOK becomes a defensive way to own the AI and 5G theme. The 1% dip on this board is noise. I am a buyer of the boring compounder.

$SNAP

Now for the controversial one. $SNAP is the worst performer on the board today, down 8.14% to $4.74, and I can already hear the bears cackling. Let me make the bullish case anyway, because this is exactly the kind of washed-out, hated name that makes patient investors a great deal of money.

Start with the price. At $4.74, Snap is trading like a company the market has all but given up on. That is the point. When a stock with hundreds of millions of daily users and billions in revenue is priced for irrelevance, you are not paying for growth — you are getting it for free if it ever shows up. The downside has already been front-run by years of disappointment. The risk-reward at this level is asymmetric: limited room to fall, enormous room to recover if the company simply stops bleeding.

The recent news cuts both ways, and that is exactly what you want at a bottom — a tug of war, not unanimous despair. On the bullish side, S&P Global lifted Snap's credit rating to BB- with a positive outlook, citing double-digit first-quarter revenue growth, stronger free cash flow, and more than half a billion dollars of annualised cost cuts — Snap generated roughly $286 million of free cash flow on $1.53 billion of revenue last quarter, which is not the profile of a dying company. Snap also bought spatial-AR firm Illumix to deepen its glasses roadmap. On the bearish side, the market sold the launch of its $2,195 "SPECS" augmented-reality glasses, nervous about the spending, and the UK is threatening tighter youth social-media rules. Founder Evan Spiegel is publicly defending the heavy AR investment against activist pressure — and I am with him. The hardware looks expensive today; so did every category-defining device at launch. You are paying nothing for that optionality at this price.

What could drive that recovery? An advertising market that heals as the economy stays strong — remember, the same hot economy that makes the Fed nervous is the economy in which brands open their ad wallets. Snap's audience is young, engaged, and exactly the demographic advertisers pay a premium to reach. The company has been rebuilding its ad platform and leaning into augmented reality, where it owns genuine technological leadership that the market currently values at roughly zero. And at a sub-$5 share price and a modest market capitalisation relative to its reach, Snap is the kind of strategic asset that draws acquisition interest. A larger platform could buy this audience and AR capability for what, in big-tech terms, is pocket change.

On the rate question, I will be honest: an unprofitable-leaning growth name is the most rate-sensitive stock in this group, which is exactly why it is down the most today. But that sensitivity cuts both ways. The selling has already happened. You are buying after the pain, not before it. When sentiment is this bad and the price is this low, you do not need much to go right. I would treat $SNAP as a small, high-conviction speculative position — and today's 8% flush is the kind of capitulation that often marks a bottom, not a beginning.

$SPCX

And finally, the rocket — and the freshest story on the board. $SPCX is SpaceX, and as of last week it is no longer locked away as a private holding for venture funds and insiders. Space Exploration Technologies priced its IPO on June 11 at $135 a share, sold roughly 555 million shares to raise about $75 billion, and began trading on the Nasdaq on June 12 in the largest initial public offering in history. It opened at $150, jumped nearly 20% on its first day, and ran all the way to an all-time high of $225.64 by June 16 before cooling off. It now changes hands around $175 — well off that high and only modestly above where it priced. That, to me, is the opportunity.

When the most-hyped IPO ever gives back a chunk of its first-week pop, the crowd calls it a broken trade. I call it the first real entry point for investors who were shut out of the offering. The lock-up euphoria is bleeding off, the fast money is taking profits, and the rate scare is giving everyone an excuse to sell — none of which has anything to do with the business underneath.

And what a business it is. SpaceX is building two of the most valuable franchises in the world at once. The first is launch: it has turned getting to orbit into a routine, reusable, dramatically cheaper service, and it dominates global commercial launch by a margin that is almost embarrassing for its competitors. The second is Starlink — a satellite internet constellation that is putting broadband over every corner of the planet, including the vast areas terrestrial networks will never economically reach. Starlink is the part that turns SpaceX from a heroic engineering project into a cash-generating machine, with a subscription revenue base that scales as the constellation grows. That mix of an unassailable launch monopoly and a fast-scaling consumer-and-enterprise connectivity business is precisely why public investors have been clamouring to own it.

The analyst community, freshly able to cover the name, lands at an overall Buy, with an average twelve-month target around $188 and a high estimate of $310. The range is wide — this is a newly public, richly valued stock and it will be volatile — but the direction of travel is up. Launch cadence keeps climbing. Starlink subscribers keep growing. The next-generation vehicle promises to lower the cost of access to space by another order of magnitude, which opens markets we cannot yet fully imagine. This is a business whose value is measured in decades, and decade-long compounding stories should be bought when the first-week froth comes off the price.

On rates: yes, a long-duration growth asset like a freshly listed space franchise feels the squeeze of a higher discount rate more than a dividend-payer does, and a hot IPO is exactly the kind of name that gets sold first in a rate scare. But SpaceX's moat is physical, not financial. No rate hike builds a competitor a reusable rocket fleet or launches tens of thousands of satellites. The competitive position is untouchable, and untouchable positions are worth owning through any rate cycle. I view the post-IPO pullback in $SPCX as the market handing long-term investors a far better price than the people chasing it at $225 ever got.

Putting it together: a barbell for a hawkish world

Look at how this basket is constructed and you will see it is deliberately balanced for exactly the environment the bears are afraid of.

On one end of the barbell you have the cash-rich, moat-protected, hard-asset businesses that shrug off higher rates: $NVDA with its toll on the entire AI economy, $INTC with its hard manufacturing assets and government backing, and $NOK with its essential networks, patent royalties, and dividend. These are the anchors. If rates grind higher, they keep generating cash, keep paying or buying back, and keep their strategic positions. Their multiples might compress, but their businesses do not.

On the other end you have the higher-octane, more rate-sensitive names — $SNAP and $SPCX — that have already taken their punishment on the day and offer asymmetric upside if the rate scare fades or even if it simply stops getting worse. These are smaller positions, sized for their volatility, but they are where the explosive returns hide.

That barbell — defensive cash flow on one side, asymmetric growth on the other — is how I want to be positioned when the consensus is leaning one way. The crowd is leaning toward "rates up, sell everything." History says the crowd is usually most wrong at the extremes.

How I would size and time it

A view is only as good as the way you express it. With a basket like this, I am not trying to call the exact day the rate fear peaks — nobody can, and pretending otherwise is how investors blow up. I would build positions in tranches rather than in one lump, using the volatility the rate scare is creating to my advantage. Buy a piece of the quality anchors — $NVDA, $INTC, $NOK — now, and keep dry powder to add on the down days that hawkish headlines are sure to deliver. Treat the higher-octane names, $SNAP and $SPCX, as smaller satellite positions: size them so that if the rate fear deepens and they fall another leg, you are comfortable adding rather than forced to sell.

The discipline matters more than the entry. Rate-driven sell-offs are noisy and emotional, and the investors who do well in them are the ones with a plan written down before the volatility hits. Decide your position sizes in advance, decide where you would add, and then let the market's anxiety come to you. The goal is not to be a hero on any single day — it is to own great businesses at better prices than the calm crowd was willing to pay a month ago.

The thing the bears keep getting wrong

Let me close on the rate-hike point directly, because it is the question hanging over every red number on this board.

Rate hikes do not kill bull markets. Recessions kill bull markets, and valuation bubbles kill bull markets. A central bank raising rates into a growing economy with strong employment is, historically, something equities have lived with perfectly well — often while making new highs. The 1990s, the mid-2000s, and several stretches since have all featured rising rates alongside rising stock prices, because earnings were growing faster than the discount rate was rising. The mistake the bears make, over and over, is to treat the direction of rates as the only thing that matters and ignore the reason rates are moving.

Right now, rates are firm because the economy refuses to roll over. That is a feature, not a bug. It means the ad market that lifts $SNAP stays open. It means the enterprise capital spending that fuels $NVDA and $NOK keeps flowing. It means the consumer who subscribes to Starlink and the government that backs $INTC are both in a position of strength. The same heat that has the Fed reaching for the brakes is the heat warming the earnings of the companies I want to own.

So when the most-active board lights up red on rate fear, I do not see a warning. I see a sale. I am bullish on $NVDA, bullish on $INTC, bullish on $NOK, bullish on $SNAP, and bullish on $SPCX. I would use the fear to build positions in the quality names and to nibble at the beaten-down ones, and I would let the crowd's anxiety pay for my entry.

The market climbs a wall of worry. This wall is made of interest rates. I plan to climb it.

Shayne Heffernan is the founder of Knightsbridge and a thirty-year veteran of global markets. This article is general market commentary and the personal opinion of the author. It is not investment advice, a recommendation, or an offer to buy or sell any security. Markets carry risk, including the loss of capital. Prices, percentage moves and news referenced are as of mid-June 2026 and will change. Newly listed shares such as $SPCX can be especially volatile in the weeks after an IPO. Always do your own research and consult a licensed financial adviser before making any investment decision.

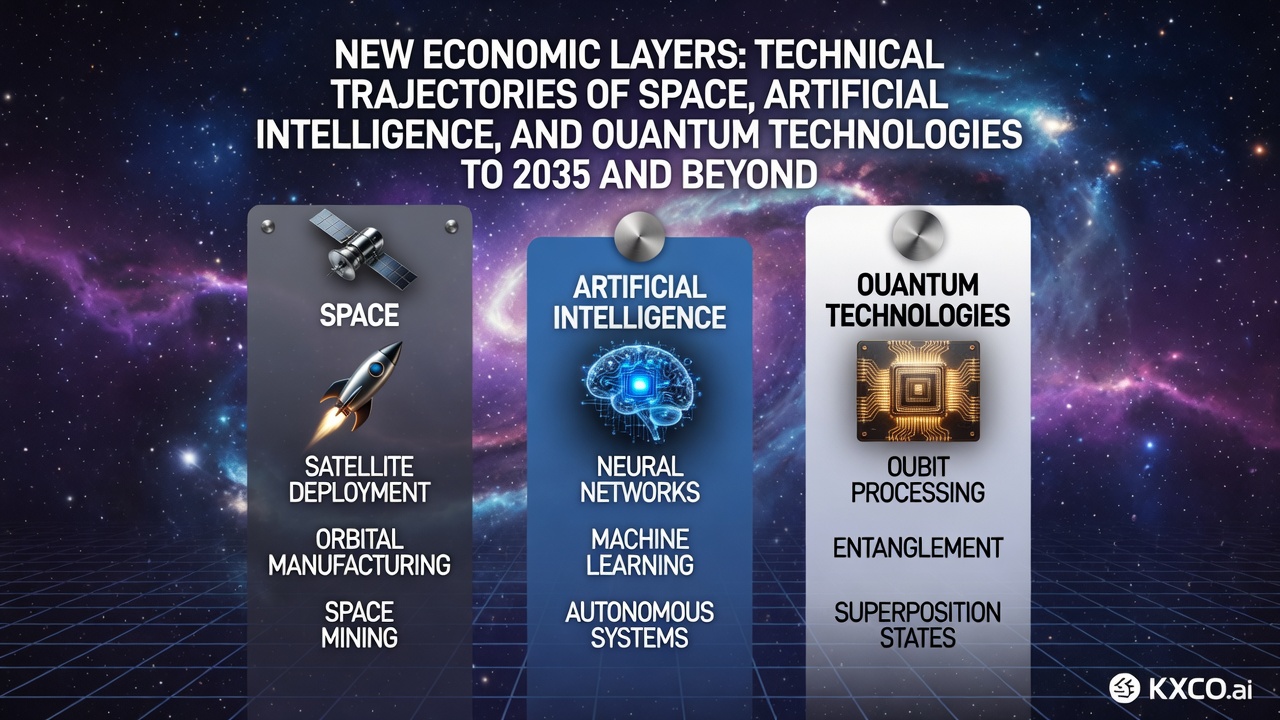

The New Economies: Space, AI, and Quantum

Three new economic layers are taking shape: space is becoming an industrial domain, artificial intelligence is evolving into continuous infrastructure, and quantum technologies are moving into operational use in simulation and sensing. While technical and energy constraints remain significant, the period through 2035 is likely to see these layers expand in parallel, creating new requirements for verifiable trust and post-quantum security. KXCO is positioning its infrastructure as the transaction

Inside Saudi PIF: $900 Billion Portfolio

Saudi Arabia’s Public Investment Fund (PIF) manages over $900 billion. This analysis covers its investments by sector and geography, major project updates including Qiddiya and HUMAIN, and the 2026–2030 strategy.

The SpaceX IPO, Is It a Buy Now

SpaceX completed the largest IPO in history with a $75 billion raise at a $1.75 trillion valuation. While the stock popped nearly 20% on debut, the analysis suggests $SPCX becomes a more compelling long-term buy below $100.

The New AI-Quantum Arms Race

The world’s leading tech CEOs are now aligned on one thing: AI and quantum computing are converging into hybrid systems that will unlock new capabilities in markets, scientific discovery, and strategic competition. The companies that build the most effective infrastructure layers will define the next era of computational advantage.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.