The SpaceX IPO, Is It a Buy Now

SpaceX ($SPCX): Buy Below $100 After $2 Trillion Debut

SpaceX ($SPCX) Completes Largest IPO in History: $75 Billion Raise at $1.75 Trillion Valuation, Shares Surge on Debut

On June 12, 2026, Space Exploration Technologies Corp. ($SPCX) executed the largest initial public offering in stock market history. The company sold 555,555,555 new shares at $135 each, raising $75 billion in primary proceeds at a $1.75 trillion valuation. Shares opened at $150 on Nasdaq, reached an intraday high of $176.52, and closed near $161 — up approximately 19% on the first day of trading — briefly pushing the market capitalization above $2 trillion.

Elon Musk became the world’s first trillionaire as a result of the listing and the subsequent pop in his SpaceX holdings (combined with his Tesla stake and other assets). The IPO followed a confidential SEC filing in April, a public S-1 on May 20, and an accelerated roadshow that demonstrated exceptionally strong demand.

This was not merely a large capital raise. It was the public market debut of a company that now spans reusable launch vehicles, the world’s largest satellite broadband constellation, and a rapidly scaling AI and compute infrastructure business following the integration of xAI.

IPO Structure and Key Mechanics

SpaceX structured the offering as an all-primary transaction, meaning the full $75 billion went directly to the company rather than to selling shareholders. The deal was led by Goldman Sachs as lead left bookrunner, with Morgan Stanley (serving as stabilization agent), Bank of America Securities, Citigroup, and JPMorgan Chase as joint book-running managers. A broader syndicate of more than 20 banks participated.

In a notable departure from standard practice, SpaceX set a fixed price of $135 rather than marketing a range and adjusting based on feedback. The offering included a standard 15% greenshoe (overallotment) option, giving underwriters the ability to purchase up to an additional ~83.3 million shares (approximately $11.25 billion more) within 30 days to support stabilization or meet excess demand. As of June 14, the base $75 billion raise has been confirmed; the status of any greenshoe exercise has not yet been finalized in public reporting.

The company also included a directed share program for employees and other designated parties, broadening participation beyond traditional institutional allocations.

Valuation Context and Financial Snapshot

SpaceX’s path to public markets included several private tender offers. A December 2025 secondary transaction implied a valuation near $800 billion. The February 2026 xAI integration was valued around $1.25 trillion at the time. The IPO represented another significant step-up to $1.75 trillion at pricing, with trading quickly taking the market cap above $2 trillion.

On 2025 revenue of $18.67 billion, the valuation implies very high multiples. However, the business mix is shifting rapidly toward higher-growth areas.

2025 Segment Performance (from S-1 data):

Segment | Revenue | Operating Income | Adj. EBITDA | Key Notes |

|---|---|---|---|---|

Connectivity (Starlink) | $11.39B | +$4.42B | +$7.17B | Strongest segment; high margins |

Space (Launches) | $4.09B | Negative | +$653M | Strategic but lower margin today |

AI (xAI-integrated) | $3.20B | Large negative | Negative | Heavy capex phase |

Total | $18.67B | -$2.59B | +$6.58B | Consolidated view |

Q1 2026 revenue reached $4.69 billion with continued growth in Connectivity and AI infrastructure buildout. The company remains unprofitable at the consolidated level due to heavy investment in Starship development and AI compute capacity.

Major Shareholders and Governance

Elon Musk holds the largest economic stake at approximately 42–46% of shares outstanding following the IPO. Through a dual-class share structure (Class B shares carrying 10 votes each), he controls roughly 82% of the voting power. This gives him the ability to elect the majority of the board. SpaceX qualifies as a “controlled company” under Nasdaq rules and has elected certain governance exemptions.

Other significant holders include long-term investors such as Valor Management (Antonio Gracias, ~3.8%), early backers with ties to Founders Fund (including Luke Nosek), Baron Capital, Fidelity, and specialist firms like 137 Ventures, which built a meaningful stake over more than a decade through secondary purchases.

Who Benefited Most from the IPO

The listing created substantial wealth across the cap table:

Elon Musk saw his net worth cross $1 trillion for the first time.

Early institutional investors realized enormous markups. 137 Ventures’ long-held position is now valued in the range of $20 billion at current levels.

Executives and employees were major beneficiaries. COO Gwynne Shotwell’s equity reached an estimated $1.3–1.7 billion. Reports indicated that roughly 4,400 employees became millionaires through vested equity and the post-IPO price action. Long-tenured staff who received options or grants years earlier saw life-changing outcomes.

Pre-IPO tender offers had already provided partial liquidity to some insiders and employees at rising private valuations.

SpaceX’s Core Businesses: Rockets, Starlink, and AI/Compute

SpaceX operates across three segments:

Space Segment Reusable launch vehicles remain foundational. Falcon 9 has flown hundreds of missions with >99% success. Falcon Heavy provides heavy-lift capability. Starship — the fully reusable next-generation vehicle — is the critical catalyst for dramatically lower costs to orbit and higher launch cadence. Starshield serves government and national security customers.

SpaceX catches Starship rocket booster in dramatic landing during fifth flight test

Connectivity Segment (Starlink) This is currently the most profitable and cash-generative part of the business. The constellation comprises roughly 9,600+ satellites in low Earth orbit. Residential and enterprise subscribers reached approximately 10.3 million by Q1 2026 across more than 160 countries. Direct-to-cell/mobile services are expanding through partnerships with mobile operators. Next-generation V3 satellites, with significantly higher capacity, will be deployed using Starship.

AI and Compute Segment Following the February 2026 integration of xAI, SpaceX consolidated Grok frontier models, API and enterprise offerings, and large-scale terrestrial compute clusters (COLOSSUS and COLOSSUS II). The company is also advancing Terafab, a semiconductor initiative with Tesla and Intel aimed at designing and manufacturing advanced AI chips at scale in Texas.

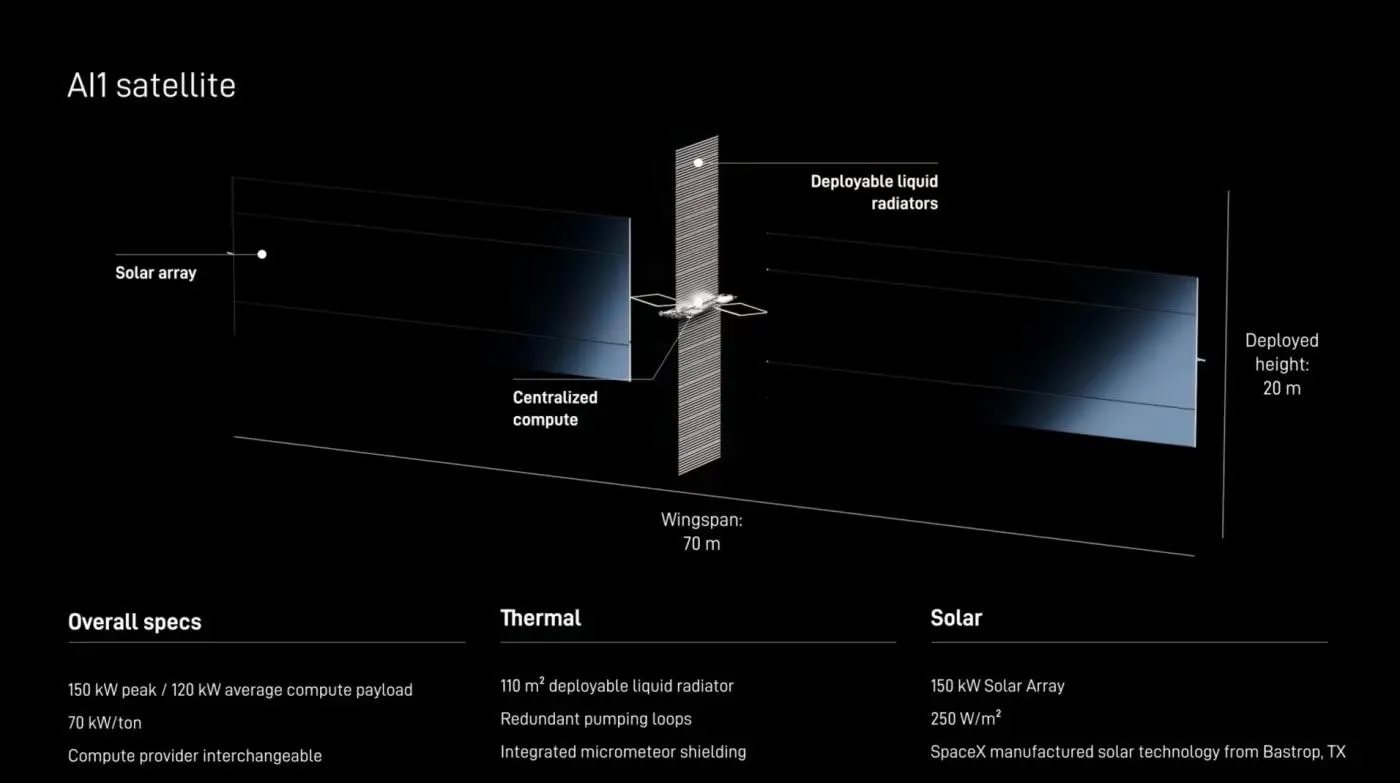

The most ambitious element is orbital AI compute — plans to deploy solar-powered satellite-based data centers using Starship’s payload capacity. The long-term thesis involves leveraging space-based solar power and Starlink connectivity to deliver large-scale, lower-cost AI inference and training capacity.

Risks and Considerations

The valuation leaves limited room for near-term disappointment. Consolidated losses continue amid heavy capital expenditure on Starship and AI infrastructure. Starship must achieve reliable, high-cadence operations. Regulatory approvals (FAA, FCC, export controls) and competition in both launch services and broadband remain relevant. Musk’s attention is divided across multiple major companies. The dual-class structure concentrates control but has drawn governance commentary from some institutional observers.

Price Outlook: 1 Month, 1 Year, and 5 Years

Large, hyped IPOs have historically shown significant volatility. Many deliver strong debuts followed by corrections of 30–50%+ within the first year as lockups expire, reality sets in, or macro conditions shift. A smaller number compound over time when execution is strong.

Near term (next 30 days): Expect volatility. A pullback toward $120–145 would be consistent with typical post-IPO behavior after a large pop. The $135 IPO price and recent private tender levels provide reference points. Strong AI narrative momentum could keep the stock elevated, but profit-taking and analyst commentary on valuation are likely.

One year: A wide range of $90–180 is plausible. Key catalysts include Starship flight cadence and payload success, Starlink subscriber growth and margin expansion, visible progress on AI compute revenue and Terafab, and any early orbital infrastructure milestones. Macro factors (interest rates, AI spending trends) will also matter. Sub-$100 levels on any meaningful weakness would represent an attractive entry zone for long-term investors.

Five years: Outcomes are highly asymmetric and execution-dependent. In a strong bull case, Starship enables routine high-volume launches, Starlink becomes global connectivity infrastructure, and orbital + terrestrial AI compute delivers meaningful scale and returns. This could support a multi-trillion-dollar (or significantly higher) valuation. A base case might see the stock in the $150–300 range with solid but slower progress toward sustained profitability. A bear case (prolonged Starship delays, AI capex without commensurate returns, or increased competition) could see the shares trade materially lower.

Entry point view: For investors with a multi-year horizon who believe in the combined space + AI infrastructure thesis, sub $100 offers a more comfortable margin of safety relative to current levels and the risks involved. Those comfortable with volatility may choose to build positions on dips from here while monitoring operational milestones closely.

Bottom Line

SpaceX’s IPO delivered exactly what the most bullish observers expected in terms of scale: a record $75 billion primary raise at a $1.75 trillion valuation, followed by a strong debut that quickly took the market cap above $2 trillion. The company enters public markets with a profitable and growing Starlink business, dominant launch capabilities, and an ambitious AI/compute platform that includes both terrestrial clusters and long-term orbital ambitions.

The stock will be volatile. Execution on Starship cadence, Starlink economics, and AI infrastructure returns will determine whether the current valuation proves justified over time. For readers focused on long-term infrastructure and technology trends, the coming quarters will provide important data points on whether SpaceX can translate its private-market momentum into sustained public-market performance.

Data as of mid-June 2026. This is for informational purposes only and does not constitute investment advice. IPO outcomes and stock prices can be highly volatile. Conduct your own research and consult professional advisors as needed.

SpaceX’s AI Satellites: Revolution in AI Compute

SpaceX’s AI satellites (SPCX) will deliver massive low-cost orbital compute using Nvidia then custom D3 chips from Terafab, powering xAI/Grok while creating major tailwinds for $TSLA $NVDA $GOOGL and $ANTH.

The Compute Market Boom

BlackRock CEO Larry Fink’s recent endorsement of compute as a new asset class, the impending launch of CME compute futures, massive hyperscaler deals such as Google’s $920 million monthly commitment to SpaceX

Strong Bull Case for Wall Street

This Wall Street weekly outlook presents the bullish case for $BTC, $NVDA, $TSLA, and the highly anticipated IPOs of Anthropic ($ANTH) and SpaceX ($SPCX).

Saylor Is Buying What $IBIT Holders Are Selling — At Scale

Michael Saylor is systematically buying Bitcoin while BlackRock’s IBIT ETF experiences repeated outflows. In 2026 alone, Strategy has acquired more Bitcoin than the entire mining network has produced.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.