Is the Iran War Back?

US strikes on Iran have reignited the danger trade — and the bigger story is the money printing almost no one is watching.

Part of theGold Forecast Center

Is the Iran war back? That is the question every trader I know was asking on Friday morning, and by the time the sun was up over the Gulf the answer looked uncomfortably close to yes.

On Friday, June 26, US Central Command put aircraft over Iranian territory and struck missile and drone storage sites along with coastal radar installations. Iranian media reported explosions on Sirik Island in Hormozgan province, with at least two projectiles hitting a telecommunications tower. This was the first American military action against Iran since the two countries signed a memorandum of understanding on June 17 — barely nine days earlier — that was supposed to be the framework for a permanent peace.

Nine days. That is how long the calm lasted.

So let me answer the headline directly before we get into the money, because that is what most of you actually came here for. The war is not "back" in the sense of a full shooting war between the United States and Iran. What we have is something messier and, frankly, more dangerous for markets over the medium term: a ceasefire that nobody fully believes in, a chokepoint that controls a fifth of the world's seaborne oil, and two governments that read the same piece of paper and walked away with completely different ideas about what it said. That is the kind of setup that produces sharp, violent moves in commodities and risk assets — and it is the kind of setup I have spent thirty years positioning around.

I am going to walk you through what actually happened, why the Strait of Hormuz is the entire story, what it means for gold, Bitcoin and the defense names including Palantir, and then I am going to take you to the thing almost nobody on financial television wants to talk about while there are explosions to film: the United States government is printing money again, the data is now confirmed, and that — far more than any drone over the Gulf — is the trade of the decade.

What actually happened

Here is the sequence, because the order matters.

On June 17, President Trump and Iranian President Masoud Pezeshkian signed a memorandum of understanding aimed at building toward a permanent peace deal to end the war between the two nations. Part of that agreement reopened the Strait of Hormuz toll-free for sixty days. Think about that wording — "toll-free for sixty days." It tells you immediately that this was not a peace treaty. It was a commercial truce with an expiry date stapled to the front of it. A sixty-day window. A clock.

Then on Thursday, the Islamic Revolutionary Guard Corps issued warnings to vessels to "strictly refrain from any movement outside the designated routes." A number of ships had been taking an alternative route through the Strait rather than the one Tehran approved. Hours after that warning, an IRGC drone struck a Singapore-flagged cargo ship. Two US officials confirmed it to the press. Trump's own account was that the regime "shot at least four One Way Attack Drones at Ships transversing the Strait of Hormuz," with one drone solidly hitting the upper deck of a cargo ship — damage was done, but the vessel was able to proceed.

By Friday, CENTCOM had responded. The official line: "The unwarranted aggression against commercial shipping by Iranian forces clearly violated the ceasefire." Trump called the Iranian action a "foolish violation."

Iran, for its part, denied responsibility for the attack on the cargo ship and instead leaned into its position as the dominant coastal state on the Strait. Deputy Foreign Minister Kazem Gharibabadi made the argument that Iran's role as a coastal power has to be respected in any maritime arrangement — which is diplomatic language for "this is our water, and we will decide who passes and how."

So you have a dispute that is not really about whether anybody wants war. Both sides signed a piece of paper trying to avoid one. The dispute is about who controls the most important stretch of water on the planet, and whether ships transit on Washington's terms or Tehran's. That is a far harder problem to solve than a simple "stop shooting" ceasefire, and it is why I do not trust this calm to hold.

The Strait of Hormuz is the whole story

If you take one thing away from this piece, take this: the Strait of Hormuz is the most important twenty-one miles of water in the global economy, and everything else — the drones, the radar sites, the diplomatic statements — is noise around that single fact.

Roughly a fifth of the world's oil that moves by sea passes through Hormuz. Crude out of Saudi Arabia, the UAE, Kuwait, Iraq, Iran itself, and a huge volume of liquefied natural gas out of Qatar — it all funnels through a channel that at its narrowest is barely wide enough for two shipping lanes. There is no real alternative at scale. There are a couple of pipelines that can bypass it, but they cannot come close to handling the volume that moves through the Strait every single day. If Hormuz closes, or even if shipping insurers decide it is too risky to transit and rates spike, the price of oil does not move politely. It gaps.

And that is the part traders need to internalize. The market is not pricing a closed Strait right now — if it were, oil would be forty or fifty dollars a barrel higher and we would be having a very different conversation. What the market is doing is what it always does at the start of one of these episodes: it is sitting on its hands, waiting to see whether this is a flare-up that burns out in a week or the first chapter of something that runs for months. The professionals are watching tanker tracking data and insurance war-risk premiums far more closely than they are watching the cable news chyron.

My read? The sixty-day toll-free window is the tell. We are nine days in. That gives both sides roughly seven weeks of runway during which every shipping incident, every drone, every "designated route" dispute is a potential trigger. The structure of this agreement practically guarantees more incidents, because it left the single most contentious question — who controls passage — deliberately vague so that something could be signed at all. Vague agreements between adversaries do not produce lasting peace. They produce exactly what we saw on Friday.

This is why I am not treating the Friday strikes as a one-off to be faded. I am treating them as confirmation that the risk premium needs to stay in the portfolio.

How markets are reading it — and how they should be

Let me be honest about something, because I do not believe in selling you a panic you can see for yourself is not in the price.

As I write this, the immediate market reaction has been measured. Gold is firm but it is not spiking vertically. Oil is up but it is not limit-bid. Bitcoin is actually weak — more on that in a minute, because the reason is fascinating and it is not about Iran. Equity futures wobbled and steadied. If you only looked at the tape and not the headlines, you would not necessarily know a US carrier strike group had just hit Iranian soil.

There are two ways to read that. The lazy way is to say "the market doesn't care, nothing to see here, move on." I think that is wrong, and I think it is the kind of complacency that gets people hurt.

The correct way to read it is that the market has been conditioned by the last two years of on-again, off-again Middle East escalation to assume every flare-up de-escalates. Traders have been trained, repeatedly, that buying the dip on geopolitical fear pays. And most of the time, over the last cycle, it has. The problem with that conditioning is that it works right up until the one time it doesn't — and a structurally unstable ceasefire over the world's most important oil chokepoint is precisely the kind of situation where the pattern can break.

So I am not chasing a fear spike that has not happened. What I am doing is making sure I own the assets that pay off if the seven-week clock runs out badly, while those assets are still reasonably priced. That is a very different posture from panic. It is insurance bought before the storm, not after.

Three places I want that exposure: gold, Bitcoin, and the defense complex including Palantir. Let me take them in order.

Gold — buy it, and keep buying it

I have been a gold bull for a long time and I am not about to stop now, with the metal trading above four thousand dollars an ounce and sitting near record territory.

Let me deal with the obvious objection first. "Shayne, gold is at an all-time high, isn't it too late?" No. And I want to explain why that question, while natural, is the wrong frame entirely.

Gold at four thousand dollars is not expensive because of a number on a screen. Gold is a measuring stick. When the price of gold goes up, what is actually happening most of the time is that the thing you are measuring it in — the dollar, the euro, the yen — is getting smaller. Asking whether gold is "too high" is a bit like standing on a beach with the tide coming in and asking whether the water is too high. The water is not the variable. The thing it is rising against is.

And right now gold has two engines running at once, which is rare.

The first engine is the one we have just spent two thousand words on: geopolitical risk. When US aircraft are striking Iranian radar sites and the Strait of Hormuz is in play, money looks for somewhere to hide that does not have counterparty risk, does not depend on any government's promise, and cannot be sanctioned, frozen, or printed. That is gold. It has been gold for five thousand years and a drone strike in the Gulf does not change the thesis — it reinforces it.

The second engine is structural and far more powerful, and it has been running underneath the price for three years now: central banks are buying. Not Western retail investors chasing a chart — central banks, the most price-insensitive buyers on earth, accumulating physical gold quarter after quarter to diversify away from the dollar. They watched what happened when reserves got frozen in recent years and they drew the obvious conclusion: a reserve you do not physically hold is a reserve someone else can switch off. That realization does not reverse in a quarter. It is a multi-year, possibly multi-decade reallocation, and it puts a floor under this market that did not exist in previous cycles.

Stack the geopolitical engine on top of the central-bank engine and then — this is the part I will come back to — stack the return of US money printing on top of both, and you have the strongest fundamental case for gold I have seen in my career.

So yes, I am a buyer of gold here. Not all at once at a record high — I am not reckless — but on any pullback, and as a core holding I have no intention of trimming. If you own none, you have a problem, and Friday's strikes are as good a reason as any to fix it. If the Hormuz situation deteriorates, gold is your single best-protected position. And if it somehow resolves peacefully, the monetary backdrop alone keeps the bid intact. That is what I want in a holding — a position that wins in the bad scenario and still works in the good one.

Bitcoin — the contrarian buy nobody wants right now

Now for the interesting one, because Bitcoin is doing something that surprises people who only understand it as "digital gold."

As I write, Bitcoin ($BTC) is trading near sixty thousand dollars. The intraday range has been roughly fifty-eight to sixty-one thousand. The Fear and Greed Index is sitting at thirteen — that is "Extreme Fear." And here is the number that should make you sit up: Bitcoin is down something like forty-eight thousand dollars from where it traded a year ago. This is an asset that has been cut roughly in half from its highs.

So the obvious question: if there is a war scare and gold is the safe haven, why is "digital gold" getting hit?

Because in the short term Bitcoin is not trading as digital gold. It is trading as the most sensitive risk asset on the board. When fear spikes and people de-risk, the highest-beta, most-speculative positions get sold first, and for the last couple of years Bitcoin has behaved far more like a leveraged Nasdaq bet than like bullion. A geopolitical shock makes people reduce risk, and Bitcoin is the purest expression of risk in most portfolios. That is why it is weak into a war scare while gold is firm. They are not contradicting each other — they are doing exactly what their current market personalities dictate.

Now, why am I a buyer of that weakness?

Three reasons.

First, the sentiment. An Extreme Fear reading of thirteen is not a sell signal — historically it is the opposite. The best entries in this asset have almost always come when the Fear and Greed Index is buried in the single digits to low teens and everyone you talk to is either silent about crypto or openly disgusted by it. When the crowd is euphoric at the top, you sell. When the crowd is in extreme fear and an asset is down by half, you do your buying. I am not telling you it cannot go lower in the short term — it absolutely can. I am telling you that buying extreme fear in a structurally sound asset is how fortunes get built, and selling it is how they get lost.

Second, the long-term thesis is the same thesis as gold, and it is getting stronger by the day, not weaker. Bitcoin is a fixed-supply, twenty-one-million-coin, un-printable, un-inflatable, un-confiscatable bearer asset. In a world where — as I am about to show you — the United States is back to expanding its balance sheet and the national debt has blown through thirty-nine trillion dollars, the case for owning a hard-capped digital asset does not get weaker when the price falls. It gets more compelling, because you are being handed the same insurance policy at half the premium.

Third — and this is the part that matters for timing — Bitcoin's correlation with risk assets is not permanent. It flips. There have been long stretches where Bitcoin decoupled from equities entirely and traded on its own monetary logic. The current "risk-on proxy" personality is a phase, not a law of nature. When the monetary debasement story becomes the dominant market narrative — and I think the data is about to force that — Bitcoin's character can shift back toward the digital-gold framing, and that re-rating happens fast and violently to the upside.

So I treat Bitcoin near sixty thousand, with sentiment at extreme fear and the price halved from its highs, as exactly the sort of asymmetric setup I want to be buying. I am not betting the house. I am scaling in, the same way I scale into gold on weakness. The difference is that with Bitcoin the weakness is here right now, on a plate, while everyone else is too scared to touch it. That is usually the tell that it is time to do some buying.

To be clear about risk, because I will not pretend otherwise: Bitcoin is volatile, it can and does fall another twenty or thirty percent in these phases, and it is not a position you put money you need in the next year into. But as a long-term holding for the debasement thesis, bought into extreme fear, I am comfortable being a buyer here and I am acting on it.

War stocks — and yes, Palantir belongs on the list

When the bombs start falling, the defense sector is where the institutional money goes, and there is nothing cynical about saying so. Governments respond to conflict by spending, and a handful of companies capture the overwhelming majority of that spending. This is one of the most reliable patterns in markets, and Friday's strikes are a reminder of why these names belong in a portfolio that is positioned for an unstable world.

Start with the traditional primes, because the numbers are doing the talking.

Lockheed Martin ($LMT) just locked in roughly forty-three and a half billion dollars in new defense contracts. Forty-three and a half billion. The stock is trading around five hundred and ten dollars and it has been one of the steadier large-caps in the entire market — which is exactly what you want from a defense holding. You are not buying Lockheed for a moonshot. You are buying it for a fortress balance sheet, a contract backlog measured in years, a dividend, and a business whose biggest customer is a government that is structurally committed to spending more, not less, on hardware. When the Strait of Hormuz is contested and US assets are striking Iranian soil, Lockheed's order book does not shrink.

RTX ($RTX) — the company most of us still think of as Raytheon — is trading near a hundred and ninety dollars with a market cap around a quarter of a trillion. Their guidance for 2026 is in the region of ninety-two to ninety-three billion dollars in sales, with mid-single-digit organic growth, earnings of roughly six dollars seventy to six dollars ninety a share, and free cash flow in the eight-and-a-quarter to eight-and-three-quarter billion range. Raytheon makes missiles and missile defense. In a world where the headlines are about drones and missile and radar sites, I do not think I need to draw you a diagram about where that revenue trends.

Those two are the anchors. Around them I would have you look at Northrop Grumman ($NOC) and General Dynamics ($GD) as well — the same logic applies. These are not exciting businesses. They are not supposed to be. They are the slow-and-steady ballast that performs when the world gets dangerous, and the world just got more dangerous on Friday.

But the name I really want to talk about is Palantir ($PLTR), because that is where the opportunity is, and it is the most controversial call in this entire piece.

Here is the situation. Palantir is trading around a hundred and seven dollars, and it has just set a fifty-two-week low. The stock is down roughly forty percent year to date. Its fifty-two-week range runs from about a hundred and six dollars all the way up to two hundred and seven — so it has fallen from over two hundred to barely above a hundred. The crowd has decided Palantir is a busted story: the valuation got stretched, macro got uncertain, and there is a fashionable fear that new AI models will somehow disrupt its software moat.

I think the crowd is wrong, and I think this is a gift.

Let me make the case. Palantir is not really a "software stock" in the way the market is currently punishing it. Palantir is the company that sits at the intersection of the two most durable spending trends on the planet: defense and artificial intelligence. Its core business is taking enormous, messy streams of data — battlefield data, intelligence data, logistics data — and turning them into something a commander or an analyst can actually act on in real time. When you read that CENTCOM struck "missile and drone storage locations and coastal radar sites," the targeting, the fusion of sensor data, the operational picture behind a strike like that is exactly the category of problem Palantir's platforms are built to solve. This is not a company that benefits from war in some vague thematic sense. It is a company embedded in the actual machinery of modern military and intelligence operations.

Now layer the AI piece on top. The fear that "new AI models will disrupt Palantir" has it exactly backwards. Palantir's advantage was never a particular model — it is the deployment, the security clearances, the data integration, the years-long government relationships, and the operational trust that you cannot replicate with a clever model and a weekend hackathon. The proliferation of powerful AI models makes Palantir's ability to deploy them, securely, inside the most sensitive environments on earth more valuable, not less. The model is the commodity. The trusted pipeline into the Pentagon and the intelligence community is the moat.

And here is the part that tells me the selling is sentiment, not substance: the analysts who actually cover this name closely have an average twelve-month price target around a hundred and eighty-three dollars, with a high estimate of two hundred and fifty-five. Twenty of them rate it a buy against a couple of sells, for an overall buy rating. That is a stock the professional community thinks is worth seventy-some percent more than where it trades today, sitting at a fifty-two-week low because the momentum crowd that piled in at two hundred has capitulated.

That is the setup I spend my career looking for: a structurally advantaged business, in the right two industries at the right moment, marked down forty percent by a crowd that bought the top and panicked at the bottom. So yes — I am putting Palantir on the buy list, right alongside Lockheed and RTX. The difference is that with the primes you are buying stability, and with Palantir you are buying a beaten-down growth asset that the market has temporarily decided to hate. I will take both.

Here is the war complex at a glance — three names I want to own into a more dangerous world, with the numbers as of Friday's close:

Stock | Ticker | Price (Jun 26) | Catalyst / why it is here | My call |

|---|---|---|---|---|

Palantir | ~$107 | 52-week low, down ~40% YTD; average analyst target ~$183 | Buy — asymmetric | |

Lockheed Martin | ~$510 | Just booked ~$43.5B in new defense contracts | Buy — ballast | |

RTX (Raytheon) | ~$190 | FY26 guide ~$92–93B sales; missiles & air defense | Buy — ballast |

A word of discipline on all of these: defense names and Palantir especially can stay volatile, and Palantir at a fifty-two-week low can make a new fifty-two-week low before it turns. Scale in. Do not back up the truck in a single print. But the direction of travel is clear to me, and the Friday strikes only sharpen it.

The real story: they are printing money again

Now we get to the part that matters more than anything else in this article, and the part that almost nobody connects to the war headlines even though they are two sides of the same coin.

While everyone was watching the Gulf, the monetary data quietly confirmed something I have been warning about: the United States is printing money again. Not as an emergency. As a policy. And the numbers are no longer a forecast — they are in the official releases.

Let me give you the figures, because they are extraordinary and they deserve to be stated plainly.

The M2 money supply — the broad measure of money sloshing around the US economy — rose to roughly twenty-three trillion dollars as of the end of May 2026. That is a record high. It took out the previous peak from earlier this year and it is climbing again after the brief period of contraction that followed the rate-hiking cycle. Money supply growth has accelerated to a multi-year high.

Why is it growing again? Because the Federal Reserve has restarted quantitative easing. In December the Fed announced it was returning to asset purchases, and it is now buying on the order of forty billion dollars a month in Treasuries. The central bank's balance sheet, which had been shrinking from its pandemic peak near nine trillion dollars, has turned around — it is back up around six point seven trillion and rising, having expanded by more than two hundred billion dollars since the QE restart. Up fifty-five billion in a single recent year-over-year comparison and growing week over week.

Let me translate "the Fed is buying forty billion a month in Treasuries" out of central-bank dialect and into plain English, because the euphemisms are designed to make this sound boring and technical. The government spends far more than it collects in taxes. To cover the gap, the Treasury issues bonds — IOUs. Normally those IOUs have to be bought by real savers, real institutions, real foreign governments, with real existing money. But when the central bank steps in and buys those bonds, it does so with money it creates out of nothing, on a keyboard, that did not exist a second earlier. That is what quantitative easing is. It is the government funding its own deficit with freshly created money. It is, in the most literal sense available, printing.

And the deficit they are funding is enormous. The budget deficit ran about one point two trillion dollars in just the first eight months of fiscal 2026 — October through May. Federal debt held by the public hit thirty-one and a half trillion at the end of May, up two point six trillion from a year earlier. And the total national debt — the headline number — has now blown clean through thirty-nine trillion dollars, sitting around thirty-nine point three trillion as of late June. Even Janet Yellen, hardly a fiscal hawk, warned earlier this year that the debt is approaching a red line that economists have cautioned about for decades.

Now hold two facts next to each other, because this is the whole game.

Fact one: the Fed held its policy rate steady in June, at three and a half to three and three-quarter percent. On the surface, that looks like a central bank standing firm, keeping money tight, fighting inflation.

Fact two: at the very same time, that same central bank is buying forty billion dollars a month in government bonds and its balance sheet is expanding.

Those two things together are not "tight money." They are something far more cynical and far more important to understand. The headline interest rate is the thing the public watches, so it is held up as evidence of discipline. The balance sheet is the thing the public does not understand, so that is where the actual money creation is happening, quietly, in the back. They are showing you a firm hand on the rate while the other hand runs the printing press. This is the oldest trick in the monetary book, and it has a name that economists are increasingly willing to say out loud: fiscal dominance. It is what happens when a government's debt gets so large that the central bank can no longer set policy purely to fight inflation — it has to keep the government's borrowing costs manageable, which means it has to keep buying the debt, which means it has to keep printing. The tail wags the dog.

This is the single most important macro fact in the world right now, and it is bigger than Iran. The Iran story is a catalyst. The money-printing story is the trend. Catalysts come and go — a ceasefire holds, a ceasefire breaks, a drone hits a ship, a drone misses. Trends compound. And the trend is that the purchasing power of the dollar in your bank account is being systematically diluted to fund a government that cannot stop spending and a debt that can no longer be repaid in honest money — only inflated away.

Connecting the dots — this is one trade, not four

Here is where it all comes together, and why I have walked you through war, gold, Bitcoin, defense and money-printing in a single piece instead of four separate ones. They are not four separate ideas. They are one idea wearing four costumes.

The world is becoming more dangerous and more multipolar — Friday's strikes on Iran are a symptom of that. Governments respond to a more dangerous world by spending more on defense, which they fund by borrowing more, which pushes the debt to levels that can never be honestly repaid, which forces the central bank to print money to keep the whole structure from collapsing, which debases the currency, which drives capital into the only assets that cannot be printed: gold, Bitcoin, and the equity of the companies that profit from the danger itself.

It is a closed loop. War feeds spending feeds debt feeds printing feeds debasement feeds hard assets. And we are not at the start of that loop — we are well into it, with the data now confirming every link in the chain.

So when I tell you I am a buyer of gold above four thousand, a buyer of Bitcoin into extreme fear near sixty thousand, and a buyer of the war complex including a beaten-down Palantir, understand that these are not four bets. They are four expressions of one conviction: that the money is being debased, that the danger premium is rising, and that the people in charge have no politically survivable way to stop either process.

That is not a doom prophecy. I am not telling you the world is ending — quite the opposite. I am telling you that the world is doing something it has done many times before, and that there is a well-understood playbook for protecting and growing your wealth through it. The mistake is not the printing — you and I cannot stop that. The mistake is holding all your savings in the very instrument that is being printed, while it quietly loses value, and calling that "safe" because the number in the account does not change. The number does not change. What it buys does.

What I am actually doing

Let me close with specifics, because I do not like commentary that refuses to commit.

On gold, I am holding my core position and adding on any pullback. Above four thousand dollars I am not chasing vertical spikes, but I have no seller's instinct here whatsoever, and if Hormuz deteriorates I expect gold to be the cleanest-performing asset I own.

On Bitcoin, I am scaling into the weakness. Extreme fear at thirteen, the price halved from its highs near sixty thousand — that is a buying zone for a long-term holder, not a selling zone. I am not using money I need soon, I am sizing it as the volatile asset it is, and I am prepared for it to fall further before it turns. But I am buying.

On the war complex, I want Lockheed and RTX as the ballast — stable, contract-rich, dividend-paying, with order books that only grow in a world like this one. And I want Palantir as the asymmetric piece: a forty-percent-off, fifty-two-week-low entry into the company that sits exactly where defense meets artificial intelligence, with a professional analyst community that thinks it is worth seventy-odd percent more than today's price. Scale in, respect the volatility, but it is on my buy list and I am acting on it.

And on the dollar — on the money-printing story that underpins all of it — my position is simply to own less of it. To hold my wealth in things that cannot be created on a keyboard. That is the entire strategy, and everything above is just the specific implementation of it.

Is the Iran war back? Maybe, maybe not — that depends on the next seven weeks and on whether two governments who do not trust each other can manage a chokepoint neither fully controls. But here is what I know for certain, because it is printed in the official data and not in a cable-news headline: the money is being printed, the debt is past thirty-nine trillion, the Fed's balance sheet is expanding again, and gold is at a record for a reason. Position accordingly.

Shayne Heffernan is a trader and the founder of KXCO. The views above are his own market opinion and are provided for information and discussion only. Nothing in this article is personal financial advice or a recommendation to buy or sell any security or asset. Markets carry risk, including the risk of total loss, and you should do your own research and consult a licensed professional before making any investment decision.

Palantir Stock (PLTR): BUY Rating, $250 Price Target — The 40% Dislocation

Palantir is down ~40% in 2026 even as Q1 revenue grew 85% and management guided FY2026 to $7.66B. Shayne Heffernan issues a BUY on PLTR with a $250 price target — full breakdown of the business, customers, five-year revenue, every major Wall Street bank target and the corporate outlook.

AI Is Still Early. Quantum Is Real.

Forget the lab feud. The week's real story is earnings — Micron's $100B order book proves AI demand is committed, not speculative. My featured US stocks: Micron, Amazon, a buy on Palantir, plus the government-backed quantum names.

SpaceX and the Space Economy

Space is no longer the domain of governments alone. Led by SpaceX and a growing ecosystem of launch providers, satellite operators, and lunar infrastructure companies, the space economy is rapidly becoming one of the world's most important growth industries and could represent the next great gold rush for investors.

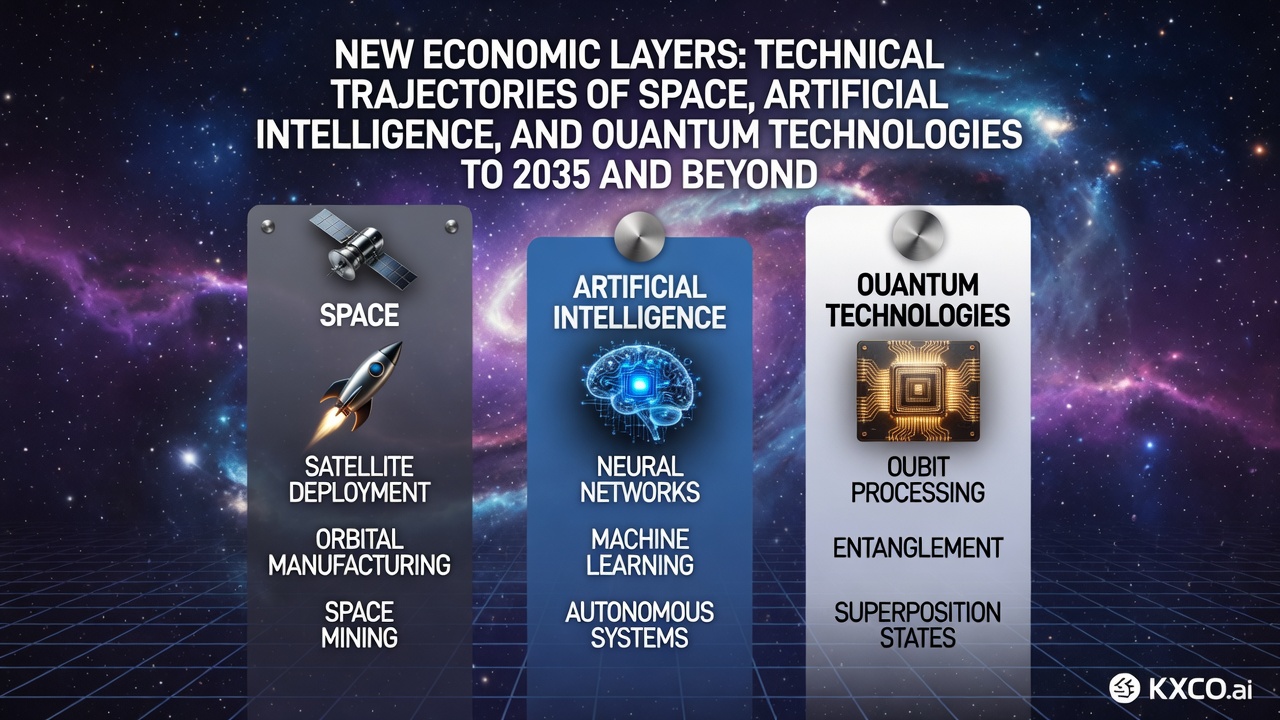

The New Economies: Space, AI, and Quantum

Three new economic layers are taking shape: space is becoming an industrial domain, artificial intelligence is evolving into continuous infrastructure, and quantum technologies are moving into operational use in simulation and sensing. While technical and energy constraints remain significant, the period through 2035 is likely to see these layers expand in parallel, creating new requirements for verifiable trust and post-quantum security. KXCO is positioning its infrastructure as the transaction

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.