Earnings Season Kicks Off

The AI Supercycle Is Just Getting Started $PLTR $NVDA $AMZN $MSFT $GOOGL $META $LMT $RTX $NOC $BA $AMAT $ASML $MU $LRCX $KLAC $AMD $INTC $TSLA $SPCX

Part of theAI Stocks Center

Earnings Season Kicks Off: The AI Supercycle Is Just Getting Started

Q2 2026 Preview — Why Nvidia and SpaceX Are the Big Winners to Watch

Live Trading News

July 14, 2026

Earnings season for the second quarter of 2026 kicks off this week, and the numbers are staggering. Analysts at FactSet project S&P 500 earnings growth of 23.3% year-over-year, driven by an 11.7% increase in revenues. All eleven sectors of the S&P 500 are expected to post positive earnings growth for the first time in over two years. For the full calendar year 2026, earnings are forecast to grow 24.1%, which would mark the strongest annual growth rate since the post-pandemic recovery of 2021. Financials will lead off the reporting cycle the week of July 13, with roughly 75% of the S&P 500 market capitalization set to report results by the end of the month. But the story of this earnings season is not the breadth of growth. The story is the concentration of growth in a handful of AI-driven companies that are redefining what is possible in corporate profitability, and two names stand above the rest: Nvidia and SpaceX.

The Q2 2026 earnings season arrives against a macroeconomic backdrop that is, by most measures, remarkably supportive. The U.S. economy continues to expand, unemployment remains near historic lows, and the Federal Reserve has maintained a rate posture that has allowed risk assets to flourish. But the earnings growth we are about to witness is not simply a function of a strong economy. It is a function of a structural transformation in how the world's largest companies generate revenue and profit. Artificial intelligence has moved from the lab to the income statement, and the companies that have positioned themselves at the center of the AI value chain are posting numbers that would have seemed fantastical just two years ago.

FactSet's latest Earnings Insight report projects that earnings estimates for Q2 2026 actually increased by 3.4% from March 31 to June 30, a phenomenon known as a positive earnings revision cycle. In most quarters, estimates drift downward as the reporting date approaches. The fact that estimates are being revised upward heading into earnings season is a powerful signal that analysts are consistently underestimating the profitability of AI-adjacent businesses. The Communication Services sector is expected to lead all sectors in earnings growth, followed by Information Technology and Industrials. Energy, which has been a drag on aggregate earnings for several quarters, is also expected to contribute positively. This broad-based improvement in earnings quality is rare and historically bullish for equity markets.

FACT SET: Q2 2026 Earnings Season Snapshot | |

S&P 500 Earnings Growth (YoY) | +23.3% (FactSet consensus) |

S&P 500 Revenue Growth (YoY) | +11.7% |

Sectors with Positive Growth | All 11 sectors |

CY2026 Full-Year Earnings Growth Forecast | +24.1% |

Earnings Estimate Revision (Mar 31 to Jun 30) | +3.4% (upward) |

Reporting Kickoff | Week of July 13, 2026 (Financials) |

S&P 500 Market Cap Reporting by Month End | ~75% |

Table 1: Q2 2026 earnings season key metrics. Sources: FactSet, Interactive Investor, Forbes.

Sector | Est. Q2 2026 Earnings Growth | Key Drivers |

|---|---|---|

Communication Services | Highest growth rate | |

Information Technology | Well above average | Nvidia $NVDA, Microsoft $MSFT, AMD $AMD, semiconductor demand |

Industrials | Above average | Defense AI (Palantir $PLTR, RTX $RTX, Northrop $NOC), Boeing $BA recovery |

Financials | Above average | Bank earnings lead-off, AI-driven trading and lending efficiency |

Health Care | Moderate growth | AI drug discovery, operational efficiency |

Consumer Discretionary | Moderate growth | |

Energy | Positive contribution | Oil price stabilization, refiner margins |

Materials | Modest growth | Semiconductor materials demand (Micron $MU) |

Utilities | Modest growth | Data center power demand |

Real Estate | Modest growth | Data center REITs benefiting from AI capex |

Consumer Staples | Lowest but positive | Pricing power, margin expansion |

Table 2: Estimated Q2 2026 earnings growth by S&P 500 sector. Sources: FactSet, analyst consensus estimates.

The Big Winner: Nvidia $NVDA

Nvidia $NVDA has already reported for its fiscal Q2 2026 (ending May 2026), and the numbers confirm what the market has been pricing in: absolute dominance of the AI chip market. The company posted total revenue of $46.7 billion, up 56% year-over-year and up 6% sequentially. Data center revenue reached $41.1 billion, representing the overwhelming majority of total revenue and driven by insatiable demand for Blackwell architecture GPUs. The company guided Q3 revenue to approximately $54 billion, plus or minus 2%, a number that does not even assume any H20 chip shipments to China. Analysts are now projecting forward revenue of approximately $65 billion per quarter, implying a runway that extends well into 2027.

What makes Nvidia $NVDA the standout winner of this earnings season is not just the top-line growth, which is extraordinary by any standard. It is the margin profile. Nvidia's gross margins on Blackwell products are estimated to exceed 75%, making the company one of the most profitable hardware businesses in the history of the technology industry. The Blackwell architecture is seeing 17% sequential revenue growth, and supply remains constrained relative to demand. Every GPU Nvidia $NVDA can produce is being purchased, primarily by the hyperscalers who are in the midst of the most aggressive capital expenditure cycle in corporate history. The company's data center revenue alone now exceeds the total revenue of most Fortune 500 companies.

The competitive landscape remains favorable for Nvidia $NVDA, despite the best efforts of AMD $AMD, Intel $INTC, and the hyperscalers' own custom chip programs. Amazon $AMZN, Alphabet $GOOGL, and Microsoft $MSFT are all developing custom AI silicon to reduce their dependence on Nvidia, but these custom chips are years away from matching the performance and software ecosystem of Nvidia's CUDA platform. AMD $AMD provides the most credible alternative with its MI300 and MI400 series, but Nvidia's $NVDA market share in AI training chips remains above 80%. Intel $INTC, while making progress with its Gaudi accelerators, has largely been relegated to a secondary role. For the remainder of 2026 and into 2027, Nvidia $NVDA remains the undisputed king of AI compute, and its earnings trajectory reflects that dominance with crystal clarity.

FACT SET: Nvidia $NVDA Earnings Highlights | |

Q2 FY2026 Total Revenue | $46.7 billion (up 56% YoY, up 6% QoQ) |

Data Center Revenue | $41.1 billion |

Blackwell Sequential Growth | +17% |

Q3 FY2026 Revenue Guidance | ~$54 billion (plus or minus 2%) |

Analyst Forward Revenue Estimate | ~$65 billion per quarter |

Estimated Gross Margin (Blackwell) | >75% |

AI Training Chip Market Share | >80% |

Table 3: Nvidia financial highlights from fiscal Q2 2026 earnings. Sources: Nvidia investor relations, CNBC, analyst consensus.

The Wildcard: SpaceX $SPCX

SpaceX $SPCX is the most consequential IPO of 2026, and its debut has already rewritten the rules of the public markets. The company listed on the Nasdaq on June 12, 2026 under the ticker $SPCX, targeting a $2 trillion valuation. The stock closed its first full day of trading at $160.95, a 19% gain from its offering price, and has continued to appreciate as investors digest the company's extraordinary financial disclosures. SpaceX is not just a space company. It is an infrastructure company whose satellite constellation, launch services, and defense contracts create a revenue base that no competitor can replicate.

The financials that emerged from SpaceX's $SPCX IPO filing are remarkable. Total revenue reached $18.7 billion on a consolidated basis for the most recent fiscal year, with the Starlink satellite internet service generating approximately $7.2 billion in adjusted EBITDA, up 86% year-over-year. Starlink now accounts for roughly 61% of consolidated revenue and is converting approximately 85% of its revenue forecast into cash flow. The brand alone was valued at $5.19 billion in 2026, cracking the Brand Finance top 500 for the first time. For 2026, revenue is forecast to grow approximately 15% year-over-year, driven by Starlink subscriber growth, expanded launch cadence, and the $6.45 billion Golden Dome defense contract that positions SpaceX as a primary military contractor.

What makes SpaceX $SPCX a big winner this earnings season is not just the headline numbers, though those are impressive. It is the optionality. SpaceX operates in three massive addressable markets simultaneously: satellite communications, space launch, and defense. Starlink's subscriber base is growing at double-digit rates globally, and the service is expanding into enterprise and government markets. The launch business is booking record numbers of missions for both commercial and government customers. And the defense portfolio, anchored by the Golden Dome space layer contract, provides a recurring revenue stream with government backing that is essentially recession-proof. SpaceX $SPCX is a company that can grow 15% to 20% annually for the next decade, and the market is only beginning to price that in.

FACT SET: SpaceX $SPCX Financial Snapshot | |

IPO Date | June 12, 2026 (Nasdaq: $SPCX) |

First Day Close | $160.95 (+19% from offer price) |

Target Valuation | $2 trillion |

Consolidated Annual Revenue | $18.7 billion |

Starlink Revenue Share | ~61% of consolidated |

Starlink Adjusted EBITDA | $7.2 billion (up 86% YoY) |

Starlink Cash Conversion | ~85% of revenue |

Golden Dome Contract | $6.45 billion (space layer) |

2026 Revenue Growth Forecast | ~15% year-over-year |

Brand Value | $5.19 billion (Brand Finance 2026) |

Table 4: SpaceX financial and market data. Sources: Nasdaq, CNBC, Morningstar, Yahoo Finance, Brand Finance.

The Hyperscaler Capex Supercycle

The single most important driver of earnings growth across the technology sector is the unprecedented capital expenditure cycle being undertaken by the four hyperscalers: Amazon $AMZN, Microsoft $MSFT, Alphabet $GOOGL, and Meta $META. Collectively, these four companies plan to allocate approximately $725 billion to capital expenditures in 2026, an increase of 77% from the prior year. In Q1 2026 alone, the hyperscalers spent $130 billion on capital expenditures, with the full-year total now exceeding $750 billion across the group. This is the largest infrastructure investment cycle in the history of the technology industry, and it is almost entirely driven by the buildout of AI data center capacity.

Company | 2026 Capex Guidance | Change YoY | Primary Focus |

|---|---|---|---|

Amazon $AMZN | $200 billion | Significant increase | AWS data centers, Trainium/Inferentia chips, AI services |

Alphabet $GOOGL | $175-185 billion | Major increase | Google Cloud AI infrastructure, TPU expansion, DeepMind |

Meta $META | $115-135 billion | Up from $72B | AI training clusters, Llama model infrastructure, Reality Labs |

Microsoft $MSFT | Part of $725B total | Significant increase | Azure AI, OpenAI infrastructure, Copilot enterprise |

Combined Total | $725B+ (2026 est.) | +77% YoY | AI data center buildout across all four |

Q1 2026 Alone | $130 billion | Record quarterly pace | Accelerated AI infrastructure deployment |

Table 5: Hyperscaler 2026 capital expenditure plans. Sources: company earnings calls, Futurum Research, Data Center Richness.

This capex supercycle is the fundamental reason why Nvidia $NVDA, Applied Materials $AMAT, Lam Research $LRCX, KLA $KLAC, ASML $ASML, Micron $MU, and AMD $AMD are all experiencing extraordinary earnings growth. Every dollar the hyperscalers spend on AI infrastructure flows through the semiconductor value chain, creating a cascading effect that benefits companies at every tier. Nvidia $NVDA sells the GPUs. TSMC manufactures them using ASML $ASML lithography machines and equipment from Applied Materials $AMAT, Lam Research $LRCX, and KLA $KLAC. Micron $MU provides the high-bandwidth memory. AMD $AMD provides competitive alternatives. And the hyperscalers themselves, Amazon $AMZN, Microsoft $MSFT, Alphabet $GOOGL, and Meta $META, monetize this infrastructure through AI cloud services that are driving their own revenue growth at double-digit rates.

The critical point for investors is that this capex cycle shows no signs of slowing. Management teams at all four hyperscalers have explicitly stated on earnings calls that AI demand continues to outpace their capacity to build infrastructure. Amazon $AMZN CEO Andy Jassy has described AI as a once-in-a-lifetime opportunity. Alphabet $GOOGL CEO Sundar Pichai has committed to making Google the most AI-forward company in the world. Meta $META CEO Mark Zuckerberg has called AI the company's top investment priority. Microsoft $MSFT CEO Satya Nadella has positioned Azure as the default cloud for AI workloads. When the CEOs of the four most valuable companies in the world are all saying the same thing, investors should pay attention. The capex cycle is not a bubble. It is an infrastructure buildout that will define the next decade of technology.

AI, Quantum, and the Next Frontier

While artificial intelligence dominates the current earnings narrative, quantum computing is emerging as the next major technology theme that investors need to monitor. The U.S. government has committed approximately $2 billion to quantum computing research and development, and the pace of breakthroughs is accelerating. Google's Willow quantum processor demonstrated error correction capabilities that were previously thought to be years away. IonQ has seen its stock advance 41% in 2026, with analysts setting an average price target of $70.83, representing a forecasted upside of over 42%. IBM $INTC has also surged on quantum computing news, leveraging its decades of quantum research to position itself as a credible player in the emerging quantum ecosystem.

The quantum computing landscape is distinct from AI in several important ways. First, it is earlier in the commercialization cycle. While AI is generating hundreds of billions of dollars in revenue today, quantum computing is still primarily a research and development investment. Companies like IonQ, Rigetti Computing, and D-Wave Quantum are generating minimal revenue and are not yet profitable. However, the strategic importance of quantum computing, particularly for cryptography, drug discovery, and materials science, means that government and corporate investment will continue to flow regardless of near-term profitability. The $2 billion U.S. government commitment signals that quantum is being treated as a matter of national security, not just a commercial opportunity.

Company / Entity | Quantum Focus | 2026 Status |

|---|---|---|

Google $GOOGL | Willow quantum processor, error correction | Major breakthrough demonstrated; commercialization timeline 2028-2030 |

IBM | Quantum chips and systems, quantum cloud | Decades of R&D; stock surged on quantum news |

IonQ | Trapped-ion quantum computers | Stock up 41% in 2026; avg price target $70.83 |

Rigetti Computing | Superconducting quantum processors | Pre-revenue; government contracts |

D-Wave Quantum | Quantum annealing systems | Niche commercial applications; pre-profitability |

Microsoft $MSFT | Topological qubits, Azure Quantum | Long-term bet; quantum cloud platform |

U.S. Government | Quantum R&D funding | $2 billion committed |

Table 6: Quantum computing landscape as of mid-2026. Sources: BlueQubit, TECHi, analyst reports.

Defense and Industrial Earnings: The AI Premium

The intersection of AI and defense is creating a new earnings dynamic for traditional industrial companies. Lockheed Martin $LMT, RTX $RTX, Northrop Grumman $NOC, and Boeing $BA are all reporting increasing AI content in their defense contracts, and this is beginning to show up in their financial results. The Pentagon's $13.4 billion AI and autonomy request for FY2026, the $185 billion Golden Dome program, and the $9 billion intelligence community chip authorization are flowing through the defense supply chain and creating incremental revenue and margin opportunities for companies willing to adapt.

Palantir $PLTR, as profiled extensively in prior Live Trading News coverage, is the purest play on defense AI, with cumulative DOD deal values exceeding $10 billion and revenue growing 54% year-over-year. But the traditional primes are not standing still. Lockheed Martin $LMT won a $514.4 million AI-related contract and is integrating AI into its F-35, missile defense, and space systems. RTX $RTX is a subcontractor on the $185 billion Golden Dome program, providing missile interceptors and sensor systems enhanced with AI. Northrop Grumman $NOC is building the space sensors and advanced electronics that form the eyes of next-generation defense systems. Even Boeing $BA, which has faced well-documented challenges in its commercial aviation business, is seeing increased AI demand in its defense, space, and autonomous systems divisions. Tesla $TSLA, while not a traditional defense contractor, is positioning its Optimus humanoid robot and autonomous driving technology as dual-use platforms with military applications.

The Semiconductor Earnings Chain

The semiconductor earnings chain is where the AI supercycle is most visible in the numbers. Nvidia $NVDA reports 56% revenue growth, but the companies that supply Nvidia and the hyperscalers are also posting extraordinary results. ASML $ASML, the Dutch monopoly supplier of extreme ultraviolet lithography machines, continues to see record bookings as TSMC, Samsung, and Intel expand advanced chip fabrication capacity to meet AI demand. Applied Materials $AMAT, Lam Research $LRCX, and KLA $KLAC, which provide the process equipment and inspection tools used in semiconductor manufacturing, are all reporting order books that extend well into 2027.

Micron $MU is experiencing a particularly powerful earnings tailwind from AI. High-bandwidth memory, or HBM, is essential for AI training workloads, and Micron $MU is one of only three companies in the world capable of producing it. The company has reported that HBM demand is exceeding its production capacity, and it has committed billions in capital expenditure to expand output. AMD $AMD, meanwhile, is leveraging its position as the primary alternative to Nvidia in AI accelerators, with its MI400 series gaining traction among hyperscalers looking for supply diversification. Intel $INTC remains the most challenged of the major semiconductor companies, struggling to compete in AI while simultaneously executing a foundry turnaround, but even Intel is benefiting from the broader increase in semiconductor demand driven by AI infrastructure buildout.

Company | Role in AI Value Chain | Earnings Catalyst |

|---|---|---|

Nvidia $NVDA | AI GPU design (80%+ market share) | Blackwell ramp, data center revenue growth |

ASML $ASML | EUV lithography (monopoly) | Advanced fab capacity expansion bookings |

Applied Materials $AMAT | Semiconductor process equipment | AI-driven fab tool demand |

Lam Research $LRCX | Etch and deposition equipment | Memory and logic chip expansion |

KLA $KLAC | Process control and inspection | Yield optimization for advanced nodes |

Micron $MU | High-bandwidth memory (HBM) | HBM supply constraint, pricing power |

AMD $AMD | Alternative AI accelerators (MI series) | MI400 adoption by hyperscalers |

Intel $INTC | Edge computing, foundry services | Foundry turnaround, Gaudi accelerator progress |

Table 7: Semiconductor earnings chain and Q2 2026 catalysts. Sources: company filings, analyst estimates.

It Is Still Very Early in the AI Cycle

Here is the most important insight for investors heading into this earnings season and beyond: despite the extraordinary numbers about to be reported, despite the $750 billion in hyperscaler capital expenditure, despite the 56% revenue growth at Nvidia and the 86% EBITDA growth at SpaceX's Starlink, we are still in the very early innings of the artificial intelligence revolution. The infrastructure being built today, the data centers, the chips, the satellite networks, the defense systems, this is the foundation upon which the next decade of AI applications will be built. The consumer-facing AI products that will transform daily life for billions of people are still in development. The enterprise AI deployments that will redefine every industry from healthcare to finance to manufacturing are still in pilot phases. The autonomous systems that will change warfare, transportation, and logistics are still in testing.

To put this in perspective, consider the internet in 1998. The browser had been invented, the infrastructure was being built, and a handful of companies were posting extraordinary growth rates. But Google had not yet gone public. Social media did not exist. Cloud computing was a research project. The applications that would ultimately generate trillions of dollars in value were still years away. Artificial intelligence in 2026 is in a similar position. The foundation is being laid, the enabling technologies are being deployed, and the companies building the infrastructure are being richly rewarded. But the transformative applications, the ones that will touch every human being on the planet, have not yet arrived. When they do, the current earnings numbers will look small by comparison.

“People look at Nvidia's $46 billion quarter or the hyperscalers' $750 billion capex and they think the AI trade is priced in. It is not. We are still laying the pipes. The applications that will drive the next hundred trillion dollars of value have not been invented yet. We are in the first quarter of a game that will last decades.”

— Shayne Heffernan, CEO KXCO

This perspective is critical for how investors should approach this earnings season and the quarters that follow. Beating earnings estimates by a few cents per share is not the story. The story is the trajectory of capital expenditure, the rate of AI adoption, and the compounding network effects that are being created by the companies at the center of the AI ecosystem. Nvidia $NVDA is not a chip company. It is the central nervous system of the global AI infrastructure. Amazon $AMZN, Microsoft $MSFT, Alphabet $GOOGL, and Meta $META are not just cloud providers. They are the platforms upon which the next generation of software will be built. SpaceX $SPCX is not just a rocket company. It is the communications and defense infrastructure company of the future.

Earnings Season Playbook: What to Watch

Stock / Ticker | Earnings Focus | What to Watch For |

|---|---|---|

Nvidia $NVDA | Data center revenue, Blackwell ramp | Sequential growth rate, guidance, China H20 commentary |

SpaceX $SPCX | First public earnings (post-IPO) | Starlink subscriber growth, EBITDA, Golden Dome progress |

Amazon $AMZN | AWS growth, capex plans | AI services revenue, custom chip progress, operating margins |

Microsoft $MSFT | Azure AI growth, Copilot monetization | AI revenue contribution, capex sustainability |

Alphabet $GOOGL | Google Cloud, Search AI | AI overviews monetization, TPU economics |

Meta $META | AI infrastructure ROI, ad AI | Llama adoption, Reality Labs trajectory, capex efficiency |

Palantir $PLTR | Commercial vs. government revenue | U.S. commercial growth, new contract wins |

Tesla $TSLA | AI/robotics, autonomous driving | Optimus milestones, FSD regulatory progress |

AMD $AMD | MI400 adoption, data center share | Hyperscaler win rate, margin expansion |

Micron $MU | HBM revenue and pricing | Supply/demand dynamics, HBM mix expansion |

ASML $ASML | Bookings and backlog | China exposure, next-gen EUV timeline |

Applied Materials $AMAT | Order book and revenue | AI-driven tool demand, China headwinds |

Lam Research $LRCX | Deposition/etch orders | Memory capex cycle, HBM equipment demand |

KLA $KLAC | Inspection tool demand | Advanced node yield, AI chip qualification |

Lockheed Martin $LMT | AI contract wins | F-35 AI upgrades, Golden Dome subcontract value |

RTX $RTX | Defense AI integration | Missile defense AI, sensor orders |

Northrop Grumman $NOC | Space and electronics | AI sensor orders, classified programs |

Boeing $BA | Defense AI, recovery | Commercial delivery recovery, autonomous systems |

Intel $INTC | Foundry progress, AI accelerators | 18A process yield, Gaudi order book |

Table 8: Q2 2026 earnings season playbook for AI and adjacent stocks. Sources: analyst consensus, company guidance.

Conclusion: The Setup for a Generational Earnings Cycle

This earnings season is not just another quarterly reporting period. It is the first full earnings cycle in which the AI supercycle is visible in the numbers across the entire value chain, from the semiconductor equipment makers like ASML $ASML, Applied Materials $AMAT, Lam Research $LRCX, and KLA $KLAC, through the chip designers like Nvidia $NVDA, AMD $AMD, and Intel $INTC, to the hyperscalers like Amazon $AMZN, Microsoft $MSFT, Alphabet $GOOGL, and Meta $META, to the defense primes like Lockheed Martin $LMT, RTX $RTX, and Northrop Grumman $NOC, to the new entrants like SpaceX $SPCX and Tesla $TSLA. The breadth of AI-driven earnings growth is unprecedented, and it is occurring during a period of macroeconomic stability that provides a favorable backdrop for risk assets.

The two big winners of this earnings season, Nvidia $NVDA and SpaceX $SPCX, represent the two sides of the AI investment thesis. Nvidia is the pure infrastructure play, the company that builds the compute foundation upon which all AI applications depend. SpaceX is the platform play, the company that combines satellite communications, space launch, and defense into an infrastructure business with no comparable competitor. Together, they illustrate the scale of the opportunity and the diversity of ways to participate in it. But the broader message is even more important: this is still the beginning. The AI supercycle has years, possibly decades, to run. The companies reporting earnings this season are building the foundation for the most significant technological transformation in human history. The smart money is not asking whether AI is overhyped. The smart money is asking whether it is underhyped.

For a structured mapping of the entire AI sector, including company relationships, investment flows, and technology classifications, visit the KXCO AI Ontology at https://kxco.ai/ontology-live/.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. The author may hold positions in securities mentioned. All data sourced from public reporting and analyst consensus estimates. Visit https://kxco.ai/ontology-live/ for the KXCO AI Ontology.

AI Stocks Are War Stocks

The Pentagon is pouring $13.4 billion into AI this year, and a new generation of tech-native defense companies — Palantir, Anduril, SpaceX — are capturing the lion's share of the fastest-growing military spending category in history.

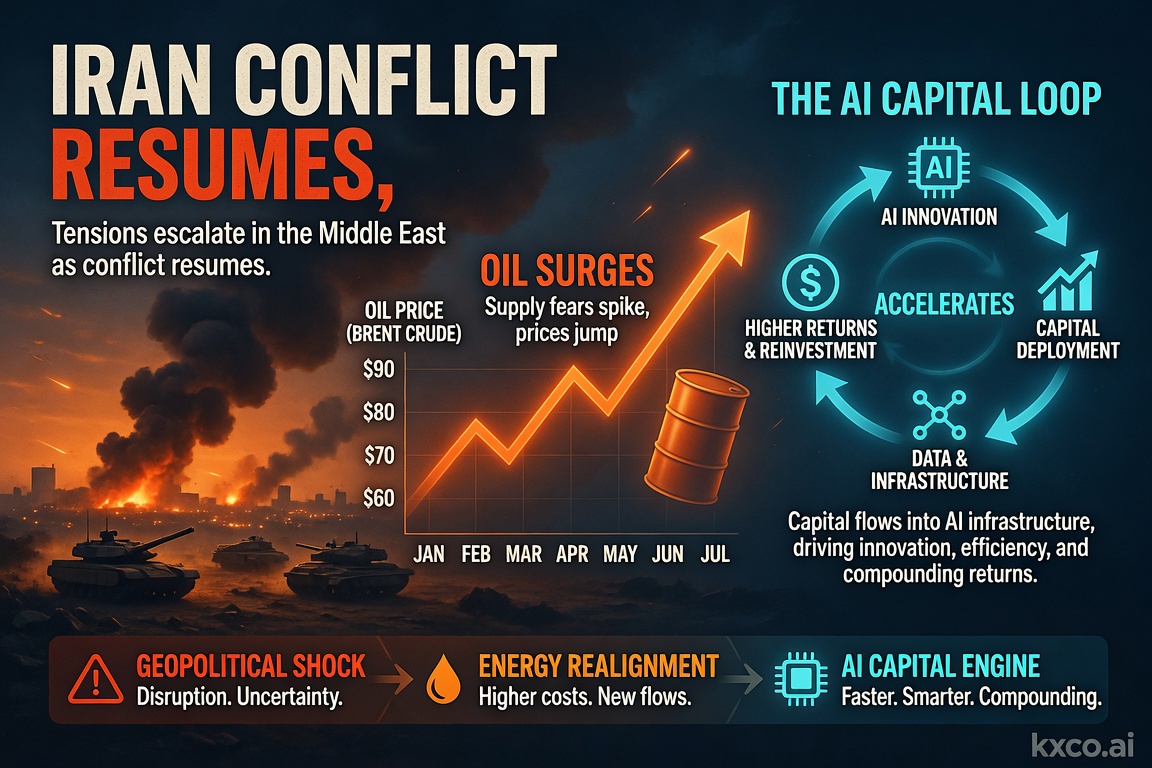

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

Who Is Who in the AI Space: The Definitive Guide to AI Stocks in 2026

The definitive 2026 guide to AI stocks: $NVDA, $GOOGL, $MSFT, $AMZN, $META, $TSM, $AVGO, $ORCL and $PLTR in the US; $BABA, $TCEHY and $BIDU in China — each mapped to its layer of the AI value chain, with cashtags, market caps and the investment thesis for each.

AI and Quantum Computing Latest News

AI and quantum computing are converging into a single US-China contest. A fact-checked, investor-focused map of the model gap, the quantum milestones, the security imperative, and the stocks positioned across both — NVDA, GOOGL, MSFT, IBM, IONQ, TSM. By Shayne Heffernan.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.