AI Stocks Are War Stocks

$PLTR, $NVDA, $AMZN, $MSFT, $GOOGL, $META, $LMT, $RTX, $NOC, $AMAT, $ASML, $MU, $LRCX, $KLAC, $AMD

Part of theAI Stocks Center

AI Stocks Are War Stocks

Inside the $13.4 Billion Pentagon AI Buildout and the Companies Profiting From It

Live Trading News

July 13, 2026

"Never think that war, no matter how necessary nor how justified, is not a crime. Ask the infantry and ask the dead."

— Ernest Hemingway

There is a new kind of war stock in town. It does not manufacture bullets, hulls, or jet engines. It builds neural networks, trains large language models, and deploys autonomous decision-making systems that can identify threats, track targets, and compress the kill chain from hours to seconds. Artificial intelligence has become the single most important line item in the United States defense budget, and the companies supplying that capability are reaping rewards that dwarf anything the traditional defense industrial base has ever seen. The era of AI stocks as war stocks has arrived, and the scale of capital flowing into this sector is staggering.

The numbers tell the story plainly. The Department of Defense requested $13.4 billion for AI and autonomy programs in fiscal year 2026, representing the largest single-year AI investment in American military history. The broader DOD IT budget for FY2026 stands at $66 billion, with AI as the top priority across every branch of the armed services. Federal AI spending across all agencies has surged from $1.75 trillion in 2025 to an estimated $2.52 trillion in 2026. The value of DOD funds obligated for AI leapt to $7.2 billion in 2026, an increase of 966% from 2024 levels according to Brookings Institution analysis. These are not incremental budget adjustments. This is a structural realignment of how the United States projects power, and the publicly traded companies positioned to capture this spending are experiencing revenue growth that the legacy defense primes can only watch from the sidelines.

The Department of Defense did not arrive at its current AI posture by accident. Years of strategic planning, operational failures in traditional warfare, and the demonstrated success of commercial AI systems converged to produce a consensus at the highest levels of the Pentagon: the future of military advantage belongs to whoever masters artificial intelligence first. The January 2026 publication of the Artificial Intelligence Strategy for the Department of War made this official doctrine, declaring that AI-enabled warfare and AI-enabled capability development would redefine the character of military affairs over the coming decade.

The scale of financial commitment underpinning this doctrine is without precedent. The $13.4 billion requested for AI and autonomy in FY2026 dwarfs the combined AI budgets of the next ten military spenders globally. The DOD's $66 billion IT budget pivots hard toward AI and efficiency, with the Army alone requesting $16.7 billion for IT, even as its overall request declined slightly. The message is clear: every dollar that can be redirected from legacy systems toward AI-enabled capabilities is being redirected. Cyber Command created an entirely new AI program in its FY2026 budget, allocating $5 million for rapid 90-day pilot cycles of AI technologies for offensive and defensive cyber operations. The Replicator initiative, the Pentagon's signature autonomous systems program, received approximately $1 billion in FY2024-2025 appropriations and continues into FY2026 with expanded scope covering one-way attack drones, autonomous maritime vehicles, counter-drone systems, and supporting AI software.

FACT SET: Pentagon AI Budget Snapshot (FY2026) | |

Total DOD AI & Autonomy Request | $13.4 billion |

Total DOD IT Budget | $66 billion |

DOD AI Obligations (FY2026) | $7.2 billion (up 966% from FY2024) |

Replicator Initiative (FY2024-2025) | ~$1 billion |

Army IT Budget | $16.7 billion |

Cyber Command New AI Program | $5 million (90-day agile pilots) |

Total US Federal AI Spending (FY2026) | $2.52 trillion (up from $1.75T in FY2025) |

Table 1: Key Pentagon AI budget figures for fiscal year 2026, compiled from Brookings Institution, Washington Technology, and USAspending.gov data.

The intelligence community is matching the Pentagon's urgency, if not its public transparency. The White House approved a secret $9 billion request in 2026 to acquire cutting-edge computer chips for America's spy agencies, enabling them to tap into the full capabilities of the latest artificial intelligence systems. The National Security Agency uses AI to identify hackers attempting to breach U.S. critical infrastructure and to seek out AI-enabled threats. The Central Intelligence Agency leverages AI for content triage, translation, and transcription to help analysts process vast volumes of intercepted information. The National Reconnaissance Office, which operates America's intelligence satellites and holds by far the largest budget of any intelligence agency, is integrating AI into satellite imagery analysis and real-time threat detection. Across all eighteen elements of the intelligence community, AI adoption is described by officials as both wary and urgent, driven by the recognition that exponential data growth will smother analysts who do not have machine assistance.

The Neo-Primes: Palantir, Anduril, and SpaceX

The traditional defense industrial base, the so-called prime contractors like Lockheed Martin, RTX (formerly Raytheon), Northrop Grumman, and Boeing, built their dominance on traditional platforms and long-term procurement deals that spanned decades. That dominance is now being challenged by a new generation of technology-native defense companies that move at software speed and bring capabilities the old primes cannot match. These companies, led by Palantir Technologies, Anduril Industries, and SpaceX, have been collectively dubbed the neo-primes, and their market valuations and contract wins tell a story of a power shift in the defense sector that is accelerating with every quarter.

Palantir Technologies has emerged as the single most important software company in the American defense establishment. The company's revenue surged 54% year-over-year in 2025, making it the most profitable year in Palantir's history since it began doing business with the military. The Army awarded Palantir a $618.9 million contract for its Titan ground station system, and the company's cumulative deal value with the DOD now exceeds $10 billion. Palantir software helps enable the U.S. Army to leverage AI insights to make quick decisions across multiple domains, from logistics to intelligence fusion to fires coordination. But Palantir's most consequential role is its position as co-developer, alongside Anduril Industries, of the software backbone for the Golden Dome missile defense system.

The Golden Dome project is a $185 billion missile defense initiative ordered by President Trump to build a space-based shield capable of intercepting ballistic, cruise, and hypersonic missiles. Anduril and Palantir are providing not only software but the artificial intelligence solutions to accelerate command and control and compress engagement times. They are joined by Scale AI, which provides the data labeling and AI training infrastructure, networking firm Aalyria for communications, and Swoop Technologies. SpaceX has won a $6.45 billion contract to build the space layer of Golden Dome, including space-based sensors and a satellite data network backbone. The consortium bid, which also includes OpenAI, represents a fundamental shift in how major defense programs are structured: led by software and AI companies rather than traditional hardware manufacturers.

FACT SET: Golden Dome Consortium | |

Program Value | $185 billion |

Capability | Space-based missile defense (ballistic, cruise, hypersonic) |

Software Leads | Anduril Industries, Palantir Technologies |

Space Layer | SpaceX ($6.45B contract for SB-AMTI and SDN Backbone) |

Data & AI Infrastructure | Scale AI |

Communications | Aalyria |

Other Partners | Saronic, OpenAI, Swoop Technologies |

Table 2: Golden Dome missile defense program structure and key contractors. Source: Reuters, Wall Street Journal, AeroMorning.

Anduril Industries, founded by Palmer Luckey, has positioned itself as the hardware complement to Palantir's software dominance. The company builds autonomous drones, counter-drone systems, and surveillance towers that integrate directly with Palantir's AI-powered command-and-control platform. Anduril received a $99.6 million contract alongside Palantir to develop the AI-based Next Generation Command and Control (NGC2) platform, which is being tested across multiple military services. The Brennan Center for Justice noted that 2025 was the most profitable year for both Palantir and Anduril since they began working with the military, a testament to the speed at which DOD procurement is shifting toward commercially proven AI capabilities.

SpaceX, while not traditionally classified as a defense AI company, has become indispensable to the military AI architecture. Its Starlink satellite constellation provides the communications backbone for autonomous systems operating in denied environments. The $6.45 billion Golden Dome space layer contract cements SpaceX's role as a primary defense contractor, and the company's $1.25 trillion pre-IPO valuation makes it more valuable than Lockheed Martin, RTX, and Northrop Grumman individually. The consortium bid structure, where SpaceX, Palantir, Anduril, and OpenAI jointly bid for military programs, represents a direct challenge to the incumbent prime contractor model that has governed Pentagon procurement for generations.

The AI Foundation: OpenAI, Scale AI, and the Model Builders

The military AI value chain begins not with hardware or platforms but with the fundamental AI models and data infrastructure that make everything downstream possible. OpenAI, the company behind ChatGPT and GPT-4, reversed its longstanding prohibition on military contracts and signed a deal with the Department of War in 2026, outlining safety red lines and legal protections for how AI systems would be deployed in classified military environments. OpenAI won a $200 million contract to develop artificial intelligence for the Army, marking the first time a large language model company has been directly contracted for operational military AI development. The Pentagon also announced agreements with OpenAI, Alphabet, Nvidia, SpaceX, and Microsoft as part of a broader partnership framework to bring commercial AI capabilities into the defense ecosystem.

Scale AI, which is 49% owned by Meta, has become the data backbone of military AI operations. The Pentagon's Chief Digital and Artificial Intelligence Office (CDAO) expanded its enterprise agreement with Scale from $100 million to $500 million, a five-fold increase that gives any component of the Department of War streamlined access to Scale's data labeling, AI evaluation, and model fine-tuning platform. The deal, reported by Bloomberg and Forbes, represents one of the largest single AI contracts awarded by the U.S. government and underscores the critical importance of high-quality training data to military AI systems. Scale provides the infrastructure that allows the DOD to take commercial AI models and adapt them for classified military applications, a process that requires massive amounts of curated, domain-specific data.

Major Military AI Contracts: A Comparative Overview

Company | Contract / Program | Value | Role |

|---|---|---|---|

Palantir ($PLTR) | Army Titan / DOD cumulative | $10B+ | AI-powered C2, intelligence fusion, Golden Dome software |

Scale AI | CDAO Enterprise Agreement | $500M | Data labeling, AI training, model evaluation |

SpaceX | Golden Dome Space Layer | $6.45B | Satellite sensors, SB-AMTI, SDN backbone |

OpenAI | Army AI Development | $200M | Large language models for military applications |

Anduril | NGC2 Platform / Golden Dome | $99.6M+ | Autonomous systems, counter-drone, C2 software |

Lockheed Martin ($LMT) | Various AI programs | $514.4M+ | Traditional platforms with AI integration |

RTX ($RTX) | Golden Dome subcontractor | TBD (part of $185B) | Missile interceptors, sensors |

Northrop Grumman ($NOC) | Golden Dome subcontractor | TBD (part of $185B) | Space sensors, advanced electronics |

Table 3: Major military AI contracts and programs as of mid-2026. Sources: company filings, Bloomberg, Reuters, Forbes, DefenseScoop.

The AI Value Chain: From Silicon to Warfare

Understanding which companies will profit from the military AI buildup requires understanding the full value chain, from the silicon wafers that power AI computations to the cloud platforms that deliver AI services to warfighters in the field. The KXCO AI Ontology, available at https://kxco.ai/ontology-live/, maps this entire ecosystem with structured relationships between companies, technologies, and investment flows. The ontology reveals that military AI spending does not flow linearly but cascades through multiple layers of the technology stack, creating investment opportunities at every tier.

At the foundation of the AI value chain sits semiconductor design and fabrication. Nvidia dominates the market for AI training and inference chips, with its H100 and successor Blackwell GPUs serving as the computational backbone for virtually every military AI system in development. Nvidia's GPUs are manufactured by TSMC in Taiwan, creating a single point of failure that the Pentagon has identified as a critical strategic vulnerability. Amazon, Alphabet, and Microsoft are all accelerating custom AI chip programs in 2026 while still purchasing enormous volumes of Nvidia GPUs for their cloud infrastructure. AMD provides the primary competitive alternative to Nvidia for AI compute, while Intel, despite its struggles in the AI chip market, remains a significant supplier of processors for edge computing and legacy military systems.

The fabrication layer is dominated by TSMC, which manufactures approximately 90% of the world's most advanced semiconductors. ASML, a Dutch company, holds a monopoly on the extreme ultraviolet lithography machines required to print the smallest transistor features. Applied Materials, Lam Research, and KLA Corporation provide the process equipment and inspection tools that make advanced fabrication possible. Memory suppliers including Micron, SK Hynix, and Samsung produce the high-bandwidth memory essential for AI training workloads. The intelligence community's $9 billion chip acquisition request underscores how critical this foundation layer has become to national security.

Moving up the stack, the cloud infrastructure layer is controlled by Amazon Web Services, Microsoft Azure, and Google Cloud. All three have secured major defense cloud contracts and are building specialized environments for classified AI workloads. These hyperscalers provide the computational environments where military AI models are trained, tested, and deployed. Microsoft's partnership with OpenAI gives it a unique advantage, as many of the same models being adapted for military use are trained on Azure infrastructure. Amazon's custom Trainium and Inferentia chips represent an attempt to reduce dependence on Nvidia while capturing more of the AI compute value chain internally. Google's Tensor Processing Units power the company's own AI services and are being evaluated for classified defense applications.

Value Chain Tier | Key Companies | Military AI Role |

|---|---|---|

Chip Design | GPU/AI accelerator design for training and inference | |

Chip Fabrication | TSMC, Samsung | Manufacturing advanced AI semiconductors |

Lithography Equipment | ASML ($ASML) | EUV lithography machines (monopoly position) |

Process Equipment | Applied Materials ($AMAT), Lam Research ($LRCX), KLA ($KLAC) | Semiconductor manufacturing tools |

Memory | Micron ($MU), SK Hynix, Samsung | High-bandwidth memory for AI workloads |

Cloud Infrastructure | Classified AI training and deployment environments | |

AI Model Development | Foundation models adapted for military applications | |

Data Infrastructure | Scale AI, Palantir ($PLTR) | Data labeling, ontology, model fine-tuning |

Defense Platforms | Anduril, Lockheed Martin ($LMT), RTX ($RTX), Northrop Grumman ($NOC) | Autonomous systems, C2, missile defense |

Space & Comms | SpaceX, Aalyria | Satellite constellations, communications backbone |

Table 4: The AI value chain for military applications, mapped using the KXCO AI Ontology framework. Visit https://kxco.ai/ontology-live/ for the full interactive ontology.

The Winners in the Military AI Race

The companies best positioned to capture the military AI spending boom share several characteristics. First, they have commercially proven AI products that can be adapted for defense applications at relatively low marginal cost. Palantir's Gotham and Foundry platforms were battle-tested in the commercial sector before being deployed with the military. Scale AI's data labeling platform was built to serve commercial AI companies before being contracted by the Pentagon. This commercial-to-defense pipeline allows companies to amortize research and development costs across a much larger revenue base than pure defense contractors can access.

Second, the winners are moving at software speed. Traditional defense procurement cycles span five to ten years from concept to deployment. The neo-primes are delivering capabilities in months. Scale AI's $500 million contract expansion happened in less than a year. The Golden Dome consortium was formed and won contracts within months of the program's announcement. OpenAI's military AI deal came together in weeks after the company reversed its military prohibition. This velocity is fundamentally changing the competitive dynamics of the defense market, because the Pentagon's most urgent requirements, from counter-drone systems to real-time intelligence analysis, demand solutions that can be fielded quickly.

Third, the biggest winners are building platform businesses, not point solutions. Palantir is not selling a single AI tool; it is building the operating system for military decision-making. Scale AI is not labeling data for one project; it is providing the enterprise data infrastructure for the entire Department of War. SpaceX is not launching one satellite; it is building the communications backbone for the entire military AI architecture. These platform positions create switching costs and network effects that compound over time, making it increasingly difficult for competitors to dislodge the incumbents.

The Cashtags to Watch: $PLTR (Palantir), $NVDA (Nvidia), $AMZN (Amazon), $MSFT (Microsoft), $GOOGL (Alphabet), $META (Meta/Scale AI backer), $LMT (Lockheed Martin), $RTX (Raytheon Technologies), $NOC (Northrop Grumman), $AMAT (Applied Materials), $ASML (ASML Holding), $MU (Micron), $LRCX (Lam Research), $KLAC (KLA Corporation), $AMD (Advanced Micro Devices).

The Intelligence Community's AI Buildup

While the Pentagon captures the headlines, the intelligence community's AI spending is equally transformative, if less visible. The CIA, NSA, NRO, and the other fifteen elements of the U.S. Intelligence Community are facing a data deluge that threatens to overwhelm human analysts. The volume of signals intelligence, satellite imagery, open-source intelligence, and human intelligence being collected every day exceeds the processing capacity of the entire analyst workforce by orders of magnitude. AI is not a luxury for the intelligence community; it is a survival necessity.

The $9 billion White House authorization for spy agency AI chip acquisition represents the largest single intelligence technology investment in recent history. The NSA is using AI to identify hackers targeting U.S. critical infrastructure and to detect AI-enabled cyber threats that traditional signature-based systems cannot catch. The CIA has deployed AI systems for content triage, rapidly screening millions of intercepted communications to prioritize the most actionable intelligence for human analysts. The NRO is integrating AI into its satellite imagery analysis pipeline, enabling real-time identification of military movements, weapons deployments, and infrastructure changes that would take human analysts weeks to detect. PBS reported that U.S. intelligence agencies' embrace of generative AI is characterized by a tension between wariness about the technology's limitations and urgency about the consequences of falling behind adversaries in AI capability.

FACT SET: Intelligence Community AI Programs | |

White House AI Chip Authorization | $9 billion (classified details) |

NSA AI Use Cases | Hackers targeting critical infrastructure, AI-enabled threat detection |

CIA AI Use Cases | Content triage, translation, transcription, analyst prioritization |

NRO Focus Area | AI-powered satellite imagery analysis, real-time threat detection |

IC-Wide Challenge | Exponential data growth overwhelming human analyst capacity |

Number of IC Elements | 18 agencies and offices |

Table 5: U.S. Intelligence Community AI programs and spending. Sources: New York Times, CSIS, PBS, Aspen Institute.

The Hemingway Warning and the AI Crossroads

Ernest Hemingway wrote that war, no matter how necessary nor how justified, is not a crime. His words carry a particular weight in the age of AI-enabled warfare, where the distance between a human decision and a lethal outcome is being compressed by algorithms that operate at machine speed. The Pentagon's AI strategy explicitly envisions autonomous systems making engagement decisions in compressed timeframes where human oversight is advisory rather than directive. The Replicator initiative, which aims to field thousands of autonomous drones capable of identifying and engaging targets, raises fundamental questions about accountability, proportionality, and the moral weight of delegating kill decisions to machines.

The companies building these systems are aware of these concerns, at least publicly. OpenAI's contract with the Department of War includes safety red lines and legal protections. Palantir emphasizes that its systems provide decision support rather than making autonomous engagement decisions. Anduril positions its autonomous systems as defensive in nature, designed to protect rather than attack. But the trajectory of the technology is clear: as AI systems become more capable and the perceived threat environment becomes more acute, the pressure to delegate greater autonomy to machines will intensify. The $13.4 billion in AI spending, the $185 billion Golden Dome program, the $9 billion intelligence chip authorization, these are not investments in theoretical capabilities. They are investments in systems that will be deployed, tested in conflict, and refined based on operational experience.

"The public are yet to see the wonder, the magic or the horror of AI. What we are witnessing now is merely the infrastructure being built, the pipes being laid. When the full force of artificial intelligence is directed at both creation and destruction, and the public finally sees what it can do, the conversation will change forever."

— Shayne Heffernan, CEO KXCO

Investment Implications: Reading the AI War Trade

For investors seeking exposure to the military AI theme, the KXCO AI Ontology at https://kxco.ai/ontology-live/ provides a structured framework for understanding the relationships between companies, technologies, and capital flows across the entire AI sector. The ontology maps not only the publicly listed companies profiled in this article but also the private companies, government agencies, and research institutions that form the broader AI ecosystem. It is an essential tool for anyone looking to navigate the complexity of AI investment with precision.

The military AI trade is not a single bet. It is a value chain play that spans semiconductors, cloud infrastructure, data platforms, model developers, and defense primes. Nvidia remains the purest exposure at the chip design layer, with its GPUs serving as the foundational compute platform for virtually every military AI system. Palantir offers the most direct exposure to defense AI software and platform economics. Amazon, Microsoft, and Alphabet provide cloud infrastructure leverage with diversified revenue streams that include significant commercial AI demand. Lockheed Martin, RTX, and Northrop Grumman offer traditional defense exposure with increasing AI content. Scale AI, while privately held and 49% owned by Meta, represents the data infrastructure layer and may eventually offer a public investment opportunity.

The risk factors are substantial. Geopolitical escalation could accelerate spending or disrupt supply chains. Semiconductor concentration in Taiwan represents a single point of failure for the entire AI value chain. Regulatory changes could constrain the autonomy of AI-powered weapons systems. Ethical controversies could slow adoption or create reputational risks for publicly traded companies. And the pace of technological change means that today's dominant companies may be disrupted by new entrants with superior capabilities. But for investors with a multi-year time horizon and tolerance for volatility, the military AI sector represents one of the most compelling structural growth themes in the global equity markets today.

Conclusion: The Industrialization of AI Warfare

The transformation of AI stocks into war stocks is not a metaphor. It is a financial and strategic reality driven by billions of dollars in government spending, accelerating procurement cycles, and the demonstrated superiority of AI-enabled systems over legacy military technologies. The companies profiled in this article, from the chip designers at Nvidia to the platform builders at Palantir, from the data infrastructure providers at Scale AI to the space layer architects at SpaceX, are not merely participating in a defense spending cycle. They are building the infrastructure of a new kind of warfare, one in which the speed of decision-making, the quality of intelligence fusion, and the autonomy of weapons systems will determine outcomes on the battlefield.

The KXCO AI Ontology tracks these relationships in real time, providing investors, analysts, and policymakers with a structured, machine-readable map of the AI sector at https://kxco.ai/ontology-live/. As the Pentagon's AI spending continues to scale, as the intelligence community's chip acquisitions come online, and as programs like Golden Dome and Replicator move from concept to deployment, the companies that have positioned themselves at the intersection of commercial AI innovation and defense application will continue to generate the kind of revenue growth and market valuation expansion that defines generational investment opportunities. The war for AI dominance is being fought on multiple fronts simultaneously, and the stocks of the companies winning that war are the new war stocks of the twenty-first century.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. The author may hold positions in securities mentioned. All data sourced from public reporting. Visit https://kxco.ai/ontology-live/ for the KXCO AI Ontology.

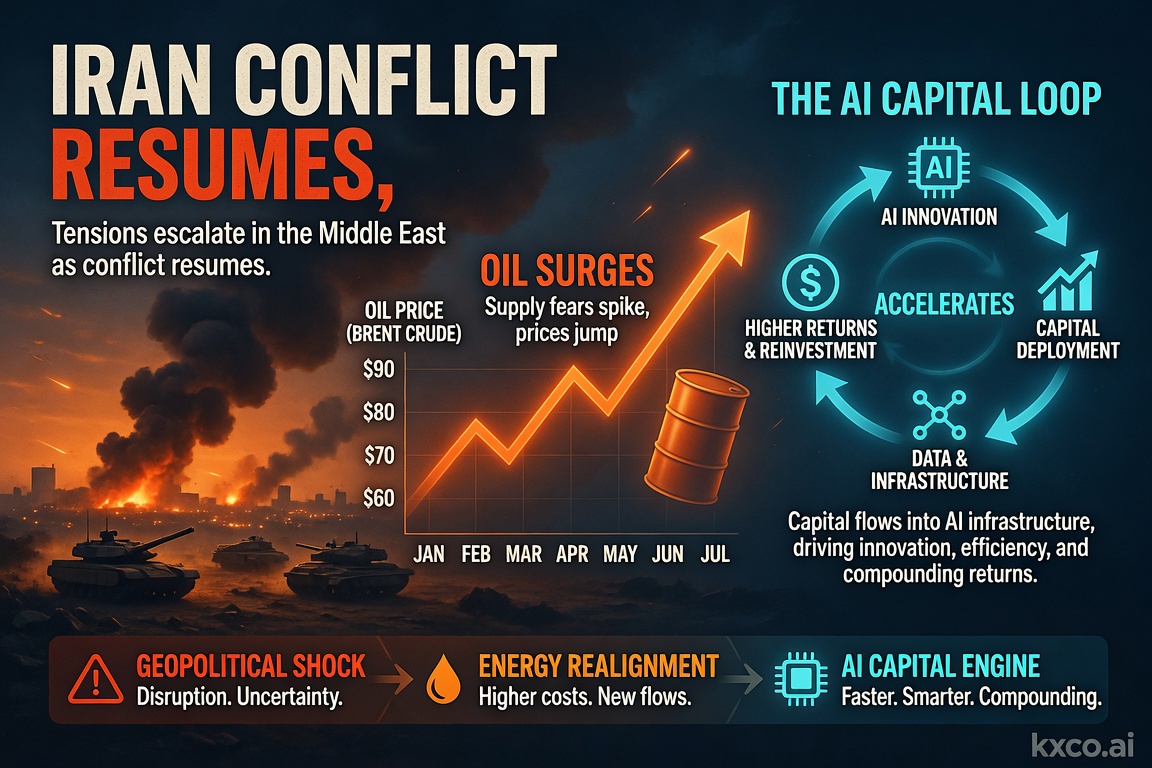

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

Who Is Who in the AI Space: The Definitive Guide to AI Stocks in 2026

The definitive 2026 guide to AI stocks: $NVDA, $GOOGL, $MSFT, $AMZN, $META, $TSM, $AVGO, $ORCL and $PLTR in the US; $BABA, $TCEHY and $BIDU in China — each mapped to its layer of the AI value chain, with cashtags, market caps and the investment thesis for each.

AI and Quantum Computing Latest News

AI and quantum computing are converging into a single US-China contest. A fact-checked, investor-focused map of the model gap, the quantum milestones, the security imperative, and the stocks positioned across both — NVDA, GOOGL, MSFT, IBM, IONQ, TSM. By Shayne Heffernan.

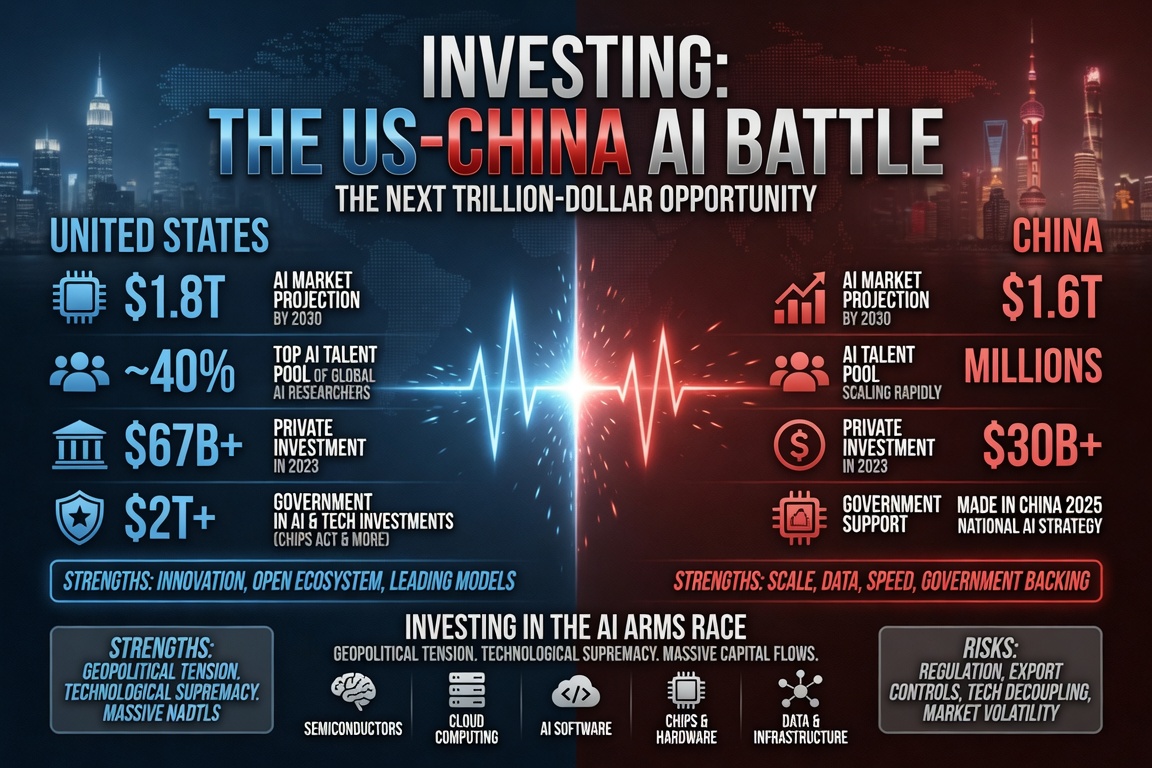

Investing: The US-China AI Battle

US China AI battle investing, decoded: Claude Fable 5 & Opus 4.8 vs GLM-5.2 & Kimi K2.7, the NVIDIA-vs-Huawei chip supply chain, target prices for the best AI stocks to buy in 2026, and a full geopolitical risk matrix. By Shayne Heffernan.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.