AI Stocks to Own Now

The Definitive Guide to the $3 Trillion Buildout $ASML, $TSM $NVDA $AMD $MSFT $AMZN $GOOGL

The AI Stocks: The Definitive Guide to the $3 Trillion Buildout

Follow the Money, Follow the Ontology, Follow the Chips

Shayne Heffernan | Live Trading News | July 2026

The artificial intelligence market in the middle of 2026 is not a speculative bubble. It is the largest infrastructure buildout the global economy has seen since the internet itself, and every major financial institution on Wall Street has revised its forecasts upward in the last six months to reflect a reality that is outpacing even the most aggressive projections. The numbers are staggering, and they deserve to be treated with the gravity they command. This is not a sector play. This is a civilizational shift in how capital is allocated, how compute is distributed, and how value is created across every industry on Earth.

Morgan Stanley Research estimates that nearly $3 trillion of AI-related infrastructure investment will flow through the global economy by 2028, with more than eighty percent of that spending concentrated among a handful of US hyperscalers and the semiconductor companies that supply them. Goldman Sachs has raised its 2026 year-end target for the S&P 500 to 8,000 from 7,600, citing AI-driven earnings growth as the primary catalyst, and projects that AI infrastructure investment will account for roughly half of all S&P 500 earnings growth in 2026. UBS Global Wealth Management has lifted its year-end S&P 500 forecast to 7,900 and now expects global AI capital expenditure to surge to $571 billion in 2026, an eighty-eight percent year-over-year increase from 2024 levels. Bank of America has published a dedicated AI stocks buy list for 2026, arguing that we are at the midpoint of a major overhaul of global computing infrastructure. JP Morgan favors a barbell portfolio approach, splitting allocations between AI leaders and cyclical stocks, and projects AI spending will deliver a second consecutive year of solid capital expenditure gains across the technology sector.

Wall Street AI Forecasts: Mid-2026 Consensus | |

Morgan Stanley | $3T AI infrastructure investment by 2028; $805B hyperscaler capex in 2026 |

Goldman Sachs | S&P 500 year-end target 8,000; AI = ~50% of S&P 500 earnings growth in 2026 |

UBS | Global AI capex $571B in 2026 (88% YoY); S&P 500 target 7,900 |

Bank of America | 2026 is the midpoint of global computing infrastructure overhaul |

JP Morgan | AI spending to deliver second year of solid capex gains; barbell AI + cyclicals |

Table 1: Major bank AI market forecasts, updated Q1–Q2 2026

The implications for investors are clear. This is not a trade. This is a multi-year structural reallocation of capital that will define equity returns for the rest of this decade. The question is not whether AI spending will continue to accelerate, it will, but where the value captures along the supply chain. And that is where the KXCO AI Ontology becomes an indispensable tool for any serious investor trying to navigate this landscape.

The KXCO AI Ontology: Mapping the $973 Billion Supply Chain

The AI sector is complex, interconnected, and riddled with dependencies that are invisible to anyone looking at individual stocks in isolation. That is why we rely on the KXCO AI Ontology, a live, structured map of the entire AI supply chain that tracks 81 entities, 112 claims, and $973 billion in tracked capital flows across seven geopolitical regions. The ontology is not an opinion. It is a verifiable, data-driven map of who depends on whom, where the money flows, and where the systemic risks are concentrated. You can explore it yourself at https://kxco.ai/ontology-live/ — and if you are investing in AI stocks without consulting it, you are flying blind.

KXCO AI Ontology Live: https://kxco.ai/ontology-live/

The ontology reveals, with brutal clarity, that the entire AI sector rests on a chain of dependencies that is far more fragile than most investors appreciate. It identifies five critical chokepoints, twelve structural revelations, and seven geopolitical risk overlays that should inform every allocation decision. The most important insight is this: the AI sector is not a collection of independent companies competing on merit. It is a single, tightly coupled supply chain in which a handful of companies at each layer exercise monopoly or near-monopoly control over the entire stack. Understanding who those companies are, and what they control, is the difference between investing intelligently and gambling.

The Equipment Layer: One Dutch Company Holds the Keys

The KXCO ontology identifies the equipment layer as the true root of the entire AI supply chain. And the root has a name: $ASML. One company, headquartered in Veldhoven, the Netherlands, manufactures the extreme ultraviolet (EUV) lithography machines that every leading-edge AI chip in the world depends on. No ASML, no EUV. No EUV, no advanced semiconductors. No advanced semiconductors, no AI. It is that simple, and it is that concentrated. ASML’s EUV machines cost approximately $400 million each, and the company operates as an effective monopoly, with no competitor capable of producing equivalent equipment. The ontology maps the dependency chain with surgical precision: ASML depends on Zeiss for EUV optics and Trumpf for the laser source, creating a secondary layer of single-point dependencies within the equipment tier itself.

The investment implications are significant. $ASML is not merely a semiconductor equipment company. It is the gatekeeper of the entire AI revolution. Any disruption to ASML’s production, whether from geopolitical pressure, supply chain bottlenecks, or regulatory intervention, would cascade through the entire AI value chain with potentially catastrophic consequences for every company downstream. The ontology rates ASML’s EUV monopoly as a 95% systemic risk factor, the single highest concentration risk in the entire AI sector. Investors who own $NVDA but not $ASML are, in a very real sense, missing the foundational layer of their own thesis.

Company | Ticker | Role in AI Supply Chain | Market Position |

|---|---|---|---|

ASML | EUV lithography machines | 100% monopoly on EUV; ~$400M/machine | |

Zeiss | Private | EUV optics for ASML | Sole supplier of EUV optical systems |

Trumpf | Private | EUV laser source for ASML | Sole supplier of EUV laser sources |

Synopsys | EDA design software | Critical chip design licensing | |

Cadence | EDA design software | Critical chip design licensing |

Table 2: The equipment layer — the foundational chokepoint of the AI supply chain (source: KXCO AI Ontology)

The Foundry Layer: One Island, One Company

If ASML is the root, then TSMC is the trunk. Every leading-edge AI chip designed by Nvidia, AMD, Broadcom, or Qualcomm must be fabricated by the Taiwan Semiconductor Manufacturing Company, which controls approximately ninety percent of the world’s advanced semiconductor fabrication capacity. The KXCO ontology maps TSMC as receiving 100% of ASML’s EUV output and transforming it into the silicon that powers every major AI model in existence. The geographic concentration is staggering: the entire leading-edge AI chip supply chain runs through a single facility complex on a single island that is the subject of intensifying geopolitical tension between the United States and China.

The ontology rates TSMC’s geographic concentration as an 85% systemic risk factor, making it the second most dangerous chokepoint in the AI sector after ASML’s EUV monopoly. Samsung Electronics and SMIC offer partial alternatives, but neither can currently match TSMC’s yield rates, process node maturity, or capacity at the sub-5nm level that AI chips require. Japan’s Rapidus is pursuing 2nm fabrication with $4 billion in state funding, but commercial-scale production remains years away. For the foreseeable future, TSMC is the only game in town, and every AI investor must account for Taiwan risk in their portfolio construction.

Company | Ticker | Role | Status / Risk |

|---|---|---|---|

TSMC | Leading-edge chip fabrication | 100% of EUV; ~90% advanced fab share | |

Samsung | $005930.KS | Memory + foundry | HBM3E producer; fab capacity below TSMC |

SMIC | Private (China) | Chinese domestic fab | $8.2B National AI Fund; US-sanctioned |

Rapidus | Private (Japan) | 2nm fab pursuit | $4B state funding; years from production |

Table 3: The foundry layer — geographic concentration and alternatives (source: KXCO AI Ontology)

The Chip Designers: Nvidia and the GPU Oligopoly

Nvidia is the most valuable company in the world, and the KXCO ontology explains why with a clarity that no sell-side research report can match. Nvidia sits at the center of 26 cross-references in the ontology, more than any other entity, because it does not merely design chips. It designs the entire ecosystem that those chips operate within: the CUDA software platform, the NVLink interconnect, the Mellanox networking stack (acquired for $6.9 billion), and the HBM memory interface that connects its GPUs to the high-bandwidth memory they depend on. The ontology rates Nvidia’s GPU dominance as an 80% systemic risk factor, meaning that the entire AI sector is overwhelmingly dependent on a single company’s product roadmap.

But Nvidia is not alone in the chip design layer. AMD is investing approximately $90 billion across a 6-gigawatt infrastructure buildout to challenge Nvidia’s dominance. Broadcom is designing custom AI accelerators (ASICs) for the hyperscalers, a business that is growing rapidly as Google, Meta, and Amazon seek to reduce their dependence on Nvidia’s pricing power. Arm Holdings, now publicly traded, licenses the architecture that underpins virtually every AI chip on the market. Qualcomm is pushing into AI inference at the edge with its Snapdragon platform. And in China, Huawei’s HiSilicon division is building a parallel chip stack using domestic fabrication, albeit at a significant process node disadvantage. The ontology tracks 36 claims and $435 billion in tracked flows across the chip design layer, making it the most capital-intensive tier in the supply chain.

Company | Ticker | AI Role | Key Metric |

|---|---|---|---|

Nvidia | GPU design + ecosystem (CUDA, NVLink, Mellanox) | 80% GPU market share; 26 cross-refs in ontology | |

AMD | GPU + CPU challenger | ~$90B infrastructure buildout; 6GW capacity | |

Broadcom | Custom AI ASICs for hyperscalers | Growing ASIC business; 3 cross-refs | |

Arm Holdings | Chip architecture licensing | Underpins virtually every AI chip design | |

Qualcomm | Edge AI inference (Snapdragon) | Pushing AI to mobile and edge devices | |

Intel | Foundry + chip design turnaround | Struggling to regain AI relevance | |

Huawei/HiSilicon | Private | China’s domestic AI chip stack | US-sanctioned; buying downgraded Nvidia H20 chips |

Table 4: The chip design layer — the $435 billion engine room (source: KXCO AI Ontology)

The HBM Triopoly: The Most Acute Bottleneck

High-bandwidth memory (HBM) is the single most acute supply chain bottleneck in the AI sector, and only three companies in the world produce it. SK Hynix, Samsung Electronics, and Micron control one hundred percent of HBM production, and the KXCO ontology identifies this triopoly as the supply chain’s most immediate constraint. The market is projected to exceed $100 billion by 2028, driven by the insatiable demand for memory bandwidth in AI training and inference workloads. SK Hynix alone supplies more than fifty percent of all HBM3E memory for AI GPUs, making South Korea a critical node in the AI supply chain that most Western investors underestimate.

The ontology’s risk radar rates the HBM triopoly at 80%, tied with Nvidia GPU dominance. The geographic concentration is notable: Korea manufactures the memory, Taiwan packages it alongside the GPU, and Japan provides critical enabling materials and equipment. Any disruption to this Korea-Taiwan-Japan axis, whether from geopolitical conflict, natural disaster, or trade restriction, would immediately constrain AI chip production worldwide. For investors, $MU (Micron) and Samsung represent the most accessible pure-play exposures to the HBM bottleneck, though SK Hynix, traded on the Korean exchange, is the market leader.

Company | Ticker | HBM Market Position | Geographic Risk |

|---|---|---|---|

SK Hynix | $000660.KS | 50%+ of HBM3E production | South Korea |

Samsung Electronics | $005930.KS | Major HBM producer; also foundry | South Korea |

Micron | Fastest-growing HBM supplier | United States ( Boise, Idaho) |

Table 5: The HBM triopoly — 100% of supply, $100B+ market by 2028 (source: KXCO AI Ontology)

The AI Labs: Where the $2.6 Trillion Valuations Live

The foundation model companies represent the most visible and most heavily funded layer of the AI sector, and the KXCO ontology tracks a combined $2,642 billion in tracked capital flows across thirteen entities. These are the companies building the large language models, the reasoning engines, and the multimodal systems that are driving demand for everything downstream. The capital intensity is staggering: OpenAI is valued at approximately $500 billion following its joint venture restructuring, Anthropic raised a $65 billion Series H at a roughly $965 billion post-money valuation, and xAI, now under the SpaceX umbrella, carries a combined valuation of approximately $1.25 trillion when including the SpaceX AI infrastructure that hosts its models.

The ontology reveals something that most market commentary misses: the capital loop. Investors fund the AI labs. The labs immediately commit that capital back to the investors’ own cloud and chip platforms. Microsoft, which owns approximately twenty-seven percent of OpenAI and has invested roughly $135 billion, rents compute to OpenAI on Azure. Amazon has committed $38 billion over seven years to Anthropic through AWS. SoftBank has pledged $500 billion over four years to the Stargate project. MGX has committed $100 billion as a first tranche. Roughly $1 trillion of announced deals is circulating inside a single cohort of investors and their portfolio companies, a closed loop of capital that inflates valuations while concentrating risk. The ontology maps this loop with 43 cross-references, making the AI labs layer the most densely interconnected tier in the supply chain.

AI Lab | Valuation / Funding | Key Investor(s) | Compute Partner |

|---|---|---|---|

OpenAI | ~$500B (JV) | Microsoft (~27%, ~$135B) | Azure |

Anthropic | ~$965B post-money (Series H) | Amazon ($38B/7yr AWS) | AWS |

xAI / SpaceXAI | ~$1.25T combined | SoftBank, SpaceX | Colossus (SpaceX-built) |

DeepSeek | $50B valuation ($7.4B raised) | Chinese domestic investors | Domestic chips |

Mistral AI | Private | European investors | Azure / cloud |

Alibaba Cloud | Public (China) | Alibaba Group | Domestic infrastructure |

Reflection AI | ~$6.3B (implied) | VC investors | Cursor customer |

Table 6: The AI labs layer — $2.6T in tracked valuations (source: KXCO AI Ontology)

The Hyperscalers: $2.2 Trillion in Tracked Flows

The compute and cloud layer is where the physical infrastructure of AI actually lives, and the KXCO ontology tracks $2,188 billion in capital flows across five entities. This is the layer that Morgan Stanley expects to drive $805 billion in combined hyperscaler capex in 2026, nearly double the 2025 figure and triple 2024 levels. Hyperscalers are expected to account for approximately forty percent of total Russell 1000 cash capital expenditure over the 2026 to 2028 period, representing more than $2 trillion in cumulative spending. This is not a sector that is slowing down. It is accelerating.

The ontology reveals a fascinating structural dynamic within this layer: SpaceX, primarily known as a rocket company, has emerged as a major AI infrastructure provider through its Colossus data center complex in Memphis, Tennessee. Colossus 1 generates an estimated $1.25 billion per month in compute revenue, with committed contracts worth approximately $45 billion through 2029, hosting training workloads for Anthropic ($45 billion), Google ($32 billion in committed spend), and even xAI, which competes with those same companies. The irony is structural and significant: a rocket company’s data centers, rented to the labs that compete with its own AI subsidiary, represent one of the most profitable infrastructure plays in the entire sector. Oracle, through its $500 billion cloud infrastructure project, and CoreWeave, valued at approximately $22 billion as a dedicated GPU cloud provider, round out the compute layer alongside the traditional hyperscalers.

Company | Ticker | Compute Role | Key Metric |

|---|---|---|---|

Microsoft Azure | Cloud AI compute + OpenAI partner | ~27% of OpenAI; $135B committed | |

Amazon Web Services | Cloud AI compute + Anthropic partner | $38B/7yr to Anthropic | |

Alphabet / Google | Cloud + Gemini + Quantum AI | $920M/mo AI revenue (~$32B/yr) | |

Meta | Self-hosted AI + Llama open models | Top-3 AI infrastructure investor (13F) | |

SpaceX / Colossus | Private | AI data center hosting | $1.25B/mo; ~$45B committed to 2029 |

Oracle | Enterprise AI cloud | $500B cloud infrastructure project | |

CoreWeave | Dedicated GPU cloud | ~$22B valuation; pure GPU play |

Table 7: The compute and cloud layer — $2.2T in tracked capital flows (source: KXCO AI Ontology)

The CEOs Speak: Five Voices Shaping the AI Future

Elon Musk: The Exponential Bet

Elon Musk, who leads both Tesla and xAI (now folded into SpaceX as SpaceXAI), continues to make the most aggressive claims about AI’s trajectory. Musk has stated that artificial intelligence could exceed the combined intelligence of all humans within the next four to five years, a prediction that, if even partially accurate, would represent the most significant event in the history of life on Earth. He has assigned a ten percent probability that Grok 5, slated for release in 2027, could achieve artificial general intelligence. Musk has also directed Tesla’s internal AI development to migrate to Grok 4.5, a decision that underscores his conviction that the future of autonomous driving, robotics, and energy management will be built on a unified AI platform that spans his companies. The KXCO ontology tracks Musk through both Tesla and the SpaceX/xAI entity, with approximately $1.25 trillion in combined valuation and 19 cross-references, making him the most connected individual in the entire AI supply chain.

“AI could exceed the combined intelligence of all humans within the next four to five years.”

— Elon Musk, CEO of Tesla and SpaceXAI

Sam Altman: The Pragmatic Roadmap

Sam Altman, CEO of OpenAI, has adopted a notably more measured public posture in 2026 compared to the breathless enthusiasm of previous years. In a widely discussed blog post titled “Reflections,” Altman stated that OpenAI is “now confident we know how to build AGI as we have traditionally understood it,” a significant rhetorical shift from speculation to engineering certainty. Altman has outlined a vision in which AGI will possess roughly the intelligence of a median human that could be hired as a coworker, a definition that is simultaneously ambitious and deliberately grounded. OpenAI’s policy blueprint envisions superintelligence arriving with sufficient force to require an entirely new social contract, and the company has signaled plans to deploy automated AI research systems that could accelerate its own model development. The KXCO ontology maps 14 cross-references for OpenAI, reflecting the company’s deep entanglement with Microsoft’s cloud infrastructure, its competitive relationships with Anthropic and Google, and its position at the center of the capital loop.

“We are now confident we know how to build AGI as we have traditionally understood it.”

— Sam Altman, CEO of OpenAI

Dario Amodei: The Safety Realist

Dario Amodei, CEO of Anthropic, occupies a unique position in the AI leadership landscape as the most prominent advocate for frontier AI safety while simultaneously building one of the most powerful AI systems in existence. Amodei has stated that we are “considerably closer to real danger in 2026” than in previous years, and has described the current moment as a “rite of passage” that could test society as severely as the development of nuclear weapons. In a statement on Anthropic’s discussions with the Department of Defense, Amodei said he believes “deeply in the existential importance of using AI to defend the United States and other democracies, and to defeat our autocratic adversaries.” Anthropic’s policy positions reflect this dual orientation: the company advocates for judicious, evidence-based regulation while simultaneously building Claude into a frontier model that competes directly with GPT and Gemini. The KXCO ontology maps 12 cross-references for Anthropic, with $65 billion in Series H funding and deep dependencies on Amazon Web Services for compute.

“We are considerably closer to real danger in 2026 than we were in previous years. This is a rite of passage for our civilization.”

— Dario Amodei, CEO of Anthropic

Jack Hidary: AI for the Physical World

Jack Hidary, CEO of SandboxAQ, the Alphabet spinoff focused on quantitative AI and post-quantum cryptography, has been among the most vocal advocates for the thesis that the next wave of AI value creation will come not from chatbots but from the application of AI to the physical world. In a widely cited appearance on CNBC’s Squawk on the Street in July 2026, Hidary declared that 2026 will be an “explosive year” for AI, driven by the convergence of large models with robotics, materials science, and industrial automation. Hidary has articulated a vision of “AI for the physical world” in which quantitative AI techniques, combining large computational models with physics-based simulations, will transform manufacturing, drug discovery, logistics, and energy production. SandboxAQ’s position in the KXCO ontology reflects this thesis: the company sits at the intersection of the AI labs, quantum computing, and defense layers, with 3 cross-references connecting it to Google (its parent), the quantum tier, and the national security ecosystem.

“2026 will be an explosive year for AI. The real value is coming from AI for the physical world, robotics, materials science, and industrial automation.”

— Jack Hidary, CEO of SandboxAQ

Alex Karp: The Enterprise Sentinel

Alex Karp, CEO of Palantir Technologies, has emerged as the most outspoken critic of the consumer AI hype cycle while simultaneously presiding over one of the most successful AI-powered enterprise software companies in the world. On Palantir’s Q1 2026 earnings call, Karp delivered what has become one of the defining statements of the AI investment era, warning of “AI slop,” his term for unreliable, ungoverned model outputs that he described as a systemic risk to enterprises that fail to adopt rigorous AI governance. Palantir posted eighty-five percent year-over-year revenue growth in Q1 2026, beating analyst estimates and raising full-year revenue guidance to $7.656 billion, representing seventy-one percent growth. Karp has been sharply critical of the token-based AI model that dominates the consumer market, arguing that enterprises and governments need to own their data and their AI infrastructure rather than renting it from a single corporation. His philosophical framing positions Palantir as the antidote to AI slop: a company that builds AI platforms where governance, auditability, and institutional control are primary design principles rather than afterthoughts. The KXCO ontology tracks Palantir in the tech companies and capital layers, with 10 cross-references reflecting its dual role as both an AI platform provider and a significant holder of other AI assets.

“We stand on the walls, sentinels of the inner sanctum, against the assault of AI slop. Enterprises that fail to adopt rigorous AI governance are exposing themselves to systemic risk.”

— Alex Karp, CEO of Palantir Technologies

Power and Infrastructure: The $17 Billion Bottleneck Nobody Talks About

The KXCO ontology identifies power and infrastructure as a critical but underappreciated tier in the AI supply chain, with $17 billion in tracked flows across three entities. The explosive growth of AI compute has created an electricity demand shock that is straining grids worldwide. Bank of America Institute data shows that electricity demand from GPU-based servers is growing at roughly thirty percent per year, driven increasingly by AI inference workloads rather than training. Constellation Energy has signed a $16 billion, twenty-year power purchase agreement to supply a single AI data center complex. Talen Energy secured a $650 million deal to repower a former nuclear facility for AI compute. These are not small transactions. They represent a fundamental restructuring of the energy-AI nexus that will define infrastructure investment for the next decade.

Company | Ticker | AI Power Role | Deal Size |

|---|---|---|---|

Constellation Energy | Nuclear + clean power for AI data centers | $16B, 20-year PPA | |

Talen Energy | Repurposed nuclear for AI compute | $650M deal | |

Celestica | Data center integration and buildout | Integration partnership |

Table 8: Power and infrastructure — the $17B bottleneck (source: KXCO AI Ontology)

The Quantum Frontier: Post-Classical Threat

The KXCO ontology maps a quantum computing tier with three entities and six cross-references, reflecting the growing intersection of quantum computing with the AI supply chain. Google Quantum AI operates as a subsidiary dedicated to quantum advantage research. IBM Quantum has received approximately 2.35 trillion yen (roughly $15 billion) in total government support for its quantum development programs. And SandboxAQ, Jack Hidary’s company, represents the most commercially advanced attempt to bridge quantum computing techniques with classical AI, using large-scale quantitative models to solve problems in cryptography, materials science, and national security. The ontology flags quantum computing as a “post-classical threat” to current encryption standards, a risk that is accelerating investment in post-quantum cryptography across the defense and financial sectors.

Data Centers: The $1.6 Trillion Physical Footprint

The data center layer is where the AI supply chain becomes physical, and the KXCO ontology tracks $1,645 billion in capital flows across four entities. SpaceX’s Colossus complex in Memphis is the most visible symbol of this buildout, but it is far from alone. The Stargate project, backed by SoftBank ($500 billion over four years) and MGX ($100 billion first tranche), represents the largest single AI infrastructure commitment in history. Crusoe Energy and Abilene are building dedicated AI data centers powered by natural gas to bypass grid constraints. The scale of construction is unprecedented: the United States is adding more data center capacity in 2026 alone than it added in the entire previous decade. This buildout is the physical manifestation of every bank forecast on this list, and it is creating investment opportunities in construction, cooling systems, power generation, and real estate that extend far beyond the pure technology names.

The Capital Loop: Who Funds Whom

The KXCO ontology’s capital and investors layer is perhaps its most revealing section, tracking 22 entities, 39 claims, and $1,019 billion in tracked flows. The pattern is clear: a small number of institutional investors, sovereign wealth funds, and technology corporations are recycling capital between themselves in a loop that inflates valuations while concentrating risk. Microsoft invests in OpenAI. OpenAI spends on Azure. Amazon invests in Anthropic. Anthropic spends on AWS. SoftBank invests in Stargate. Stargate spends on Nvidia. Nvidia spends on TSMC. TSMC spends on ASML. The money flows in a circle, and at each node, a company’s valuation increases, creating paper wealth that is used to justify the next round of investment. The ontology estimates that roughly $1 trillion of announced deals are circulating inside this loop, a figure that should give every investor pause even as it demonstrates the extraordinary momentum of the AI buildout.

Investor | AI Commitment | Primary Beneficiary |

|---|---|---|

Microsoft | ~$135B total (~27% OpenAI) | OpenAI |

Amazon | $38B / 7yr (AWS) | Anthropic |

SoftBank | $500B over 4 years | Stargate / xAI |

MGX | $100B first tranche | Stargate |

QIA (Qatar) | Private | Various AI infrastructure |

Founders Fund | Private | Multiple AI labs |

a16z | Private | AI startups |

BlackRock / Vanguard | Index / passive | Entire AI sector via market weight |

Table 9: The capital loop — $1T+ circulating inside one investor cohort (source: KXCO AI Ontology)

The Geopolitical Overlay: Dependence, Decoupling, and Risk

The KXCO ontology maps seven geopolitical regions and their dependencies with a clarity that should be required reading for every AI investor. The United States has 98 dependencies in the ontology, the highest of any nation, and is critically dependent on Taiwan for one hundred percent of its leading-edge AI chip fabrication and on the Netherlands (ASML) for one hundred percent of EUV lithography. China, with 12 dependencies, is building a parallel AI stack using domestic alternatives, but the gap in chip performance remains significant: China bought one million downgraded Nvidia H20 chips in 2024 versus 450,000 domestic Ascend chips. The European Union’s four dependencies are concentrated in ASML, its sole strategic asset in the AI supply chain. Taiwan’s three dependencies all relate to its role as the world’s sole source of advanced AI silicon. South Korea’s three dependencies reflect its dominance in HBM production, with SK Hynix supplying more than half the world’s AI memory. Japan’s nine dependencies reflect its role as an enabler through companies like Rapidus and critical materials suppliers.

The ontology rates US-China decoupling as a 90% geopolitical risk factor, the highest in its risk radar. This is not a distant concern. Export controls on advanced chips, restrictions on ASML sales to China, and the rapid buildout of China’s domestic alternatives are all accelerating simultaneously. Investors who are not accounting for the possibility of a bifurcated AI ecosystem, one Western, one Chinese, with reduced interoperability and increased costs for both, are underestimating the structural risks in this sector.

KXCO Risk Radar: Systemic Vulnerabilities | |

ASML monopoly on EUV | 95% risk |

US-China decoupling | 90% risk |

TSMC geographic concentration | 85% risk |

HBM triopoly (SK Hynix/Samsung/Micron) | 80% risk |

Nvidia GPU dominance | 75% risk |

Table 10: KXCO AI Ontology Risk Radar — the five systemic vulnerabilities

How to Play It: A Layered Allocation Framework

Based on the KXCO ontology structure and the consensus forecasts from Goldman Sachs, Morgan Stanley, UBS, Bank of America, and JP Morgan, we propose a layered allocation framework that mirrors the physical structure of the AI supply chain. The logic is simple: own the chokepoints, the monopoly or near-monopoly positions that every other layer depends on, and supplement with exposure to the fastest-growing demand drivers. The ontology makes this allocation strategy visible in a way that no amount of sell-side research can replicate, because it maps the actual dependency chains rather than theoretical market share estimates.

Layer | Priority | Key Tickers | Rationale |

|---|---|---|---|

Equipment (Root) | Highest | 100% EUV monopoly; sector gatekeeper | |

Foundry (Trunk) | Highest | 90% advanced fab; Taiwan risk premium | |

HBM Memory | High | Fastest-growing HBM supplier; US-based | |

Chip Design | High | GPU + ASIC dominance; ecosystem moats | |

Hyperscalers | Medium | Capex acceleration; AI revenue inflection | |

AI Platforms | Medium | Enterprise AI governance; 85% revenue growth | |

Power / Infra | Medium | Electricity bottleneck; nuclear renaissance | |

Networking | Lower | InfiniBand/Ethernet for AI data centers | |

Watch | Private (IBM, GOOG) | Post-classical threat; long-dated optionality |

Table 11: Layered AI allocation framework based on KXCO AI Ontology structure

The KXCO AI Ontology is the most comprehensive map of the AI supply chain available to investors today. It is live, it is verifiable, and it is updated with real-time data on capital flows, dependencies, and risk concentrations. We reference it throughout this article because we believe that AI stock investing without ontology-level visibility is equivalent to navigating without a map. The sector is too complex, the dependencies too deep, and the capital flows too large for traditional stock-picking approaches to capture the full picture. Explore it at https://kxco.ai/ontology-live/ and see the supply chain for yourself.

#AIStocks #ArtificialIntelligence #Nvidia #OpenAI #Anthropic #Palantir #Hyperscalers #SemiconductorStocks #AICapEx #KXCO #AIOntology #MachineLearning #DeepLearning #TechInvesting #GPU #HBM #TSMC #ASML #QuantumComputing #xAI #SpaceXAI #SandboxAQ #EnterpriseAI #AGI #AISafety #WallStreet #StockMarket #Investing2026

Earnings Season Kicks Off

Earnings season is about to deliver the next chapter in the AI capital expenditure supercycle. Wall Street expects $NVDA and $SPCX to be the big winners, but the real story is how early we still are in this cycle.

AI Stocks Are War Stocks

The Pentagon is pouring $13.4 billion into AI this year, and a new generation of tech-native defense companies — Palantir, Anduril, SpaceX — are capturing the lion's share of the fastest-growing military spending category in history.

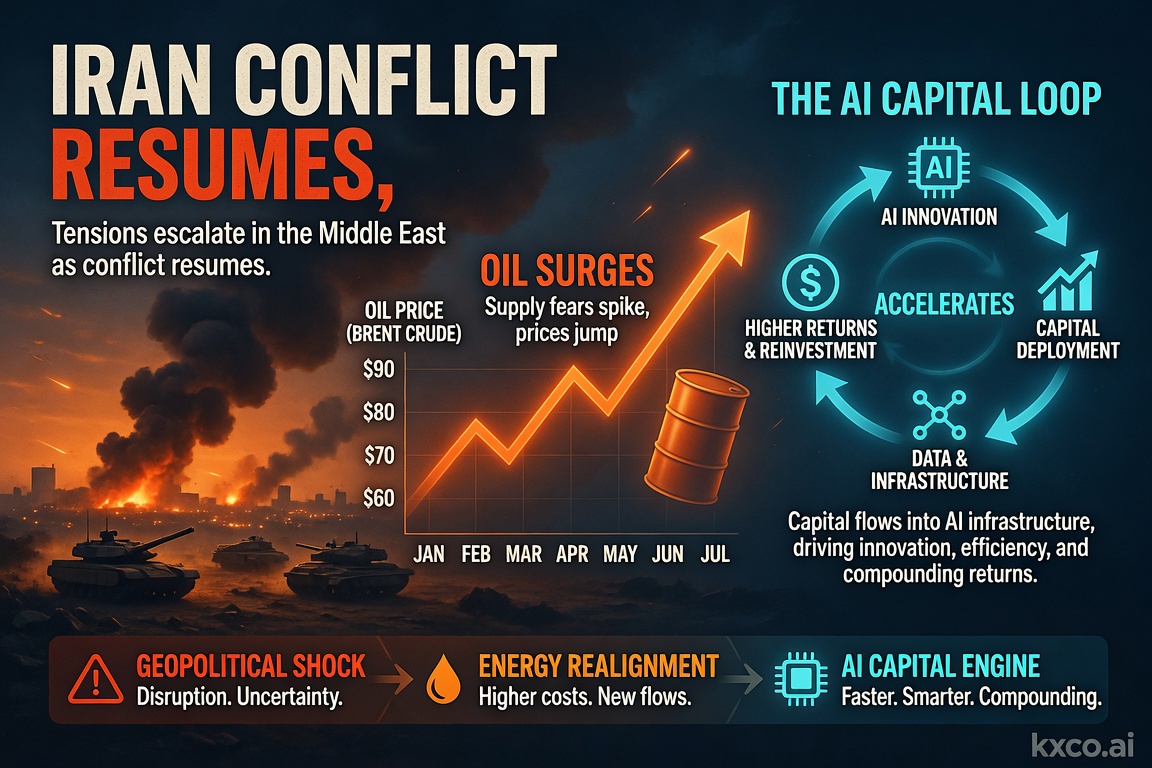

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

Who Is Who in the AI Space: The Definitive Guide to AI Stocks in 2026

The definitive 2026 guide to AI stocks: $NVDA, $GOOGL, $MSFT, $AMZN, $META, $TSM, $AVGO, $ORCL and $PLTR in the US; $BABA, $TCEHY and $BIDU in China — each mapped to its layer of the AI value chain, with cashtags, market caps and the investment thesis for each.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.