The Rise & Fall of Crypto’s Most Iconic Hedge Fund: Three Arrows Capital

#crypto #3AC #bitcoin #ether #Fed

"This is the story of how one cryptocurrency hedge fund 3AC kept getting it right until it did not"--Paul Ebeling

In Y 2018, leaning back against a well-cushioned leather sofa in a seaside bungalow in Sentosa Cove belonging to another cryptocurrency mogul, Su Zhu was basking in the aura of his power and influence as he nursed a 21-year-old whiskey at a “crypto insiders” party.

For Zhu, this was his moment of peak crypto.

Surrounded by hangers-on trying to pitch him their latest project, Zhu largely ignored the cacophony of voices that were droning around him as he sipped his drink.

Zhu and Kyle Davies, former high school classmates and founders of 3AC, a Singapore-based cryptocurrency hedge fund, had just secured an early investment in Terra Luna, giving them access to hundreds of millions of dollars’ worth of Luna tokens.

For 3AC, the investment in Terra Luna was made more special by the fact that some of the biggest names in crypto were also backing the algorithmic stablecoin project, including Galaxy Digital, whose CEO Mike Novogratz would soon go on to tattoo the Luna logo on his upper arm and Pantera Capital.

Terra Luna also counted Lightspeed Venture Partners, Coinbase Ventures and Jump Crypto as backers, cementing 3AC’s status as a major player in the digital asset scene.

By the time that Zhu and Davies had backed Terra Luna, they were already 1 of the Top cryptocurrency venture capitalists, backing such successful projects as Avax, Near Protocol, Aave, Deribit, Starkware and Axie Infinity, with their assets under management estimated to be as high as $18-B at one stage.

Even by late Y 2021, when Pantera Capital had sold most of its stake in Terra Luna, Zhu was busy buying, not Luna, but real estate.

As reported by Bloomberg, Zhu was shopping around for another Good Class Bungalow, Singapore’s most exclusive form of housing located in its toniest districts, to find an abode befitting his stature near the Top of the crypto world.

When Zhu wasn’t busy buying high-end Singapore real estate or superyachts, he enjoyed using his considerable influence on social media, in particular Twitter, to shape sentiment and possibly profit from it.

With over 560,000 Twitter followers, Zhu was known for using psyops and playing mind games with his followers, creating a thread in November 2021 that flamed Ethereum, while taking advantage of the drop in prices to snap up some $660 million worth of Ether.

Like the boy who cried wolf, Zhu’s frequent use of Twitter to talk up or spread fud (fear, uncertainty and doubt) about tokens made it difficult for followers to determine if he was gaming his audience for profit, or serious in his views, and often it appeared to be both.

Nevertheless, plenty of people held Zhu and 3AC in high regard, especially given that Zhu had correctly predicted the end of the “Crypto Winter” in Y 2018 and that Bitcoin would break its all-time-high in Y 2020.

However what Zhu and Davies had not factored in is that just as the Fed giveth, it also taketh away.

With global economies battered by the coronavirus pandemic and lockdowns, the flood of fiscal and monetary stimulus pouring into the financial system floated all manner of assets, including cryptocurrencies, feeding into Zhu’s bullish view on cryptocurrencies.

But by December 2021, soaring inflation was already forcing the Fed’s hands, with a rate hike in November of that year leading to a slip in asset prices that had thus far been punch-drunk off the central bank’s seemingly endless firehose of liquidity.

Undeterred, Zhu took to his pulpit to proclaim that this was the opportune time to double down on cryptocurrencies, borrowing a theme from legendary value investor Warren Buffett to “be greedy when others were fearful.”

Just days before Bitcoin slipped below US$40,000, and two months before 3AC would file for bankruptcy, Zhu, in his characteristic deadpan, declared at a podcast recording for cryptocurrency exchange FTX,

“When there’s a lot of despair, you can start buying. You don’t have to follow the despair.”

Yet the despair in financial markets in general and the cryptocurrency markets in particular was not unwarranted.

With the U.S. facing the greatest inflationary pressures in four decades, Fed policymakers started to unwind many of the pandemic-era measures which had contributed in no small part to the success of both the cryptocurrency markets and 3AC.

Even as cryptocurrency veterans like Pantera Capital were unloading their stake in Terra Luna, Zhu continued to talk up the merits of the algorithmic stablecoin, leading some to wonder if the 3AC cofounder was in fact looking to offload his holdings.

On 26 December 2021, Zhu bragged about the future growth prospects of Terra Luna in a tweet,

“We’re seeing some of the earliest and most ambitious ideas in crypto starting to unfold. Crosschain decentralized stablecoin backed entirely by digitally native assets was the holy grail in 2016. Bless $BTC $LUNA.”

“People down 50X more from selling early than from buying top this year, and it’s not even close, SOL, LUNA, AVAX, MATIC, DOGE, SHIB, FTM, list goes on. Tops are emotionally memorable because plebs snapshot themselves to a portfolio all-time-high, yet nobody buys top while everyone sells early.”

Despite roiling markets, Zhu walked with the cocky confidence of someone who had made it from humble beginnings to being hounded by global media and many believed that the bulk of 3AC’s funds were proprietary, making them bulletproof when in fact, they were not.

A venture investor in some of the best-known cryptocurrency startups, in many cases, 3AC also served as a manager of their corporate treasuries, which helped it to circumvent the regulatory restrictions of its Registered Fund Management Company (RFMC) license.

As early as Y 2013, 3AC held an RFMC, a type of fund management license administered and governed by the Monetary Authority of Singapore (MAS), but which came with specific restrictions that few investors were aware of.

An RFMC only allows up to 30 professional investors and a maximum of $250 million in assets under management, limitations which 3AC got around creatively.

Instead of managing a fund which promised a return on investment, 3AC would borrow money from investors, and promise a projected coupon rate, structuring these investments as loans instead of what they were marketed as; investment products, and thereby declaring these funds as “proprietary capital,” which was misleading to say the least.

But by September 2021, concerned that these workarounds would eventually surface, 3AC novated the management of its only fund to an offshore entity in the British Virgin Islands, notifying MAS in February 2022 that it intended to cease fund management activity in Singapore from May.

By late Y 2021, Zhu also publicly declared that 3AC was relocating to Dubai, an uncontroversial move at the time, given that many other cryptocurrency companies were doing the same.

However, 3AC had not applied for any fund management license in Dubai nor notified regulators in the United Arab Emirates of its intention to do so.

Publicly, Zhu remained sanguine on the prospects of cryptocurrencies, arguing on Twitter that Y 2022 would mark the year of peak adoption, even as investors were fleeing risk assets in the face of rising interest rates and tighter monetary conditions.

Many believed that Zhu was engaging in his usual psyops, to get other investors to soak up the bags of cryptocurrencies that he was looking to offload.

In reality however, Zhu, having correctly predicted market turnarounds in the past, was convinced that this time was no different, borrowing heavily to bet big that cryptocurrencies would eventually rebound.

In May this year, 3AC attempted to plug the hole caused by the collapse of Terra Luna, soaking up some $560-M in worth of Locked Luna tokens, a stake which would be worth around $600 by late June, and go on to become worthless.

Unfortunately, 3AC’s bid to shore up Terra Luna was ultimately futile, and the price of Luna kept falling, taking the rest of the cryptocurrency market with it, at a time when sentiment was already weak.

Even as things started looking bleak in January, Zhu was still showing off pictures of his latest trophy acquisition, a 171-foot Sanlorenzo 52Steel superyacht, that was intended for delivery this month, to investors and friends, presumably to maintain an air of invincibility.

It would later turn out that 3AC was only able to pay the down payment on the $50-M superyacht, and it’s been suspected that even that was paid for with borrowed money.

As Zhu and Davies were going hat in hand to investors to raise more money, 3AC was keeping secret its massive margin long position on Bitcoin, with a liquidation price of $24,000, betting that the cryptocurrency would never fall that low.

Some have speculated that Zhu and Davies may have engaged in “revenge trading” where a trader borrows even more money to trade their way out more quickly of a hole they dug themselves in by using leverage.

Unfortunately, by mid-June, 3AC had started missing margin calls from the companies funding its trades, including many major crypto lenders, who are now known to have offered the hedge fund undercollateralized loans.

Given how volatile cryptocurrencies are, most lenders are only willing to lend a fraction of the value of digital assets pledged as security for a loan, yet somehow Voyager Digital, a crypto broker and lender, lent around $700-M to 3AC, undercollateralized.

Voyager Digital was hardly alone in extending undercollateralized loans to 3AC, with fellow cryptocurrency broker and lender Genesis alleged to be facing losses of as high as 9-figures.

It has now surfaced that BlockFi and BitMEX have exposure to 3AC as well and the list of affected counterparties reads like a who’s who of the crypto world, including Cumberland DRW, Galaxy Digital and crypto options exchange Deribit.

Even before the walls started closing in on 3AC, in a desperate bid for liquidity, Zhu and Davies were said to have solicited Bitcoin from large holders known as “whales” as well as other trading firms and are thought to have lied about their assets under management in a bid to secure fresh loans.

Undeterred by the rapidly deteriorating market conditions, Zhu and Davies are said to have promised yields of as high as 20% to potential Bitcoin lenders despite liquidity and speculation, the Key driver of lending yields, rapidly drying up, but most potential lenders detected something amiss and declined doing business with the pair.

And although Zhu tweeted that 3AC was working with relevant counterparties and remained “fully committed to working this out,” in reality both he and Davies had been ghosting their creditors for some time.

When cryptocurrency prices started to falter in the wake of the Terra Luna collapse in May, lenders approached 3AC to ask for collateral, but struggled to contact the pair, forcing these lenders to liquidate the fund’s positions and causing Bitcoin to fall even further from $24,000 to $20,000.

Those liquidations sparked off a spiral of cascading defaults and triggered a run on several major crypto lenders, some of which have already gone into bankruptcy.

Throughout the debacle, creditors claim that Zhu and Davies were nowhere to be found, although some suspect that they may have decamped to Dubai.

According to 1 source, Zhu was urgently trying to sell a $35-M house in Singapore, which was being held in trust for his daughter, and with the proceeds of the sale to be transferred to a bank account in Dubai.

A search of registry records suggests that Zhu, Davies, and parties connected to the duo, as opposed to 3AC own a fleet of high-end cars, and at least 5 high-end properties in Singapore, including the $35-M Good Class Bungalow and another $28.5-M property of the same type held by Zhu’s wife, Tao Yaoqiong.

Most, if not all of these assets are likely to remain out of the reach of Three Arrow Capital’s liquidators who are now desperately trying to seize them.

For starters, the 3AC that is being liquidated was incorporated in the British Virgin Islands and the process of liquidators in that jurisdiction attempting to enforce any judgments in Singapore will be complicated and drawn out.

To make matters worse, Zhu is only known to have held in his own name a $4.5-M strata bungalow at Goodwood Grand, located in the Balmoral Road neighborhood.

3AC’s liquidators will likely have their work cut out for them if they want to go after the assets of the fund’s founders because they would need to prove beyond a reasonable doubt that Zhu and Davies were guilty of criminal misconduct.

Although 8 Blocks Capital, a smaller market maker which claims it used 3AC’s trading accounts for fee discounts, and alleges that the hedge fund misappropriated as much as US$1 million of their funds without permission, possibly in an attempt to meet margin calls, no other counterparties have alleged any criminal behavior.

Complicating the job of liquidators, 3AC filed a petition in the US Bankruptcy Court for the Southern District of New York and seeking protection from creditors in the US under Chapter 15 of the US Bankruptcy Code, which allows foreign debtors to shield US assets.

For now, nobody really knows where Davies and Zhu are, with the former having surfaced for a Wall Street Journal interview only to disappear soon thereafter, with the latter resurfacing only for the occasional tweet.

The Monetary Authority of Singapore has issued a reprimand of 3AC and is investigating, and Solitaire LLP, the Singapore lawyers retained by the fund, claim that the firm is keeping regulators apprised of developments, but such investigations typically take a considerable amount of time.

It’s unclear whether Zhu and Davies are guilty of any impropriety or financial misconduct towards the end of their reign as princes of the crypto world.

Ultimately 3AC’s legacy and contribution to the cryptocurrency industry will be forgotten under a deluge of allegations and litigation.

3AC was 1 of the industry’s biggest success stories and 1 of its biggest cautionary tales.

Have a prosperous day, Keep the Faith!

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

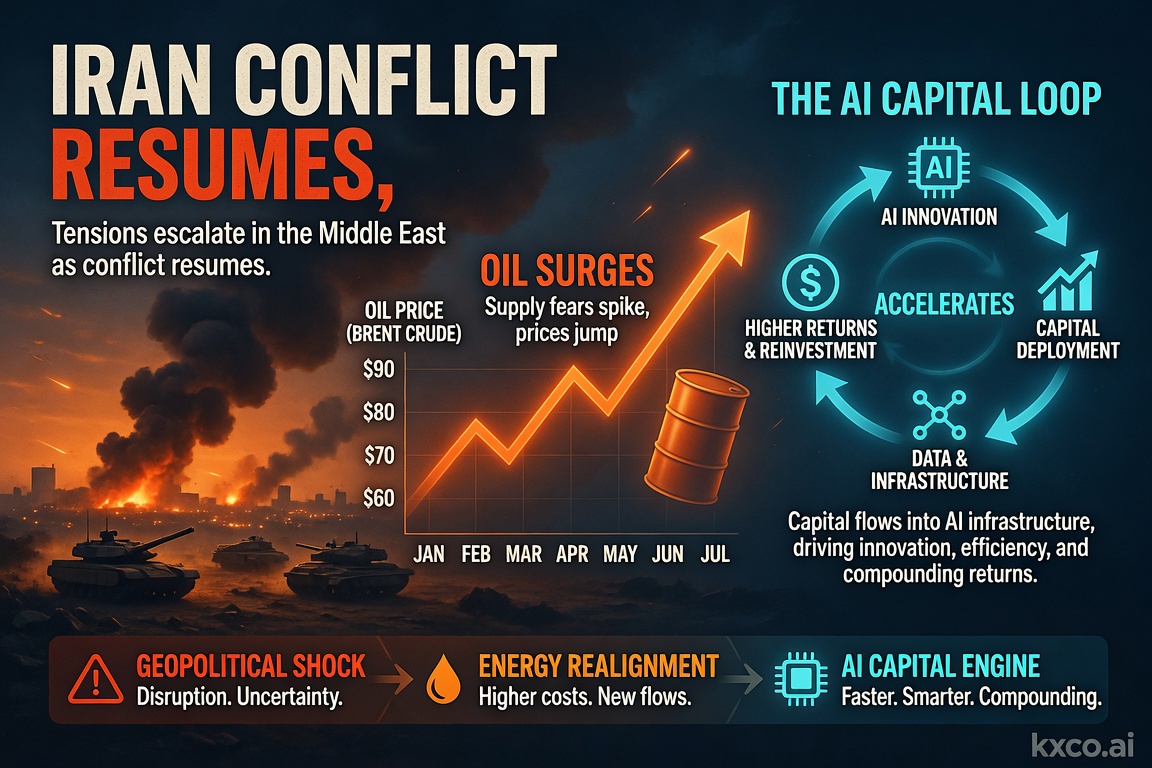

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

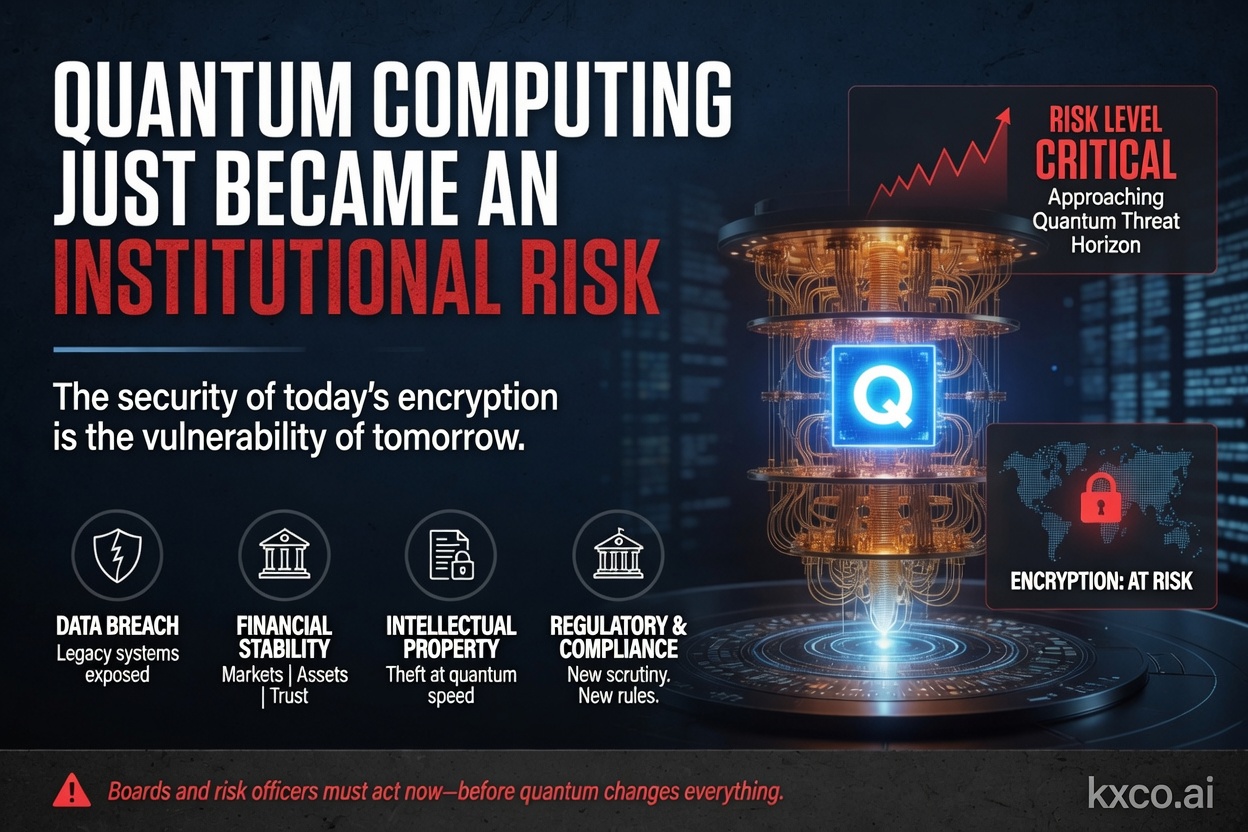

Quantum Computing Just Became an Institutional Risk

Shayne Heffernan on BlackRock's quantum-computing warning for Bitcoin and Ethereum, Google's cryptanalysis research, the two on-chain risk vectors, and how KXCO's Armature L1 — post-quantum from genesis, coordinated by its ontology — answers a threat that just went institutional.

Economic Calendar and Trading Strategies for July 7–11, 2026

A trader's guide to the week of July 7–11, 2026: the US and China economic calendar, the Fed-pivot test after a soft jobs report, and how to trade Nvidia, SpaceX, Bitcoin, the dollar, gold, silver, AI and quantum. Track every release on Live Trading News.

ASEAN: The Next Great AI Superpower

AI is not software; it is infrastructure — power, land, water, fibre and chips. Shayne Heffernan on why Southeast Asia is emerging as the third pole of global AI, where the hyperscalers are building, and how to invest.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.