Fed Ready to Move on Rates $ENPH $F $UPST $RIVN

The Fed's Potential Pivot: Decoding Signals in Latest Inflation Data

Recent developments in the Federal Reserve's preferred inflation gauge are sparking speculation that the central bank may be considering a shift in its monetary policy. The Personal Consumption Expenditures (PCE) index, a key metric monitored by the Fed, has shown signs of cooling inflation, raising expectations of a possible rate cut after two years of hikes. This article delves into the details of the latest inflation data and the potential implications for the Fed's future policy decisions.

Inflation Metrics Overview: The December PCE data revealed that the overall index grew by 2.6% year over year, consistent with the previous month's reading. Notably, the "Core" PCE, excluding volatile food and energy components, expanded by 2.9%, a decline from the previous month's 3.2% and below economists' expectations of 3.0%. Core PCE is particularly emphasized by Fed Chair Jerome Powell in assessing inflation trends.

Potential Beneficiaries of a Fed Rate Cut in USA Stocks:

Industry

Reason for Potential Benefit

Real Estate Investment Trusts (REITs)

- Realty Income Corp. (O)

REITs rely on debt financing, so lower rates benefit borrowing costs and boost investment potential.

- Brookfield Infrastructure Partners (BIP)

Similar to O, BIP's infrastructure investments and debt reliance make it sensitive to interest rate changes.

Consumer Discretionary

- Upstart Holdings (UPST)

Lower rates could revive credit demand for Upstart's AI-powered lending platform, boosting its core business.

- Ford Motor Co. (F)

Reduced borrowing costs could benefit automakers like Ford in terms of car loans and production financing.

Technology

- Mobileye Global Inc. (MBLY)

Lower rates could boost consumer purchases of autonomous driving systems, benefiting Mobileye as a leader in the field.

- NVIDIA Corp. (NVDA)

Semiconductor demand for AI and related tech could increase with a rate cut, potentially benefiting NVIDIA.

Consumer Staples

- The Honest Company, Inc. (HNST)

Consumer staples often see increased demand during economic downturns, which could be triggered by a rate cut.

Growth Stocks

- Enphase Energy, Inc. (ENPH)

Renewable energy adoption could accelerate with lower borrowing costs, potentially reviving growth stocks like Enphase.

- Rivian Automotive, Inc. (RIVN)

Cheaper financing could boost electric vehicle purchases and benefit Rivian as a prominent EV manufacturer.

Month over month, core PCE increased by 0.2% in December, up from 0.1% in November. Importantly, the annualized core PCE over the last three and six months has fallen below the Fed's 2% target.

Interpreting the Data: Capital Economics Deputy Chief US Economist Andrew Hunter highlighted that core PCE has consistently aligned with the Fed's 2% target for seven months. This suggests that there may be limited disinflation left to achieve, providing the Fed with room to contemplate interest rate cuts while maintaining economic resilience.

Powell's View and Market Expectations: Fed Chair Jerome Powell has indicated a desire to "reduce restriction on the economy" well before inflation hits 2%. The recent disinflationary trend in the data supports this view. Goldman Sachs Chief Economist Jan Hatzius emphasized that the ongoing disinflationary trend remains intact, potentially paving the way for rate cuts.

Market Reaction: Ahead of the latest data, markets had priced in a roughly 50-50 chance of a rate cut in March, as indicated by the CME FedWatch Tool. The market's response underscores the potential impact of inflation dynamics on the central bank's future decisions.

Economic Landscape: Despite the cooling inflation data, recent positive economic indicators, including higher-than-expected fourth-quarter growth and strong readings in the S&P Flash PMI, suggest ongoing economic resilience. Consumer spending remains robust, contributing to a labor market that shows signs of stability.

The recent PCE data, aligning with other inflation metrics, has set the stage for speculation about a potential shift in the Fed's stance. The combination of solid economic growth and falling inflation supports the notion of a soft landing. As the Fed's interest rate decision approaches, market participants eagerly await signals from policymakers, anticipating the central bank's response to evolving economic conditions.

Navigating Interest Rates in a U.S. Election Year: Impact and Expectations

As the United States gears up for another election year, one crucial aspect that financial markets and policymakers closely monitor is the trajectory of interest rates. Historically, interest rates have played a significant role in shaping economic sentiment, and their behavior during election years can have far-reaching implications. This article explores the patterns, potential impacts, and expectations surrounding interest rates in the U.S. during an election year.

Historical Patterns: Over the years, historical data suggests that interest rates in the U.S. tend to exhibit certain patterns during election cycles. The Federal Reserve, the country's central bank, often carefully manages interest rates to achieve specific economic goals. During election years, the Fed may fine-tune its approach to balance economic stability and support.

Rate Stability: The Fed typically aims for interest rate stability in election years to avoid causing unnecessary economic volatility. Sudden or drastic changes in interest rates could impact consumer spending, investment decisions, and overall economic sentiment.

Economic Indicators: The central bank closely monitors various economic indicators, including inflation, employment levels, and GDP growth. The Fed's decisions on interest rates may be influenced by its assessment of these indicators leading up to and during an election year.

Market Expectations: Financial markets often react to political developments, and election years are no exception. Investors may adjust their expectations based on the perceived economic policies of political candidates, influencing the demand for certain financial instruments and affecting interest rates.

Potential Impacts: The relationship between interest rates and election years can result in several impacts on the U.S. economy:

Consumer and Business Confidence: Interest rates can influence consumer and business confidence. Stable or lower rates may encourage borrowing and spending, stimulating economic activity. On the other hand, rising rates might lead to cautious consumer and business behavior.

Housing Market: Interest rates play a crucial role in the housing market. Lower rates can boost mortgage affordability and stimulate home purchases, while higher rates may dampen demand.

Stock Market Dynamics: Changes in interest rates can influence stock market performance. Investors may reevaluate their portfolios based on interest rate expectations, potentially leading to shifts in equity markets.

Expectations for 2024: As the U.S. heads into the 2024 election year, several factors will influence interest rate expectations:

Economic Recovery: The trajectory of the post-pandemic economic recovery will be a key determinant. The Fed may adjust rates based on the pace of recovery and inflation dynamics.

Inflation Concerns: Persistent inflation concerns may prompt the Fed to consider rate adjustments to maintain price stability. However, the central bank is likely to balance this with the need to support economic growth.

Global Economic Conditions: External factors, such as global economic conditions and geopolitical events, can also influence the Fed's approach to interest rates.

Interest rates during a U.S. election year are subject to a complex interplay of economic, political, and market dynamics. While historical patterns provide insights, the unique circumstances of each election cycle and the prevailing economic conditions will shape the Federal Reserve's decisions. Market participants will closely watch for signals from the central bank as it navigates the delicate balance between supporting economic growth and maintaining stability in a pivotal election year.

The history of interest rates in the United States spans several centuries and reflects the nation's economic evolution, financial crises, and the policies of the Federal Reserve. Here's a brief overview of key periods and milestones in the history of U.S. interest rates:

Late 18th Century - Early 19th Century: During the early years of the United States, interest rates were influenced by factors such as the Revolutionary War debt and the establishment of the First Bank of the United States in 1791. Interest rates were generally higher due to the risk associated with a developing nation.

Civil War Era: The Civil War (1861-1865) led to increased government borrowing, resulting in higher interest rates. The issuance of greenbacks (paper currency) and the subsequent Gold Act of 1864 affected inflation and interest rates.

Late 19th Century - Gold Standard Era: The adoption of the gold standard in the late 19th century provided stability to interest rates. Rates remained relatively low during the latter part of the 19th century, contributing to economic growth.

World War I and the Roaring Twenties: World War I led to increased government borrowing and rising interest rates. The 1920s, known as the Roaring Twenties, saw a period of economic prosperity with moderate interest rates.

Great Depression and New Deal: The Great Depression in the 1930s prompted a series of interest rate cuts to stimulate economic activity. The New Deal programs implemented by President Franklin D. Roosevelt aimed to address economic challenges.

Post-World War II Era: After World War II, interest rates remained relatively low, contributing to the post-war economic boom. The Bretton Woods Agreement in 1944 established a fixed exchange rate system with the U.S. dollar tied to gold.

1970s - Inflationary Pressures: The 1970s saw a period of high inflation, driven by factors like oil price shocks. The Federal Reserve, under Paul Volcker's leadership, implemented tight monetary policies, leading to high-interest rates to combat inflation.

1980s - Volcker's Policies and Economic Recovery: Federal Reserve Chair Paul Volcker's policies in the early 1980s succeeded in curbing inflation but led to a temporary recession. Interest rates eventually declined, contributing to economic recovery during the Reagan era.

1990s - Greenspan Era: Federal Reserve Chair Alan Greenspan's tenure saw a period of economic expansion with relatively low-interest rates. The dot-com bubble in the late 1990s and subsequent bust influenced monetary policy.

Early 21st Century - Financial Crises: The early 2000s experienced low-interest rates, contributing to the housing bubble. The 2007-2008 financial crisis prompted the Federal Reserve to implement aggressive monetary policies, including near-zero interest rates.

Post-2008 Recession to Present: The Federal Reserve maintained historically low-interest rates in the aftermath of the financial crisis to support economic recovery. The central bank implemented quantitative easing programs and adjusted rates in response to economic conditions.

Understanding the history of U.S. interest rates provides insights into the nation's economic challenges, policy responses, and the ongoing evolution of monetary policy.

Ontology Is the Idea Finance Has Been Missing

The world created around 181 zettabytes of data in 2025, and AI adds more every day than anyone can read. The scarce resource is no longer data or compute. It is understanding, and understanding is a picture. Shayne Heffernan on ontology, the visual layer that turns infinite data into insight, and why finance, banking and regulation need it most.

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

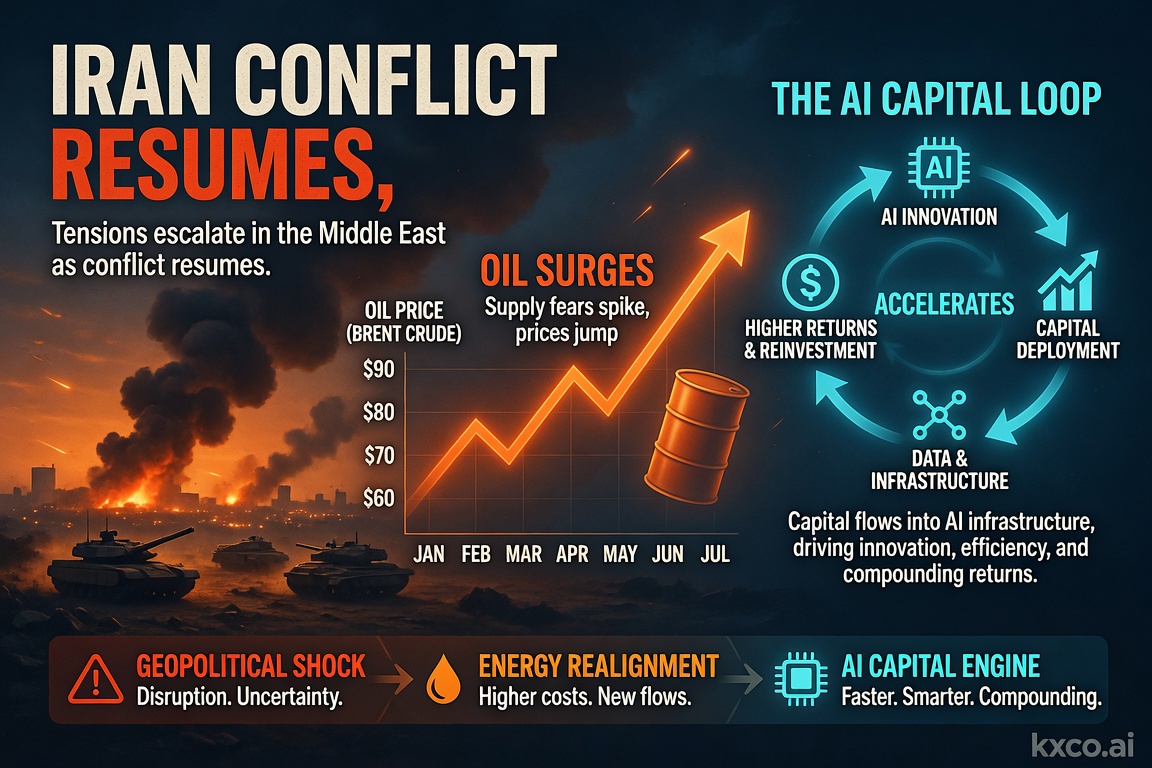

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

Ontology: Agentic AI and Infrastructure

The AI trade so far has been a compute trade. The next leg is a meaning trade — and ontology, secured and settled, is the layer almost everyone is skipping. Shayne Heffernan on why ontology is the missing layer in agentic AI, and the infrastructure it needs.

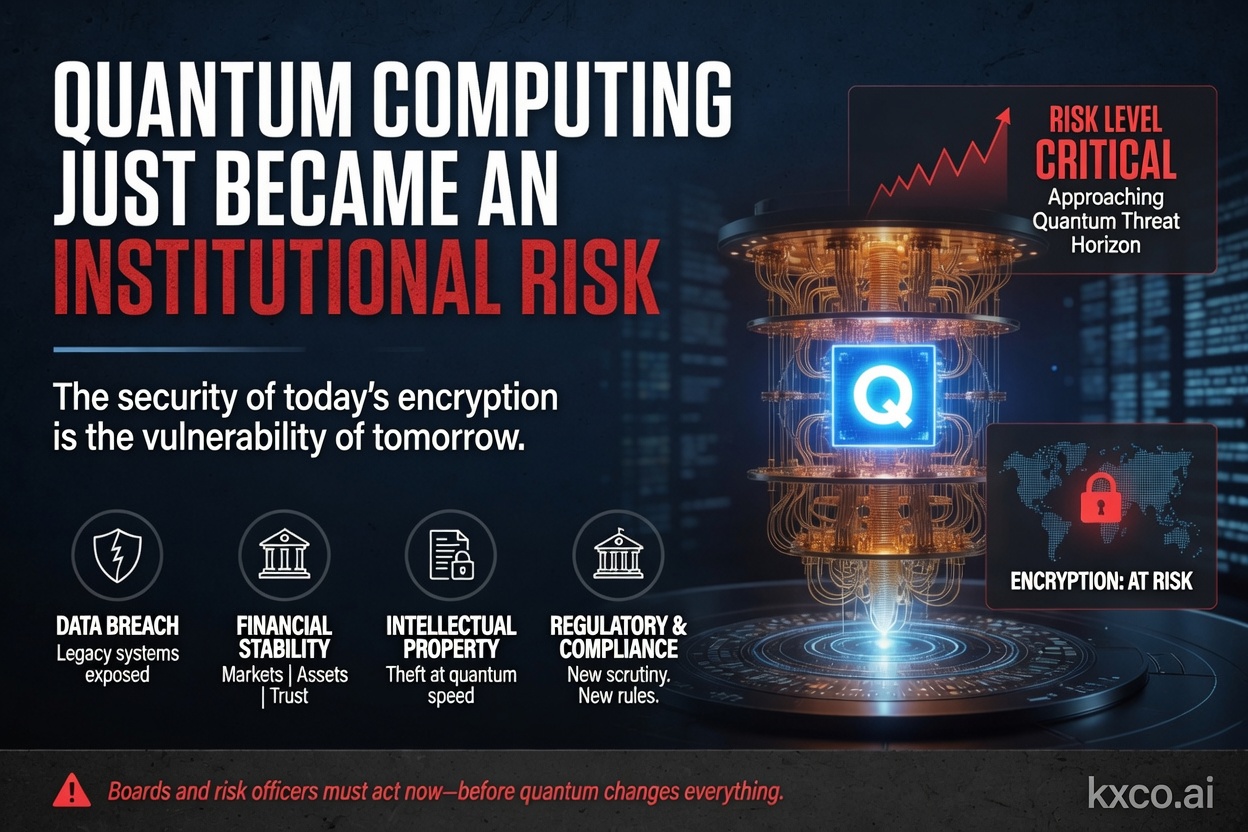

Quantum Computing Just Became an Institutional Risk

Shayne Heffernan on BlackRock's quantum-computing warning for Bitcoin and Ethereum, Google's cryptanalysis research, the two on-chain risk vectors, and how KXCO's Armature L1 — post-quantum from genesis, coordinated by its ontology — answers a threat that just went institutional.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.