China is Ramping Up Economy

Manufacturing activities outpaced expectations

Manufacturing PMI was 50.6 in February and fell from 51.3 in January, but is still expanding.

This signals some factory workers were still working during the Chinese New Year, where manufacturing activities sub PMI was 51.3 in the month, having fallen from 53.5 in the previous month. This should be the result of workers staying at work locations to spend the Chinese New Year. Some workers found a nice salary working during the holidays. Domestic orders continued to stay above 50 at 51.5 from 52.3 in January.

But external demand fell to contraction level at 48.8 in February from 50.2 before the Chinese New Year. That reflects the fact that Covid-19 cases were still high in export markets.

Honestly, the manufacturing PMIs surpassed our expectation, and shows that domestic demand can continue to support the manufacturing sector. This demand came from the technology sector, commodity sector and the construction sector.

51.5

New dometic orders Manufacturing PMI

48.9

New domestic orders Non-manufacturing PMI

Service demand expanded but not as great as we thought

Non-manufacturing PMI was 51.4 in February down from 52.4. We expected domestic orders would expand in the month but it continued to shrink from January's 48.7 to February's 48.9. This could largely be a result of continual limited orders for transporation services, both from inbound and outbound travels, as well as a lower expectation of sales after the long holiday. The next long holiday is in May.

We expect retail sales to jump over 10% year-on-year as domestic demand should be solid from job stability and wage increases. But we won't get this data until the end of March as the first three months' data are usually reported as quarterly data to avoid seasonal misalignment from the Chinese New Year.

Within all the categories of retail sales, we expect catering to resume to positive growth, which is an important indicator to show that the Covid impact on the Chinese service economy continues to fade, but a full recovery is yet to come with travel restrictions.

Ontology Is the Idea Finance Has Been Missing

The world created around 181 zettabytes of data in 2025, and AI adds more every day than anyone can read. The scarce resource is no longer data or compute. It is understanding, and understanding is a picture. Shayne Heffernan on ontology, the visual layer that turns infinite data into insight, and why finance, banking and regulation need it most.

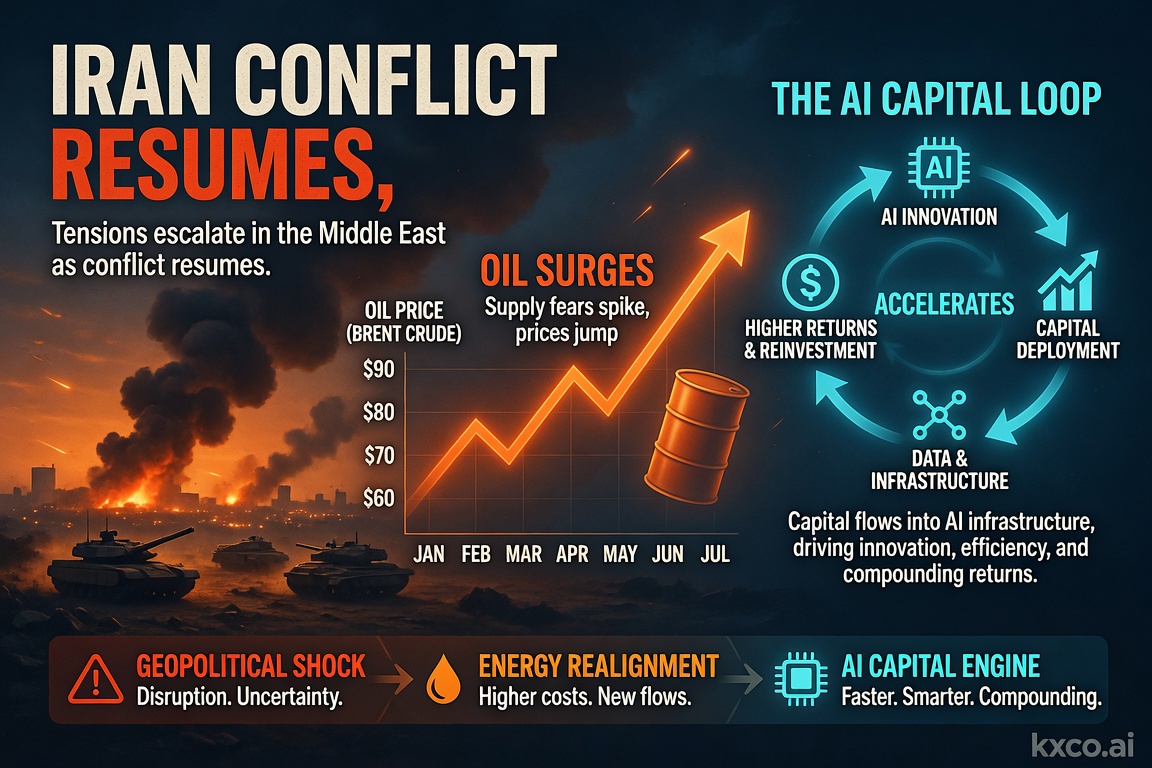

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

Ontology: Agentic AI and Infrastructure

The AI trade so far has been a compute trade. The next leg is a meaning trade — and ontology, secured and settled, is the layer almost everyone is skipping. Shayne Heffernan on why ontology is the missing layer in agentic AI, and the infrastructure it needs.

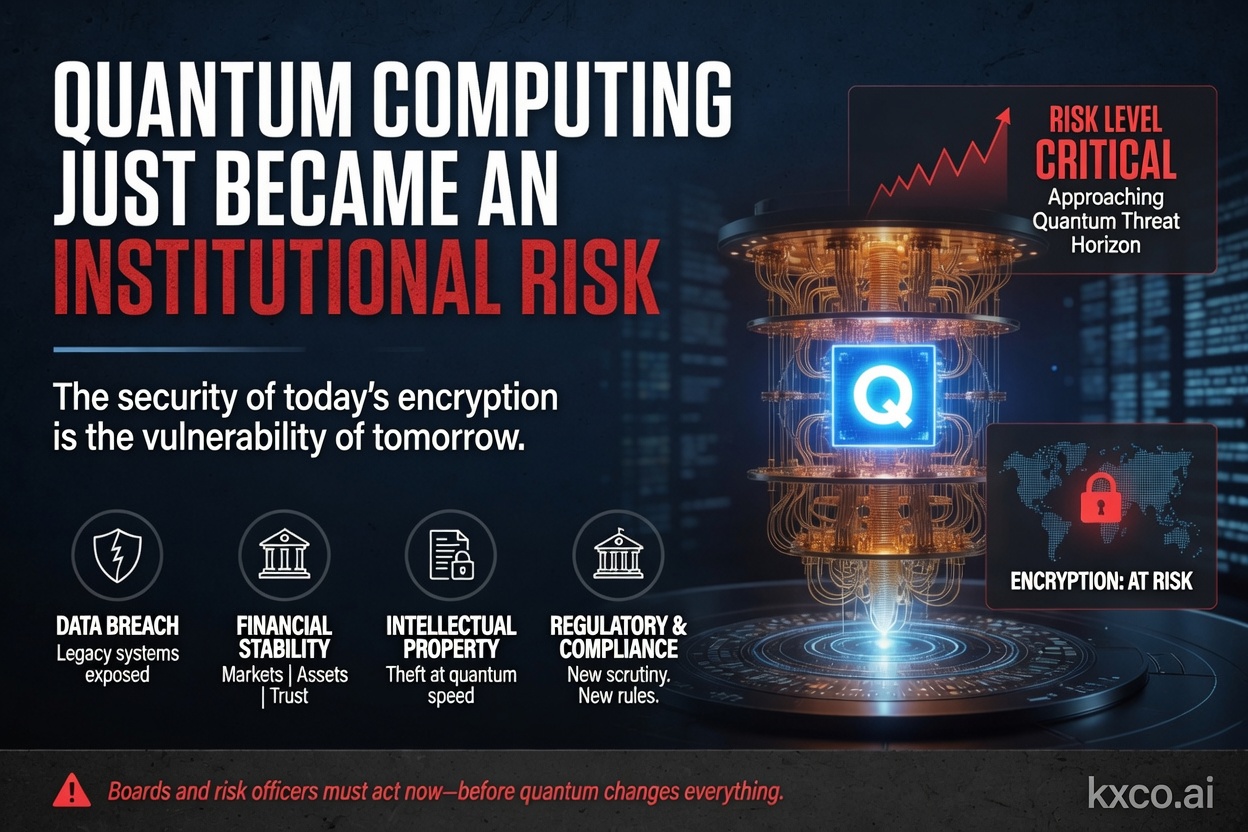

Quantum Computing Just Became an Institutional Risk

Shayne Heffernan on BlackRock's quantum-computing warning for Bitcoin and Ethereum, Google's cryptanalysis research, the two on-chain risk vectors, and how KXCO's Armature L1 — post-quantum from genesis, coordinated by its ontology — answers a threat that just went institutional.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.