Wall Street this Week $SPY $QQQ $TGT $M

From the business standpoint, retail earnings reports will remain of importance; announcements from Lowe's (LOW), Target (TGT), Macy's (M), TJX (TJX), and BJ's (BJ) will be especially noteworthy.

Everybody focused on the Fed.

The stock comeback this week was much aided by a busy economic data week. Following a lower-than-expected jobs report, worries of recession grew more pronounced; this week's statistics helped allay investors.

According to the most recent data releases, consumer spending is holding steady while layoffs aren't rising and inflation keeps moving toward the Fed's 2% target.

Economists and Wall Street analysts have suggested this week's data dump demonstrates the revered soft landing, when the US economy avoids a major economic collapse while inflation retreats to the Fed's 2% goal, is now clearly visible.

"The packed data calendar for this week presented generally positive news. Head of economics Michael Gapen of Bank of America Securities stated in a weekly note to investors on Friday, "Inflation was generally tepid and activity still looks healthy." "The current data flow fits our soft-landing projection."

A calm week of economic data will not alter that story much. But the Jackson Hole Symposium address by Federal Reserve Chair Jerome Powell might change market expectations for rate cuts. Markets are pricing in a 76% likelihood the Fed would reduce interest rates by 25 basis points by the end of its September meeting as of Friday morning. Markets a week earlier showed a more than 50% probability the Fed would carry out a 50 basis point rate reduction.

Following two weeks of whipsaw activity in markets, the S&P 500 is currently back almost at record highs. Over the previous few sessions, technology stocks have been guiding the market higher while rip-off the most recent market low. Strategists feel fairly good about the overall direction of the US economy, and Fed cuts are just around here.

Middle of August, the market seems to be right back where it entered the month taken all together. However, some strategists contend things feel a little different now following the worst sell-off of 2024.

"Sentiment looks much more balanced now than it did heading into this month," Citi US equities strategy director Drew Pettit told Yahoo Finance, citing the market downturn—particularly the more forceful retreat on the growth side of the market.

To gauge market mood, Pettit's team employs the Levkovich Index, an indicator considering investors' short holdings and leverage among other elements. With a current value of 0.31, below the 0.38 that indicates markets have entered euphoria—that is, an overstretched peak. Drawdowns generally follow past times when the market moves into euphoric zone, as the graph below shows.

This supports the thinking of the Citi Equity Strategy Team—that stocks have space to run higher this year. City predicts the S&P's end of year value to be 5,500. Moreover, Pettit said growth companies are "looking incrementally more attractive here," since segments of the market like tech are where the recent decline most affected.

Weekly calendar

Monday

Economic data: Leading Index, July (-0.3% expected, -0.2% prior)

Earnings: Estee Lauder (EL), Palo Alto Network (PANW)

Tuesday

Economic data: Philadelphia Fed Non-Manufacturing Activity, August (-19.1 prior)

Earnings: Lowe's (LOW), XPeng (XPEV), Toll Brothers (TOL)

Wednesday

Economic data: MBA mortgage applications, week ending Aug. 16, (+16.8% prior); FOMC meeting minutes, July

Earnings: Macy's (M), Target (TGT), TJX (TJX), Snowflake (SNOW), Synopsys (SNPS), Urban Outfitters (URBN), Zoom (ZM)

Thursday

Economic data: Initial jobless claims, week ending Aug. 17 (227,00 previously); S&P Global US manufacturing PMI, August preliminary (49.6 prior); S&P Global US services PMI, August preliminary (55 prior); S&P Global US composite PMI, August preliminary (54.3 prior); Existing home sales, month-over-month, July (+0.3% expected, -5.4% prior)

Earnings: Advance AutoParts (AAP), BJs (BJ), Cava (CAVA), Intuit (INTU), Peloton (PTON), Red Robin (RRGB), Ross Stores (ROST), Viking Therapeutics (VKTX), Workday (WDAY)

Friday

Economic data: New home sales month-over-month, July (+2.6% expected, -0.6% prior); Kansas City Fed services activity, August (-4 prior)

Earnings: No notable earnings.

Ontology Is the Idea Finance Has Been Missing

The world created around 181 zettabytes of data in 2025, and AI adds more every day than anyone can read. The scarce resource is no longer data or compute. It is understanding, and understanding is a picture. Shayne Heffernan on ontology, the visual layer that turns infinite data into insight, and why finance, banking and regulation need it most.

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

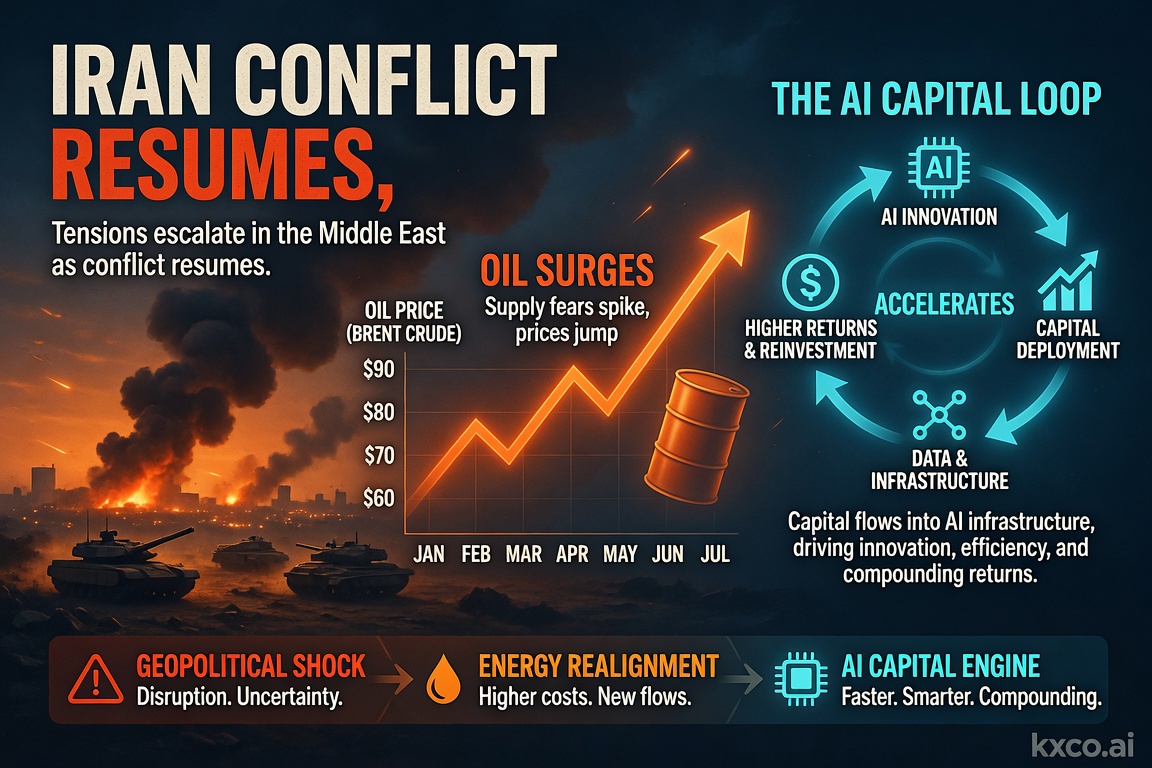

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

Ontology: Agentic AI and Infrastructure

The AI trade so far has been a compute trade. The next leg is a meaning trade — and ontology, secured and settled, is the layer almost everyone is skipping. Shayne Heffernan on why ontology is the missing layer in agentic AI, and the infrastructure it needs.

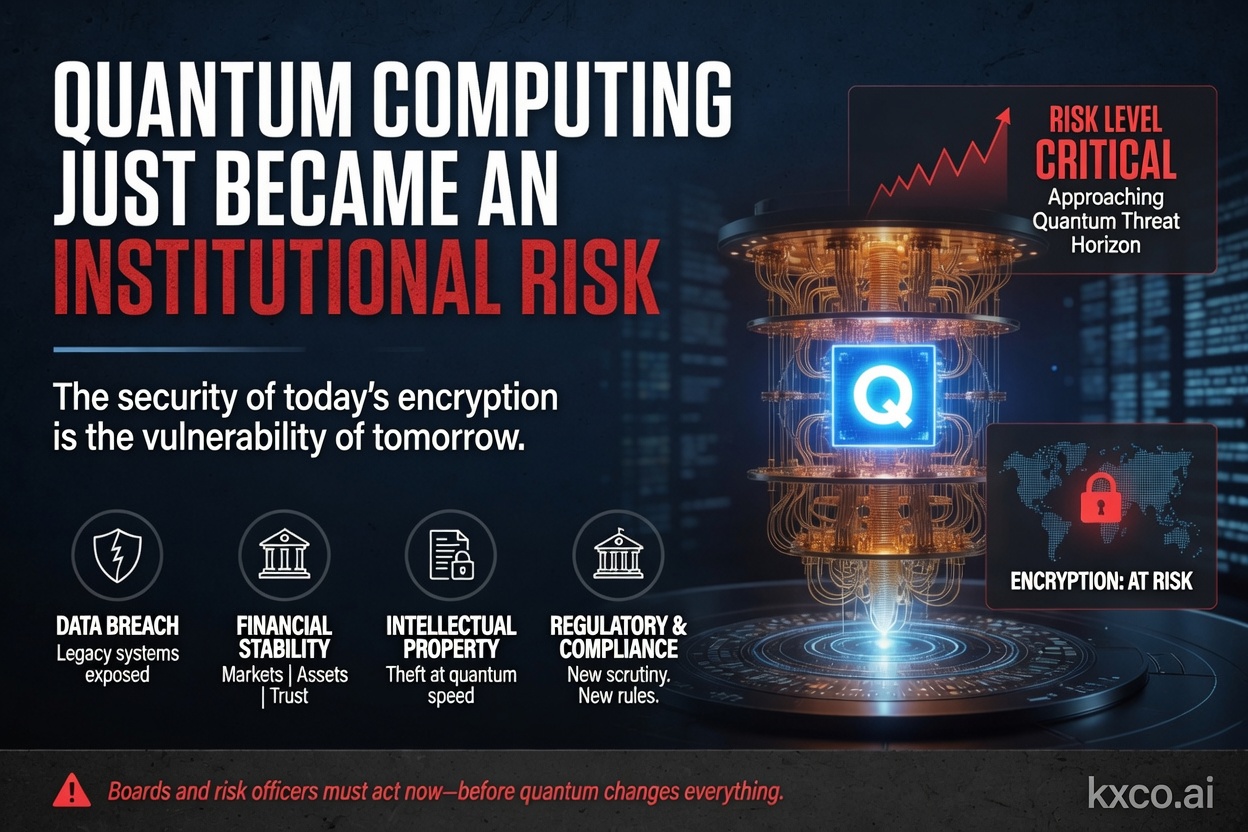

Quantum Computing Just Became an Institutional Risk

Shayne Heffernan on BlackRock's quantum-computing warning for Bitcoin and Ethereum, Google's cryptanalysis research, the two on-chain risk vectors, and how KXCO's Armature L1 — post-quantum from genesis, coordinated by its ontology — answers a threat that just went institutional.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.