Low Interest Rate Era is Over $QQQ $BTC $SPY $USD

The U.S. bond market is sending a clear message: the era of low interest rates and inflation, which began in the aftermath of the 2008 financial crisis, has come to an end. The implications of this shift are profound, touching on various aspects of policy, business, and daily life.

Recent days have witnessed a significant surge in 10-year Treasury yields, reaching 16-year highs. This surge reflects a growing belief among investors that the disinflationary forces that the Federal Reserve countered with its easy money policies after the financial crisis have now receded.

Instead, there is a growing consensus that the U.S. economy may have entered a "high-pressure equilibrium." This scenario is characterized by inflation rates surpassing the Fed's 2% target, low unemployment rates, and positive economic growth. In this new era, the challenge may no longer be trying to raise inflation rates but rather to keep them in check.

The shift in interest rate expectations carries far-reaching consequences. While higher interest rates are a welcome development for savers, they pose challenges for businesses and consumers who have grown accustomed to nearly free access to capital over the past 15 years. Adapting to a prolonged period of higher rates may result in business model failures and difficulties in affording homes and cars.

Even worse, the Federal Reserve may find itself compelled to continue raising rates, potentially to the point of causing disruptions. Minneapolis Fed President Neel Kashkari recently suggested that if the economy is indeed in a high-pressure equilibrium, the Fed may need to significantly raise rates to bring inflation back to its target. He assigned a 40% probability to this scenario.

One way to gauge investor sentiment on these developments is by examining the components of the 10-year Treasury yield. A key component, the term premium, which reflects the compensation investors require for lending money over the long term, has turned positive for the first time since June 2021. This rise in the term premium reflects heightened uncertainty about the economic outlook and monetary policy.

Simultaneously, the second component of yields, representing market expectations for short-term interest rates in 10 years, has surged in recent months to around 4.5%. This suggests that investors anticipate the Fed funds rate, currently in the 5.25%-5.50% range, will not decline significantly in the coming years.

This higher-rate outlook implies that the Fed may have more flexibility to adjust policy solely through interest rate adjustments, potentially retiring quantitative easing as a policy tool. The Fed has been gradually reducing its bond holdings, shrinking its balance sheet.

While the bond market appears confident in the end of the era of zero interest rates, there is far less certainty about the actual trajectory of the economy. Variables like the neutral rate (r-star), which determines whether the Fed's policy rate stimulates or slows the economy, remain elusive. This rate, at which growth neither accelerates nor slows while maintaining full employment and stable prices, is difficult to pin down.

The uncertainty extends to monetary policymakers, as evident in increased disagreement among policymakers about economic projections. A San Francisco Fed study from August revealed that the level of disagreement among policymakers had exceeded pre-pandemic averages by June.

In conclusion, the U.S. bond market's signaling of a new era with higher interest rates and inflation expectations is reshaping the economic landscape. While it presents opportunities for savers, it also poses challenges for businesses and consumers. The road ahead is uncertain, with the neutral rate and the economy's actual path remaining subjects of debate and speculation. Investors and policymakers alike find themselves navigating uncharted waters, with the only certainty being that change is afoot.

Ontology Is the Idea Finance Has Been Missing

The world created around 181 zettabytes of data in 2025, and AI adds more every day than anyone can read. The scarce resource is no longer data or compute. It is understanding, and understanding is a picture. Shayne Heffernan on ontology, the visual layer that turns infinite data into insight, and why finance, banking and regulation need it most.

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

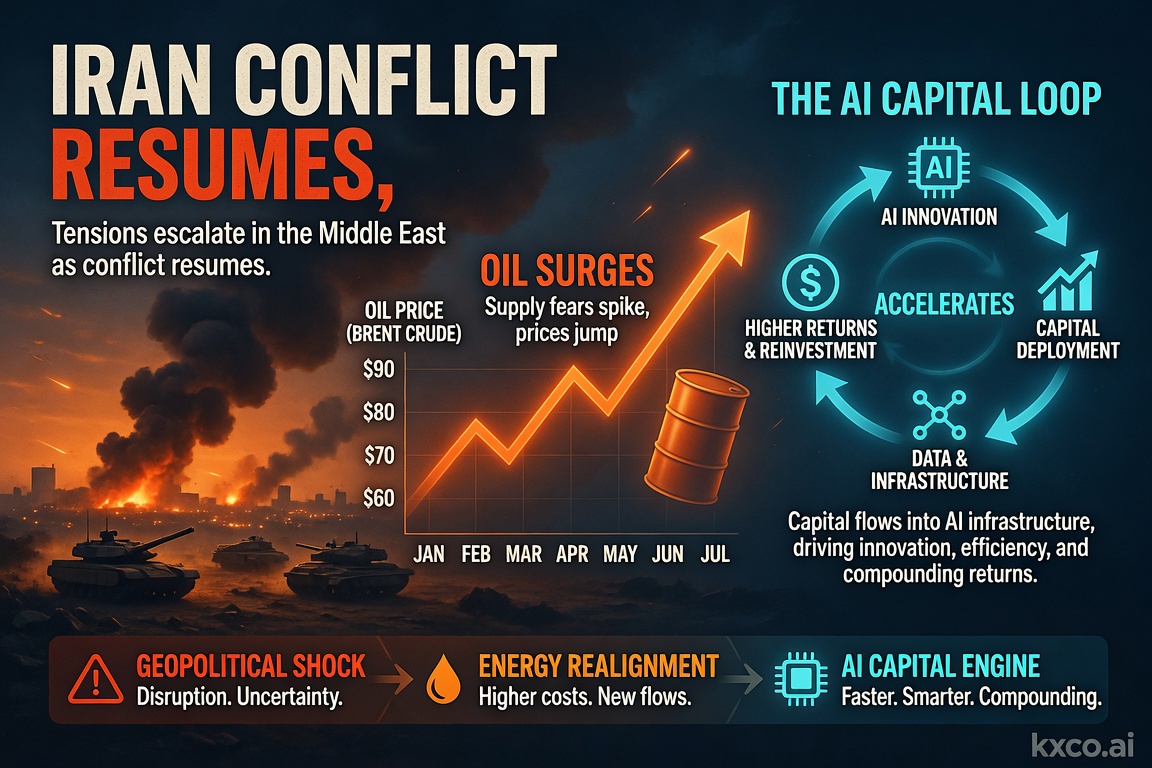

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

Ontology: Agentic AI and Infrastructure

The AI trade so far has been a compute trade. The next leg is a meaning trade — and ontology, secured and settled, is the layer almost everyone is skipping. Shayne Heffernan on why ontology is the missing layer in agentic AI, and the infrastructure it needs.

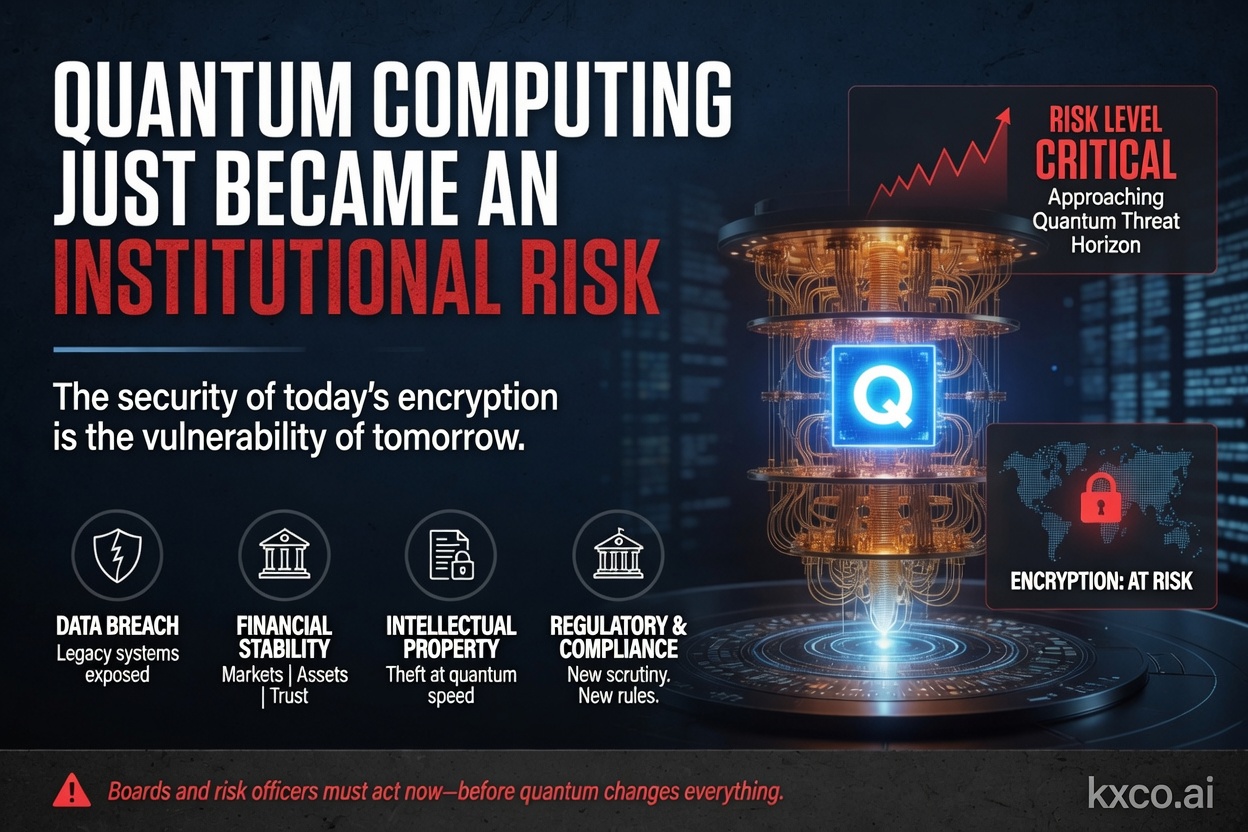

Quantum Computing Just Became an Institutional Risk

Shayne Heffernan on BlackRock's quantum-computing warning for Bitcoin and Ethereum, Google's cryptanalysis research, the two on-chain risk vectors, and how KXCO's Armature L1 — post-quantum from genesis, coordinated by its ontology — answers a threat that just went institutional.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.