Gold Miners Vs Gold Bullion $GC=F $GOLD $GDX $XAUUSD

Historically, gold miners have outperformed gold bullion as an investment. This is because gold miners are able to benefit from rising gold prices in two ways:

Increased revenue: Gold miners generate revenue by selling gold. When gold prices rise, gold miners are able to sell their gold for more money, which leads to increased revenue.

Reduced costs: Gold miners also benefit from rising gold prices because their costs are typically fixed. This means that when gold prices rise, gold miners are able to generate more profit.

Gold bullion, on the other hand, does not generate any revenue. The only way that gold bullion investors can profit is if the price of gold rises.

Here is a comparison of the historical performance of gold miners and gold bullion:

Asset

10-year total return (CAGR)

Gold miners

14.5%

Gold bullion

7.5%

As you can see, gold miners have outperformed gold bullion by a significant margin over the past 10 years.

However, it is important to note that past performance is not indicative of future results. Investors should carefully consider their own investment goals and risk tolerance before investing in gold miners or gold bullion.

Here are some of the factors that investors should consider when choosing between gold miners and gold bullion:

Investment goals: If investors are looking for an investment that generates income, then gold miners may be a better choice. However, if investors are looking for an investment that preserves their wealth, then gold bullion may be a better choice.

Risk tolerance: Gold miners are more volatile than gold bullion. This means that gold miners can experience larger price swings. Investors with a lower risk tolerance may prefer to invest in gold bullion.

Costs: Investors should also consider the costs associated with investing in gold miners and gold bullion. Gold miners typically have higher fees than gold bullion.

Overall, gold miners have outperformed gold bullion as an investment historically. However, investors should carefully consider their own investment goals and risk tolerance before investing in either asset.

The long-term outlook for gold is positive. Gold is a finite resource, and its demand is expected to grow in the coming decades. This is due to a number of factors, including:

Inflation: Gold is a hedge against inflation. When inflation rises, the value of gold tends to increase as well. This is because gold is a tangible asset that retains its value over time.

Geopolitical uncertainty: Gold is also a safe haven asset. When there is geopolitical uncertainty, investors tend to buy gold as a way to protect their wealth.

Central bank reserve diversification: Central banks are increasingly diversifying their reserve holdings away from US dollars and towards other assets, such as gold. This is because gold is a more stable and less volatile asset than the US dollar.

In addition to these factors, the increasing use of gold in technology is also supporting the long-term demand for gold. Gold is used in a variety of electronic devices, such as smartphones, laptops, and solar panels. As the demand for these devices continues to grow, so too will the demand for gold.

Overall, the long-term outlook for gold is positive. Gold is a finite resource with a growing demand. This is likely to support the price of gold in the coming decades.

Here are some specific factors that could support the price of gold in the long term:

Continued economic and political uncertainty: Gold is likely to remain a popular safe haven asset in the face of continued economic and political uncertainty.

Increased demand from central banks: Central banks are likely to continue to diversify their reserve holdings away from US dollars and towards other assets, such as gold.

Growing use of gold in technology: The increasing use of gold in technology is likely to support the long-term demand for gold.

However, there are also some factors that could weigh on the price of gold in the long term, such as:

Development of new technologies that could replace gold: For example, the development of new battery technologies could reduce the demand for gold in electronics.

Increased supply of gold: New gold mines are being discovered and developed all the time. This could increase the supply of gold and put downward pressure on prices.

Ontology Is the Idea Finance Has Been Missing

The world created around 181 zettabytes of data in 2025, and AI adds more every day than anyone can read. The scarce resource is no longer data or compute. It is understanding, and understanding is a picture. Shayne Heffernan on ontology, the visual layer that turns infinite data into insight, and why finance, banking and regulation need it most.

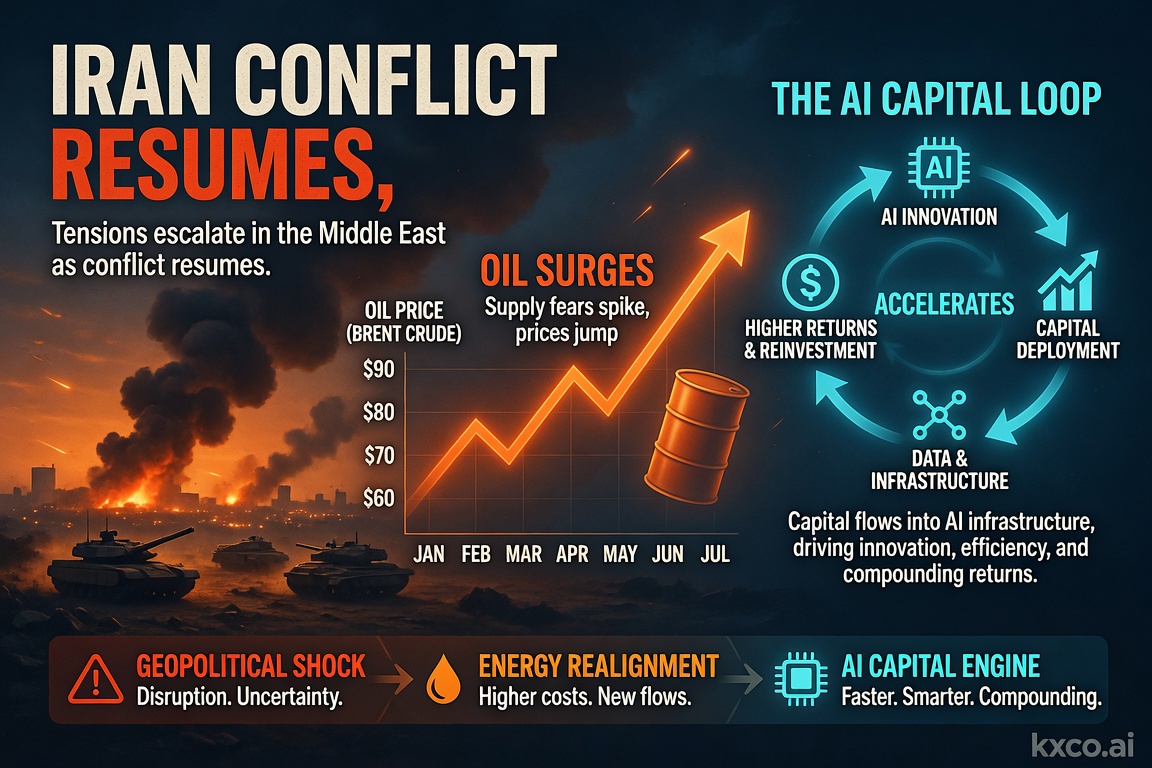

Economic Calendar and Trading Strategies for the Week Ahead: July 14–18, 2026

A pivotal week for markets: US strikes on Iran reignite the oil risk premium, June CPI and retail sales test the Fed's rate-cut path, and the $1 trillion AI capital loop keeps driving the tech trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI stocks.

Ontology: Agentic AI and Infrastructure

The AI trade so far has been a compute trade. The next leg is a meaning trade — and ontology, secured and settled, is the layer almost everyone is skipping. Shayne Heffernan on why ontology is the missing layer in agentic AI, and the infrastructure it needs.

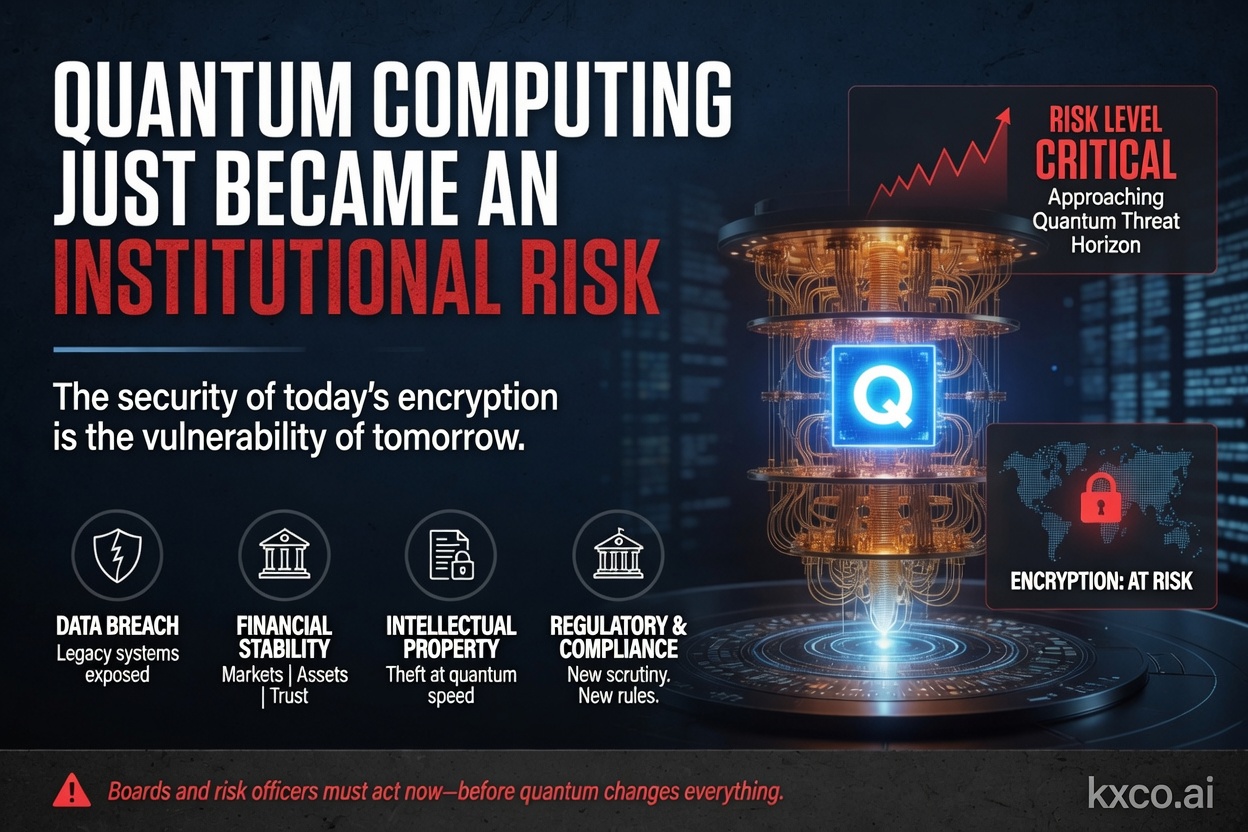

Quantum Computing Just Became an Institutional Risk

Shayne Heffernan on BlackRock's quantum-computing warning for Bitcoin and Ethereum, Google's cryptanalysis research, the two on-chain risk vectors, and how KXCO's Armature L1 — post-quantum from genesis, coordinated by its ontology — answers a threat that just went institutional.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.